10 Reasons to Buy TSS Inc.

AI picks and shovel play in the early innings of an epic ramp

This isn’t going to change anytime soon:

Why? Well:

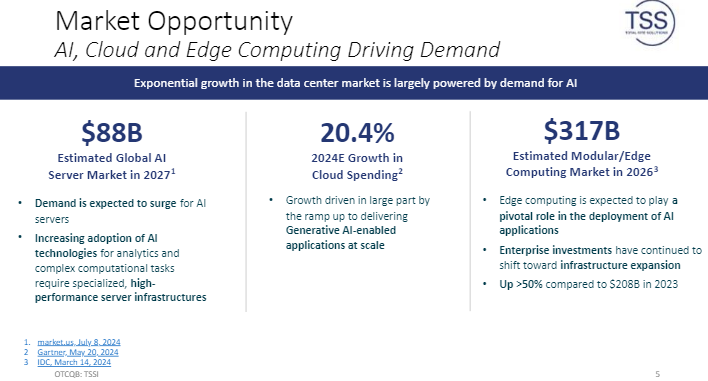

Enter consulting giant Bain & Company and a big, new forecast: “The market for AI-related hardware and software is expected to grow between 40% and 55% annually, reaching between $780 billion and $990 billion by 2027.”

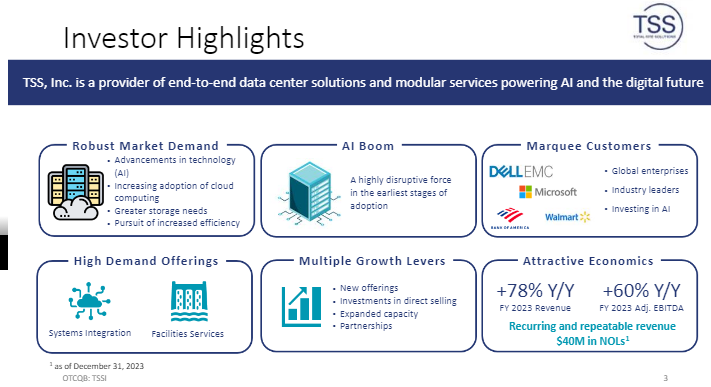

Ten reasons to buy TSS to profit from this epic build-out

TSS cleared up their act 2 years ago

Booming AI data center market

Enterprise AI to be even bigger

TSS main partner Dell is gaining share

Super Micro stumbling

xAI Elon Musk

10-folding rack integration capacity, online only since June

Q3 will see a huge ramp

Valuation is still very modest

Additional growth drivers

What does TSS do?

The company helps customers like Dell set up and integrate server racks for its customers and provides additional services like Facilities Management,

AI server demand explosion

Dell

TSS is a trusted partner, it won the Dell Technologies 2023 First Choice Partner Award. Dell also provided them with $1.7M in financing for the expansion which came online in June 2024 (per Q2CC).

Dell has woken up to the AI data center opportunity, minting its stellar reputation traditional servers and gaining market share in what’s already a rapidly growing market.

Apart from the rapid market growth Dell (and by extension, TSS) is getting two big additional tailwinds, getting half of the business from xAI (Elon Musk’s AI venture) and the other half went to its main competitor Super Micro. However, the latter is faltering (see the Hindenburg report), so more xAI business is going to Dell going forward.

TSS is an important enabler producing stuff on-time for xAI so TSS is getting more business from Dell.

So we have a triple reinforcing growth drivers, booming AI datacenter build out, Dell taking share and TSS gaining share at Dell.

Additional growth drivers

The enterprise market will grow and ultimately be bigger than the demand from hyperscalers which is booming right now.

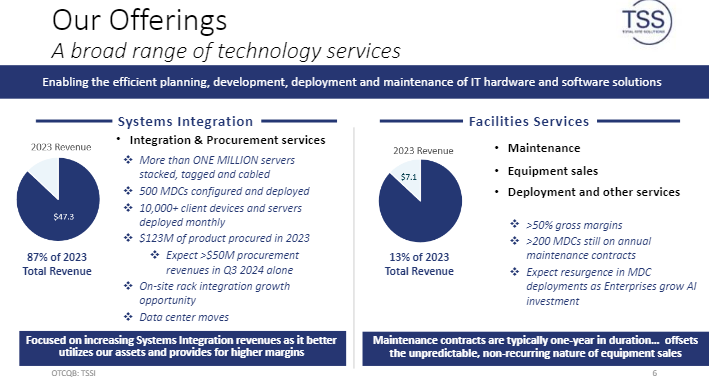

The enterprise market will also provide more opportunities in MDC (modular data centers) and Facilities Management (which produced an operating margin of 47% in Q2, it’s the segment generating the highest margins). Management expects its MDC business to grow in FY25.

The company is also in talks with a number of additional customers, in part to reduce its dependency on Dell.

The company needs a new facility that is able to handle much higher energy demands, the present facility is limited to 2.7MW but management is looking for a facility that can handle 20MW+, an indication of the sort of expansion they expect going forward (they see demand already 3-4x present constraints).

The company is also looking for M&A, partly to reduce its dependency on Dell.

New services like Data Center Move, Cybersecurity-in-a-Box, and On-site Rack Integration.

At $7+ the shares qualify for the Russell 2000 which will trigger another wave of (forced) buying, estimated at 1.5M shares. The company needs to uplist, management is aware of that and they fulfill the requirements for a senior exchange already.

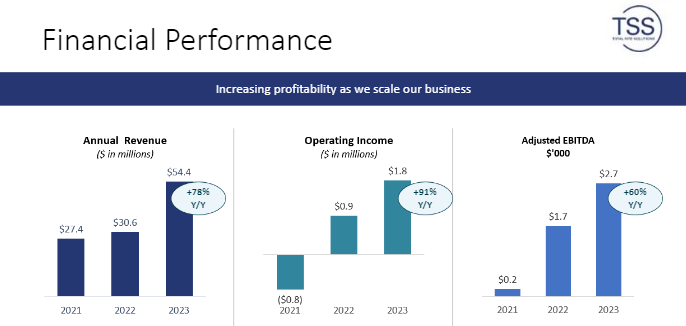

Finances

Q2 was good, even though revenues declined as low margin procurement business is very lumpy, declining from $10.6M in Q2/23 to $4.9M in Q2/24.

The most important thing to realize is this (Q2CC): “During Q2, we made a significant investment in our production capacity, which came online at the beginning of June... Demand increased in Q2, and we began delivering complex AI integration solutions on time, and I want to stress, on time, including the first stage of a highly publicized program. That initial program began in June and is being carried out into Q3.”

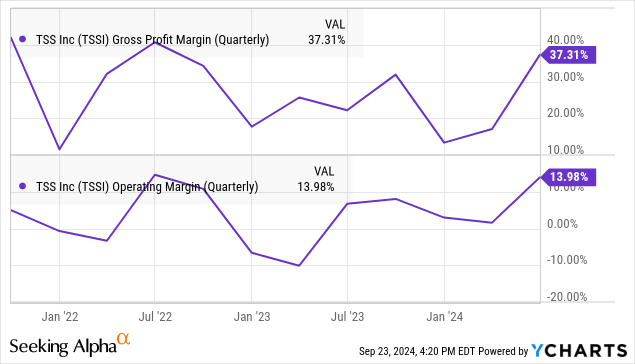

Despite the decline in revenue in Q2, gross profit increased 41% to $4.5M as higher margin rack integration and facilities management together grew 83%. The company is improving margins through economies of scale and standardization of rack integration, as well as price management.

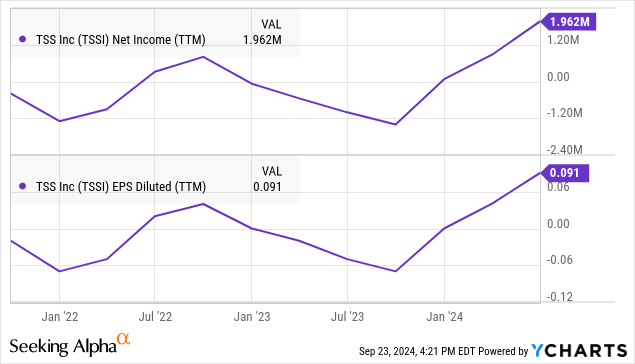

SG&A as a percentage of revenue improved 800bp to 59% so operating income improved 74% to $1.7M with net income at $1.4M (up 345%).

Q3 will see a huge ramp as capacity only came online in June will be available for the entire quarter. On top of that, the procurement business is guided to do $50M+, tenfolding sequentially. Even if margins are low (in the order of 3%, that alone adds $1.5M in earnings, more than all of earnings in Q2 ($1.4M).

We expect Q3 EPS at least double that of Q2 (with the $1.5M or so from the explosion in procurement) and likely quite a bit more as Q3 has 3 months at full capacity, rather than the one month of Q2. So we expect Q3 EPS at $0.15-$0.20

On a $0.60 EPS run rate the shares trade at 12x earnings, we think an $1 EPS run rate in the coming quarters is likely. The shares are still very cheap.

The company has no debt, $40M in NOLs.

Risks

Customer dependence, 97% of Q2 revenue came from Dell. We don’t see this as a significant risk in practice. TSS provides very valuable services for Dell, enabling it to take market share. Dell has been very accommodating, providing finance and smoothing out payments.

Lumpiness; Management doesn’t provide guidance as results can be lumpy, but the lumpiness resides mostly in the low-margin so for earnings it doesn’t matter all that much.

Conclusion

The stock might not continue in a straight line up as it has done all year, but it’s still cheap and in the midst of an epic ramp, so you can still buy at $7 and add at every dip.

This is only in the very early innings: ["But in the past couple of days, reports from Bloomberg and the New York Times have provided more details about what OpenAI in particular is trying to get from the government: support in its quest to build data centers with power requirements of five gigawatts each.

Five gigawatts is an astonishingly large amount of power. It’s the output of around five nuclear reactors—the kind of power you need for a whole major city like Miami. It’s as much as 100 times the requirement of a standard large data center. The Times reported that OpenAI’s 5GW proposal drew laughter from a Japanese official."] https://fortune.com/2024/09/27/openai-5gw-data-centers-altman-power-requirements-nuclear/

What better reason to buy an picks and shovels AI play like TSS Inc: "Enter consulting giant Bain & Company and a big, new forecast: “The market for AI-related hardware and software is expected to grow between 40% and 55% annually, reaching between $780 billion and $990 billion by 2027.” https://finance.yahoo.com/news/a-big-ai-prediction-re-juices-the-trade-morning-brief-095550869.html