16% yield with no credit risk?

This sounds too good to be true..

We found another interesting article for investors interested in high yield. The main selling point here is that the vehicle in question invests in Agency MBS (Mortgage Backed Securities).

Weren’t these one of the instruments that blew up in investors’ faces during the 2008-9 financial crisis? Well, yes, but here is the crux: with Agency MBS, the principal is guaranteed by the Agency (Fannie, Freddy, Ginnie).

If a borrower defaults, the agency buys the mortgage back at par value, resulting in agency MBS having no credit risk.

Introduction to Agency MBS

See here for an intro to Mortgage Backed Securities.

Agency Mortgage-Backed Securities (MBS) are a type of investment that represents a share in a pool of residential mortgage loans that have been bundled together and sold to investors.

These mortgages typically conform to specific underwriting guidelines set by government-sponsored enterprises (GSEs). The process begins with financial institutions like banks issuing mortgages to homebuyers.2

These institutions then pool together many similar mortgages and sell them to a trust or a GSE. This trust or GSE then structures these loans into MBS, which are subsequently sold to investors. Investors in Agency MBS receive monthly payments that include both principal and interest from the underlying mortgages, net of servicing and guarantee fees.

Agency MBS are generally considered to have very low credit risk due to the backing of U.S. government agencies or GSEs. The three main entities involved are:

Ginnie Mae (Government National Mortgage Association): MBS issued by Ginnie Mae are backed by the full faith and credit of the U.S. government, similar to U.S. Treasury bonds. This explicit government guarantee means that investors are highly protected against credit risk.

Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Corporation): These are GSEs that purchase and securitize conforming mortgages. While their securities are not explicitly backed by the full faith and credit of the U.S. government, they are understood to have limited credit risk, especially as they have been under government conservatorship since 2008. These agencies provide a guarantee of timely payment of principal and interest to investors, even if borrowers default.

The sponsoring agency (Ginnie Mae, Fannie Mae, or Freddie Mac) essentially assumes the credit risk of borrower defaults. If a homeowner in the mortgage pool defaults on their loan, the agency pledges to buy that defaulted loan out of the pool.

This guarantee transforms the risk for investors from credit risk (the risk of losing money due to borrower default) to prepayment risk (the risk that homeowners will refinance or pay off their mortgages early, especially when interest rates fall).

While prepayment risk can affect the timing and amount of cash flows, the guarantee ensures that investors will still receive their principal back. This is why Agency MBS are generally considered to be without credit risk.

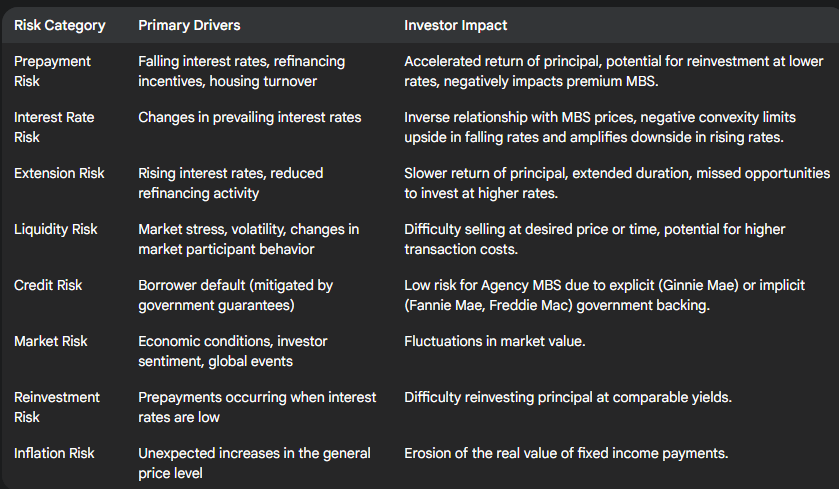

Be that as it may, there are other risks:

Let’s get to the main points of the article about a vehicle that invests in these agency-backed MBS and generates high yields through leverage.