A Primer On Dave Inc.

Dave (DAVE) has had a spectacular run (forget about the 2021 idiotic valuation during the pandemic bubble), and recently the stock price is accelerating again:

Below is our free primer to familiarize investors with the moving parts, followed later by an assessment of the financials, latest developments, and verdict.

Overview

Dave Inc. is a leading mobile-first neobank designed to provide everyday Americans with more effective money management tools.

The company targets the financially coping or vulnerable, a segment estimated at 185M Americans (69% of the US population) who are often underserved by traditional banks.

Since its inception in 2017, over 19M members have signed up for the app, with more than 14 million having used at least one product.

The mission is to level the financial playing field by offering transparent, low-cost alternatives to legacy banking systems that charge high fees for basic services.

As of December 31, 2025, Dave employed approximately 280 full-time employees. The company operates a remote-first strategy with employees across more than 30 states, which has helped reduce voluntary turnover to below peer median rates.

Dave uses the OKR (Objectives and Key Results) framework to align priorities and foster accountability across the organization.

Core Product Offerings

ExtraCash provides members with up to $500 in short-term credit via a discretionary overdraft through bank partners to bridge liquidity gaps between paychecks.

In February 2025, Dave transitioned to a mandatory 5% overdraft service fee (with a $5 minimum), replacing its previous optional fee model to enhance unit economics.

Dave Checking is a fee-free demand deposit account offering FDIC pass-through insurance, a branded debit Mastercard, and access to 40,000 fee-free MoneyPass ATMs.

Personal Financial Management (PFM) is a platform that includes tools such as Budget (overdraft prediction), Goals (automated savings), and Side Hustle (a job application portal for gig economy work).

In mid-2025, Dave increased its monthly membership fee from $1 to $3 for new members, which has improved average revenue per user (ARPU) and customer lifetime value.

Proprietary Technology and AI

CashAI is Dave’s proprietary underwriting engine that analyzes real-time cash flow data—including income patterns and spending behavior—rather than relying on FICO scores or credit bureau data.

Model v5.5 was implemented in September 2025, nearly doubled the feature set of prior models, and is optimized for the new fee structure, resulting in higher approval amounts and lower delinquency rates.

CashAI has been trained on over 180M originations and billions of transactions, providing a structural data advantage in credit decisioning.

The company utilizes DaveGPT (an AI chatbot) for automated member support and proprietary AI systems for real-time fraud detection and prevention.

Dave operates a cloud-native platform, which reduces the cost to serve members and allows for rapid deployment of new software and AI models.

Strategic Growth Pillars

Dave maintains a stable customer acquisition cost (CAC) of approximately $19, with payback periods now under four months—the fastest in the company’s history.

")

The Engagement and Retention strategy focuses on converting members into Dave Debit Card actives, who generate 1.7x higher ARPU and have 11 times the monthly transaction volume compared to non-card users.

The company leverages its foundation in underwriting and payments to prepare for the launch of new products in FY26.

Operational Partnerships

Dave currently operates concurrent programs with Evolve Bank & Trust and Coastal Community Bank.

As of Q4/25, all new members are being onboarded to Coastal Community Bank, with the transition of existing members expected to be finalized by the end of 2026.

Dave has a multi-year agreement with Galileo Financial Technologies for payment processing, which was amended in 2023 to significantly reduce processing fees.

Regulatory and Competitive Landscape

Dave is subject to regulation by the CFPB, FTC, and various state authorities regarding consumer protection, AML (Anti-Money Laundering), and privacy laws.

The company is monitoring evolving rules, including the CFPB’s finalized 2024 revisions to overdraft rules under the Truth in Lending Act and new Open Banking standards under Section 1033 of the Dodd-Frank Act.

Dave competes with traditional large banks (JPMorgan Chase, Wells Fargo), digital neobanks (Chime, Varo), and other fintech innovators (MoneyLion, Earnin, Affirm).

Management argues its 4.8-star App Store rating and structural cost advantage (no physical branches) allow it to offer a superior value proposition to the paycheck-to-paycheck market.

FY25 Financials

That stock price acceleration is no surprise:

FY25 was very strong: revenue rose 60% to $554.2M, net income increased 238% to $195.9M, and adjusted EBITDA grew 162% to $226.7M. The company also ended the year with $123.2M of cash and investments and lifted its share repurchase authorization to $300M.

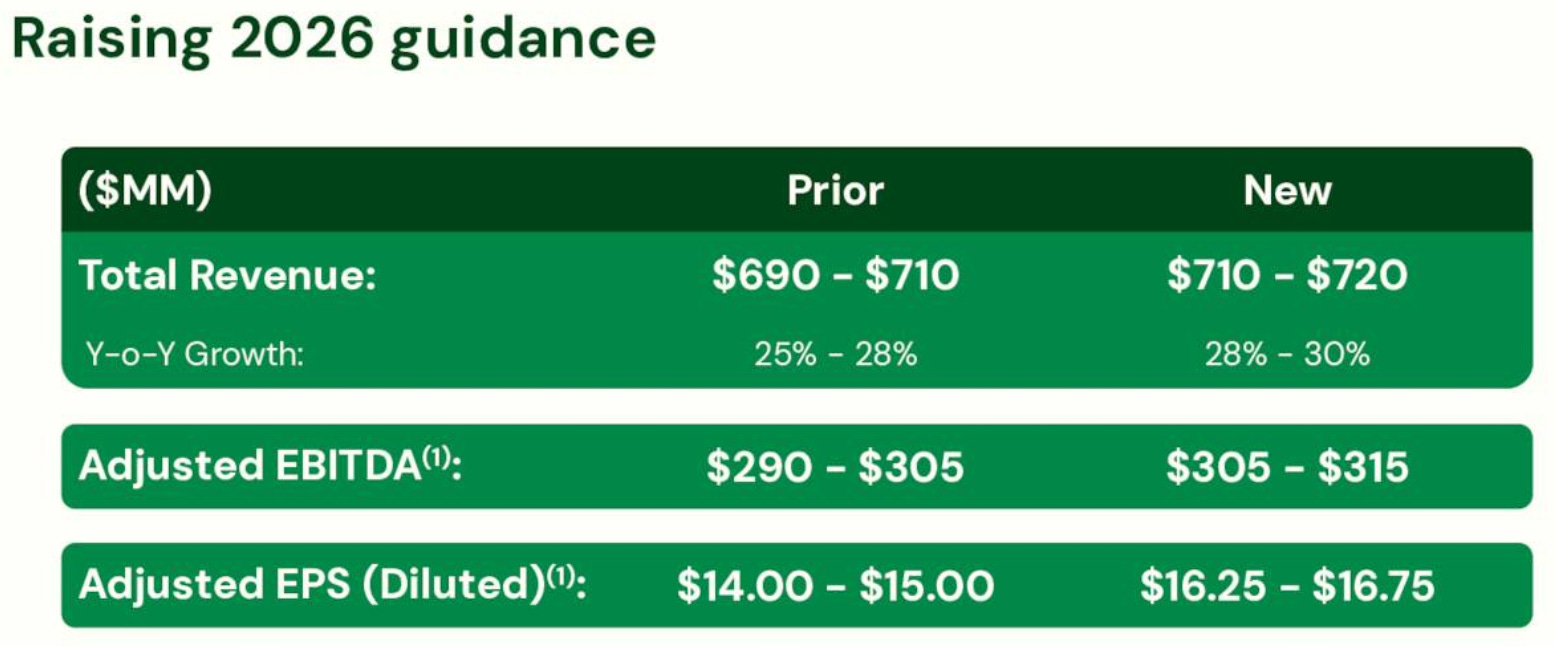

And FY26 promises to be good as well:

Note of caution: the short position has been rapidly rising in H1/26 to almost 25% of the float.

Stay tuned for our take on the financials and prospects.