A Primer on Iridex

Iridex (IRIX) has turned around, with both its businesses (its cash cow retina business and its smaller and more recent glaucoma growth business) growing again, and there has been a great deal of cost-cutting, with more to come. Cash flow and adjusted EBITDA turned positive in Q4/25.

Pending MDR certification in the EU (expected this year) will boost sales of its flagship PASCAL platform for retina, which is already benefiting from an upgrade cycle in the US.

We think the shares offer compelling risk/reward at $1, with an EV of just $15M and a 0.29x FY26 EV/S valuation, even if FY26 guidance ($51M-$53M) was cut a bit, excluding any FY26 sales from the Middle East. There has been a stream of insider buys over the past 12 months, and we don’t see that ending anytime soon either.

Business Overview

IRIDEX is an ophthalmic medical technology company specializing in products and procedures for glaucoma and retinal diseases.

The company’s value proposition centers on MicroPulse Technology and Endpoint Management Technology, which provide tissue-sparing, subvisible laser therapy as an alternative to standard continuous-wave (CW) treatments.

Revenue is generated through the sale of laser consoles and recurring sales of consumable products, specifically single-use laser probes, along with service contracts.

Management aims to promote MicroPulse as a primary treatment option while pursuing organic growth and potential complementary acquisitions.

Glaucoma

Glaucoma is the company’s smaller (29% of revenue) growth business, not yet profitable.

The primary console is the Cyclo G6 laser system, which works with a family of disposable probes, including the MicroPulse P3, G-Probe, and G-Probe Illuminate, generating a stream of recurring revenue. Probe sales were up 18.9% in Q4/25. Production will be outsourced to reduce costs.

Recent clinical studies showed that the device is safe to repeat and patients have been followed for 5 years with no side effects recorded, which is an advantage against MIGS (Minimally Invasive Glaucoma Surgery) implants, some of which carry a long-term erosion risk.

Retina

Medical Retina Line: Includes the PASCAL (Pattern Scanning Laser) System and the portable IQ 532 and IQ 577 laser systems.

Surgical Retina Line: Features the OcuLight TX and SLx systems, often used in vitrectomy procedures for treating retinal tears and detachments.

Consumable Probes: The business relies on recurring sales of single-use devices such as EndoProbe handpieces for surgical retina and patented probes for glaucoma treatment.

Versatility: Many consoles are designed for multispecialty practices, allowing a single laser to be used for both retinal disorders and glaucoma treatments.

Market

Growth is driven by an aging global population and the increasing prevalence of diabetes, which is expected to affect 700M people by 2045.

Glaucoma Market: With 80-100M candidates for treatment, IRIDEX targets an unmet need for therapies that avoid the compliance issues of pharmaceuticals and the invasiveness of traditional surgery.

Principal laser competitors include Alcon Inc., Carl Zeiss Meditec AG, and Lumenis Ltd.

The company also competes against pharmaceutical giants like Pfizer and Regeneron, as well as surgical device companies like Glaukos and Sight Sciences.

Operations

IRIDEX assembles critical subassemblies and final products in Mountain View, California, but relies on third-party suppliers for many components. Beginning in FY26, the company is moving to contract manufacturing in order to bring down COGS. This process will be completed by FY27.

A team of 11 engineers and regulatory professionals focuses on mechanical, electrical, and optical design to introduce new clinical applications.

The company’s portfolio includes 67 active US patents and 94 international patents, with dozens of additional applications pending.

As of January 3, 2026, the company employed 93 full-time equivalent employees, with the largest concentration (42) in operations and manufacturing.

Regulatory Environment

IRIDEX has obtained 510(k) clearances for all medical devices marketed in the US that require it.

Products are currently CE marked in the EU under the Medical Device Directive (MDD), with a transition to the newer Medical Device Regulations (MDR) required by the end of 2028. MDR certification is expected this year, which will unblock pent-up demand for its flagship PASCAL platform (retina).

The company is susceptible to changes in government and private insurance policies, as fixed-sum reimbursement limits can affect the budgets of hospitals and clinics for purchasing new equipment.

Revenue is typically subject to seasonal fluctuations, with lower sales in the third quarter often attributed to European summer holiday closures.

FY25 Finances

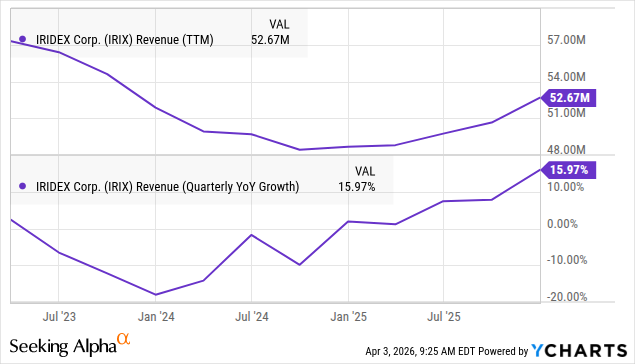

Total revenue for fiscal year 2025 was up 16% to $52.7M.

The company reported a net loss of $4.4M in 2025, which represents a significant narrowing from the $8.9M net loss recorded in 2024. Management slashed 22% of OpEx, and more cost-cutting is to come from moving facilities to cheaper locations and contract manufacturing.

Sales outside the US accounted for 55.9% of total revenue in 2025.

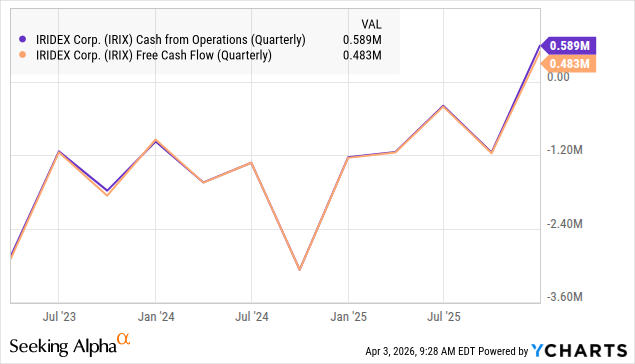

Cash flow turned positive in Q4/25:

IRIDEX utilizes a direct sales force in the US and Germany, while relying on Topcon Corporation and other independent distributors for most other international markets.

Macroeconomic Headwinds: Business operations are currently impacted by inflation, high interest rates, and conflicts in the Middle East, which have led some customers to extend their capital equipment purchase cycles.

FY26 guidance has been reduced to 1-5% growth ($51M-$53M) as management doesn’t count on any sales to the Middle East for FY26.

At $1 per share, the company has an EV of $15M, a 0.29x EV/S valuation.

The company seems back on its feet with its businesses growing again, and a great deal of cost-cutting ensued, with more cost-cutting to come. Adjusted EBITDA and cash flow turned positive in Q4, and the valuation of the shares seems compelling to us, offering low risk and substantial reward.

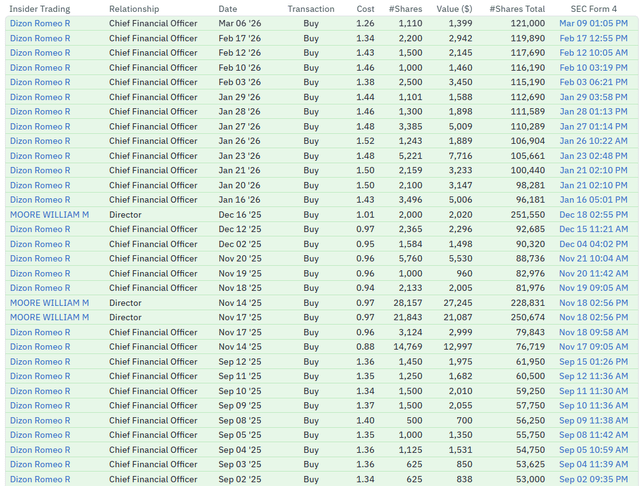

Insiders seem to agree; there has been consistent insider buying: