A Primer on KORU Medical

Introduction

KORU Medical (KRMD) specializes in innovative solutions for subcutaneous drug delivery, focusing on enhancing patient care and simplifying medication administration.

The company has turned around its fortunes and while the shares got ahead of themselves a little, that is now correcting, providing another entry point.

Reasons to buy

Unique products, recurring revenue

Tailwinds from:

Shift from Ig towards SCIg

Shift towards prefilled syringes

Market share gains

International expansion

Novel therapies offers open ended expansion

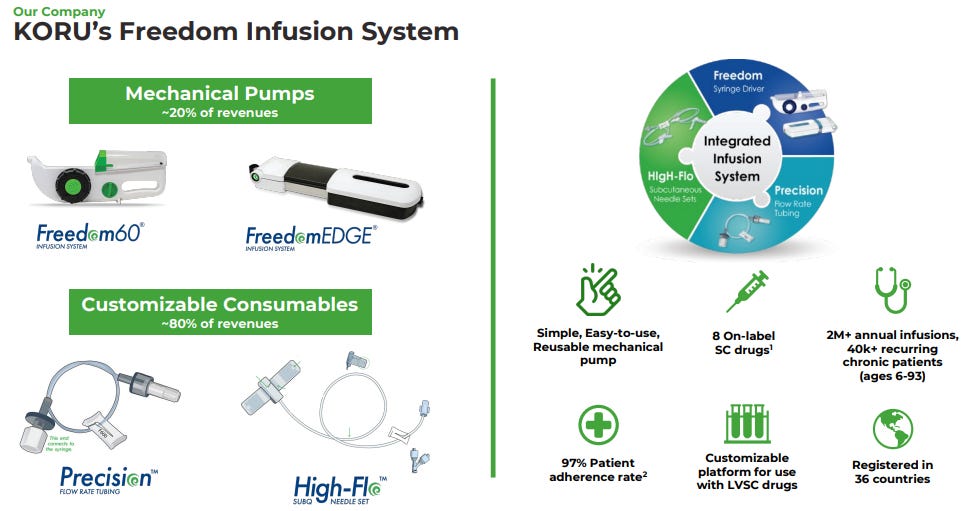

Products

FREEDOM60 Syringe Driver, compatible with standard 60/50ml syringes.

FreedomEdge Syringe Driver, compatible with standard 30/20ml syringes and prefilled syringes.

HigH-Flo Subcutaneous Safety Needle Sets, available in 26- and 24-gauge sizes, are designed specifically for subcutaneous self-administration.

Precision Flow Rate Tubing regulates flow rate and infusion time, minimizing drug waste with low residual volume.

The FREEDOM System boasts several advantages:

Portability and Ease of Use: Compact, lightweight, and user-friendly design.

Maintenance-Free Operation: No batteries or electricity required.

Low Pressure Operation: Operates at lower pressure than electronic pumps, enhancing patient comfort and subcutaneous tissue tolerance.

It saves the healthcare system time and costs; hence payors are onboard.

The FREEDOM system can be used to deliver a variety of drugs used in oncology, nephrology, and rare diseases like primary immunodeficiency diseases (PIDD), Chronic Inflammatory Demyelinating Polyneuropathy (CIDP), and Paroxysmal nocturnal hemoglobinuria (PNH).

Favorable data was presented regarding the use of the KORU FreedomEdge pump versus manual syringe administration for subcutaneous oncology biologic drugs with 3K infusions performed by 33 nurses who had previously administered the same drug using the manual push method.

Compatibility with prefilled syringes, which is a market trend and a driver of growth.

The system holds FDA clearance for numerous on-label subcutaneous indications, including specific clearance for leading immune globulins and select intravenous antibiotics.

Business model

Sales and Distribution

KORU utilizes a multi-channel sales and distribution network:

Direct Sales: To pharmaceutical companies, specialty pharmacies, and home infusion providers.

Medical Device Distributors: Facilitate one-stop shopping and remote inventory management for specialty pharmacy customers.

Manufacturing and Raw Materials

KORU conducts manufacturing, assembly, packaging, and quality control at its Mahwah, NJ facility.

Command Medical Products, Inc. (Command), a contract manufacturing organization in Nicaragua, provides subassemblies and manufactures approximately 80% of KORU's consumables.

All components are sourced from single-source third-party suppliers due to stringent regulatory approval and validation requirements.

Research and Development

Committed to ongoing research and new product development, with significant investments planned for the next 12 months to develop a "next-generation" infusion pump and consumable system.

Aims to enhance existing product performance and innovate new product opportunities to strengthen the company's portfolio.

Revenue streams

Domestic Core Sales of the FREEDOM System and associated accessories in the US and Canada, primarily for subcutaneous immunoglobulin (SCIg) therapies targeting diseases like PIDD and CIDP.

International Core Similar to domestic core, this revenue stream focuses on SCIg treatments but in markets outside the US and Canada.

Novel Therapies This segment includes revenue from:

Product Revenue generated through feasibility/clinical trials with biopharmaceutical companies developing new subcutaneous drug therapies.

Non-Recurring Engineering Services (NRE) provided to biopharmaceutical companies, aiding in the customization and regulatory preparation of the FREEDOM System for clinical and commercial use across various drug categories.

The company generates recurring revenues from consumables, like precision flow rate tubing, high-Flo subcutaneous safety needle sets, and prefilled syringes.

Growth

Core domestic market

The domestic core business experienced a 14% revenue increase in Q2 2024 compared to the same period in 2023. This growth continued in Q3 2024 with a 12% increase, making it the company's highest quarterly revenue to date and outpacing the SCIg market which itself was growing at a healthy mid to high single-digit rate. The main growth drivers are:

New patient starts are up producing share gains as subcutaneous administration expands across the overall immunoglobulin market.

The existing patient base creates a large, recurring revenue stream of consumables.

A market-wide shift towards SCIg as a preferred therapy, with pharmaceutical companies investing in their subcutaneous portfolios.

The adoption of prefilled syringes, a more convenient option for patients, is also driving growth. KORU's devices are compatible with prefilled syringes.

Expanded SCIg labels: The FDA approval of an expanded label for the SCIg drug XEMBIFY, allowing treatment-naive patients to start directly on SCIg rather than IVIg, is expected to increase the number of patients using SCIg.

CIDP market growth: The chronic inflammatory demyelinating polyneuropathy (CIDP) market is also growing, with new diagnoses and prefilled syringe delivery options making it easier for these patients to move to SCIg therapy.

Product innovation: KORU is investing in product innovation to drive growth and expand its market share.

International growth

Q2 growth of 46% includes some accelerated shipments due to residual effects from a prior issue, normalized growth was approximately 20%. Q3 growth was 5% but normalizing for excess inventory, growth would have been approximately 24%. The international business grew 38% YTD. The main growth drives:

Underlying IG market growth

KORU Medical is increasing its penetration in current markets, with a focus on both new and existing customers. They are also working with pharmaceutical companies and distribution partners to increase penetration in existing markets.

The company has expanded into new markets and seen growth in existing markets due to new indications for SCIg therapy. For example, the approval of the FreedomEdge infusion system in Japan is expected to drive further growth in 2025 and beyond. KORU also entered a new market in Austria in Q3/24.

As additional countries and regions expand their subcutaneous immunoglobulin (SCIg) therapy indications, KORU expects to see a continued increase in their consumables volume, driven by a growing patient base and share gains.

KORU is focused on expanding its presence into new geographies, and sees a significant market opportunity for SCIg outside of the U.S.. The company is currently marketed in 25 countries worldwide. They are also working to increase penetration in existing SCIg markets, tailoring device and patient programs with pharmaceutical companies and distribution partners.

KORU works with a network of 26 distributors outside of the US to expand its market reach.

Novel Therapies

Novel Therapies exploded with a 276% increase in Q3/24 after being up 50% in Q2. This growth is attributed to progress with non-recurring engineering (NRE) services and strong product sales supporting customer clinical trials. The company has seen improved NRE margins as a result of bringing engineering and development activities in-house.

There was an increased number of new collaborations and clinical trial orders 16 pipeline collaborations, representing a worldwide TAM of $2.7B on 2M+ patients.

The company just signed another collaboration with a global pharma company together with partner SCHOTT (who contributes its TOPPAC prefillable polymer syringes) and this isn’t likely to be the last of these types of deals.

Many of KORU Medical's collaborations have progressed closer to commercialization, including three opportunities in the IG business, a rare disease biologic for infusion clinics, and oncology biologics, opening up the market for oncology infusion clinics (Q3CC):

The rare disease biologic in 2025 will be an expanded market entry to the infusion clinic, in our oncology biologics, which we anticipate by the end of 2025 is potentially impactful given the large patient population... The manual syringe method is the standard-of-care for the approximate 2.5M global oncology biologic infusions performed today.

Management anticipates six potential launches by 2026 across its collaborations, including opportunities in the IG business, a rare disease biologic for infusion clinics, and oncology biologics.

Oncology Infusion Clinic Opportunity: Favorable data was presented regarding the use of the KORU FreedomEdge pump versus manual syringe administration for subcutaneous oncology biologic drugs. A study observed that nurses using the KORU FreedomEdge system reported increased patient interaction, less hand pain, and more time efficiency than with the manual push method. This study has created an opportunity for an improved delivery method within infusion centers, which KORU is eager to capitalize on.

Innovation

Its product development team is continuously improving existing products and innovating new product opportunities. For instance, the company expects a 510(k) submission for its next-generation device in mid-2025.

KORU is also updating the timing of its 510(k) submission for a rare disease biologic, with filing anticipated in 2025.

Finances

Revenues +17% to $8.2M. The company saw double-digit growth across all businesses, outpacing the SCIg market. Preliminary Q4 revenue +23% to $8.9M with preliminary FY24 growth at 18% to $33.7M

Domestic core revenues +12% to $6.4M.

International core business grew 5% to $1.1M. Excluding the residual effects of Q2 BSI stocking orders, international growth would have normalized to approximately 25%.

Novel Therapies revenue totaled $600K, a 276% increase year-over-year. This growth was driven by progress on non-recurring engineering services work for six collaborations and strong product sales supporting customer clinical trials.

Gross profit +19% and gross margin +140bp to 63.4%. The increase was driven by improved NRE margins and ASPs from contractual price increases, offset by changes in product sales mix.

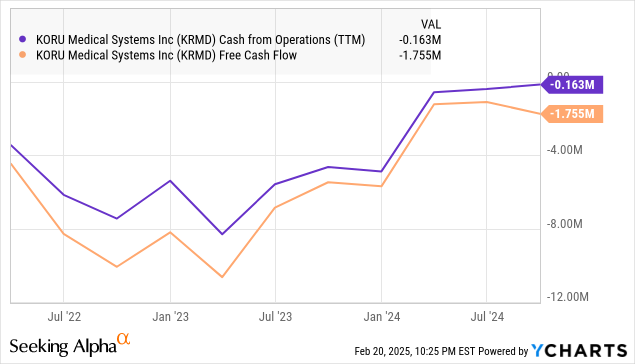

Cash usage contributors included a net loss of $800K (excluding non-cash items), $700K in investing activities for capital purchases for a new consumables product line, and $200K in working capital usage.

Cash balance at the end of Q3 was $8.8M. Cash usage for the quarter was $1.7M, in line with expectations. Preliminary Q4 figures show the cash balance at $9.6M at the end of Q4, positive cash flow of $0.8M for the fourth quarter, and FY24 cash burn of $1.9M, a 67% improvement over the prior year.

The company raised FY24 guidance to $32.75M to $33.25M but preliminary figures are even better at $33.9M.

Gross margin guidance increased to 62% to 63%.

Operating expense will finish slightly higher at $24.5M to $25M, exclusive of stock compensation.

KORU Medical anticipates reaching cash flow breakeven in Q4 and being cash flow positive, excluding capital expenditures, for the full year 2025.

Year-to-date cash usage has substantially reduced, with a 60% improvement compared to 2023.

The company has zero debt and access to a $10M long-term credit facility.

Revenue growth has been impressive at 15%, and margin expansion is at 560 basis points.

Improvements, along with disciplined operating expense management, have led to a 20% improvement in lower reported net losses and 29% and 60% improvements to EPS and cash burn, respectively.

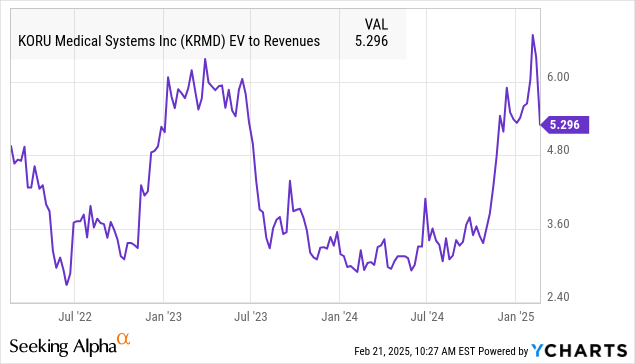

Valuation

Fully diluted there are 47.25M shares, at $3.6 per share that’s a market cap of $170M and an EV of $160.5 M. With analysts expecting FY25 revenue at $38.4M producing a FY25 EV/S of 4.17x

Analysts still expect a $0.07 EPS loss for FY25.

Piper Sandler is right that the shares were trading near multi-year highs:

That’s the trailing EV/S, but one can argue that the increase in valuation multiple reflects improving fundamentals, especially becoming cash flow breakeven in Q4.

They do have a point that FY25 comps are more difficult and novel therapies is more slanted for FY26.

Conclusion

We see an attractive long-term growth story with improving fundamentals, becoming cash flow positive is especially encouraging.

The company has major growth avenues (domestic, international, and especially novel therapies) in front of it, which aren’t likely to disappear.

It’s true that the shares aren’t cheap and FY25 has difficult comps, but FY26 looks better and the company has turned the corner on cash flow, always very important for small growth companies.

We think investors can start accumulating the shares at $3.5-$3.7.