A Primer on Limbach

Overview

Limbach Holdings, Inc. (LMB) is a Delaware corporation that functions as a building systems solution firm. Headquartered in Warrendale, Pennsylvania, the Company partners with building owners and facilities managers regarding mission critical mechanical (heating, ventilation, and air conditioning), electrical, and plumbing infrastructure.

The Company operates primarily in the eastern and midwest regions of the United States, utilizing approximately 1,400 team members across 20 offices. Limbach’s team members combine engineering expertise with field installation skills to provide custom, full life-cycle solutions, addressing both the operational and capital projects needs of customers.

Core Market Sectors (Mission-Critical Systems): Limbach’s distribution of revenue across end-use sectors is designed to reduce exposure to negative developments in any single sector. Core sectors include:

Healthcare (including research, acute care, and inpatient hospitals).

Industrial and manufacturing (including automotive, energy, and general manufacturing plants).

Data centers (facilities composed of networked computers and computing infrastructure).

Life sciences (research and development focused on living things).

Higher education (public and private colleges, universities, and research centers).

Cultural and entertainment (including casinos, amusement rides, and parks).

FY24 Key Performance Highlights

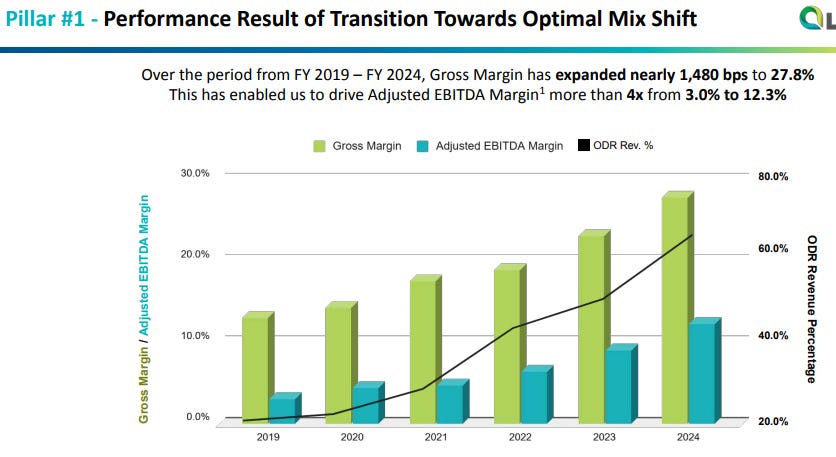

Limbach produced record annual gross profit and gross profit margins in 2024.

Net Cash Provided by Operating Activities $36.8M

Consolidated Gross Profit Margins 27.8% expanded by 470 basis points (bps).

Diluted Earnings Per Share (EPS) $2.57 increased by 46% versus 2023.

ODR Segment Revenue 66.6% of total consolidated revenue, achieving the 2024 target of 65%-70%.

Successfully completed two acquisitions: Kent Island Mechanical, LLC and Consolidated Mechanical, LLC.

Strategic Focus

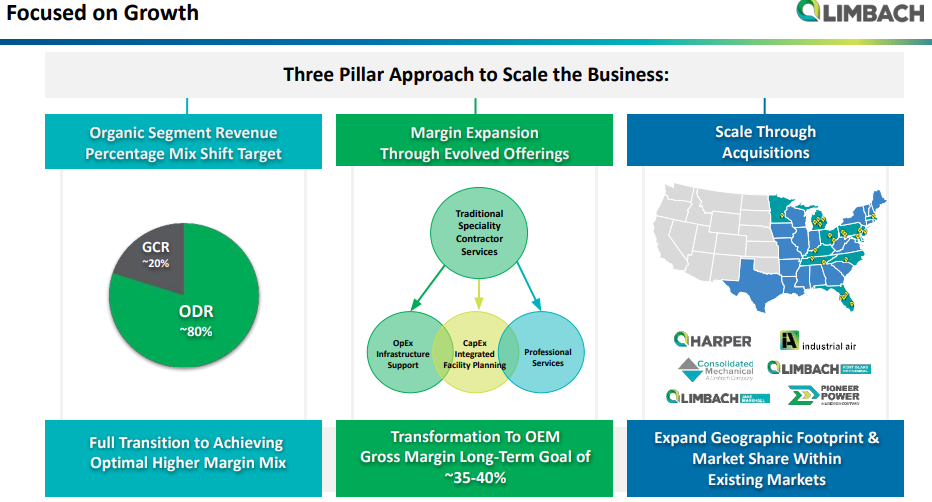

The Company's overall strategy focuses on creating value for building owners by developing long-term relationships and becoming an indispensable partner. This strategy is executed through a three-pillar approach:

Improve profitability and generate quality growth by shifting focus to the Owner Direct Relationships (ODR) segment.

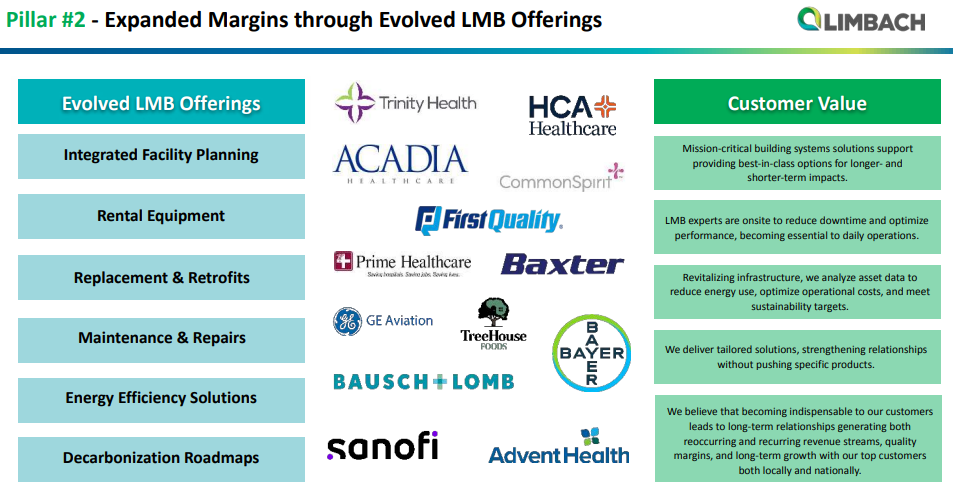

Expand margins through evolved offerings.

Scale the business through acquisitions.

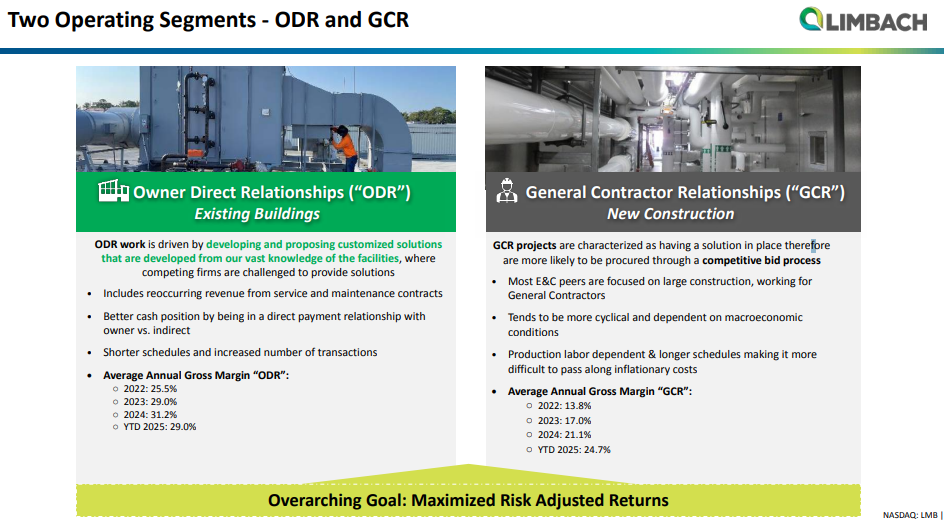

Owner Direct Relationships (ODR) Segment

The ODR segment involves performing owner-direct projects and/or providing maintenance or service primarily on mechanical, plumbing, or electrical systems directly to building owners or property managers. The ODR segment typically yields higher margins compared to the GCR segment.

ODR Focus and Offerings: The initiative is to position the Company as an indispensable partner, providing full life-cycle capabilities from concept design/engineering through system commissioning and 24/7 service. This focus on long-term partnerships and maintenance services is intended to improve revenue predictability and increase economic resilience.

ODR services include:

Integrated Facility Planning (engineer-led facility assessments and capital planning support).

Replacements & Retrofit (tailored MEP equipment upgrades and comprehensive system replacements).

Rental Equipment (turnkey rental solutions, including system design and maintenance, for planned replacements or emergencies).

Maintenance and Repairs (comprehensive inspection, troubleshooting, and tailored maintenance solutions through “evergreen” contracts, including 24/7 emergency service and proactive preventative maintenance).

Energy Efficiency Solutions (customized solutions to secure funding, reduce operating costs, and maintain energy-efficient facilities).

Decarbonization Roadmaps (customized strategies developed through consulting and engineer-led assessments to achieve carbon reduction goals).

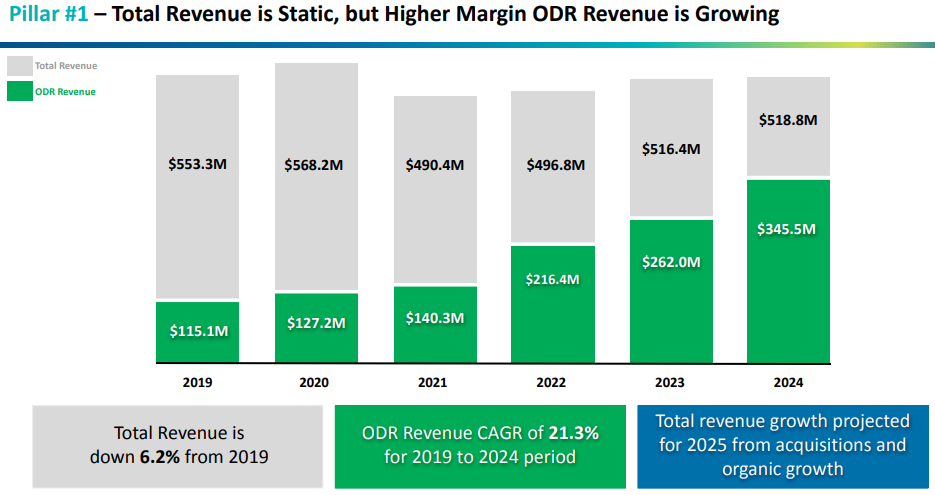

ODR FY24 Financial Performance

Revenue Growth: Increased by 31.9% to $345.5M for 2024, compared to $262.0 million in 2023.

Gross Profit Percentage: Increased to 31.2% in 2024 (up from 29.0% in 2023), driven primarily by the mix of higher margin work and material gross profit write-ups.

Backlog: Increased to $225.3M as of December 31, 2024 (up from $147.0M in 2023). The Company estimates 86% of this backlog will be recognized as revenue during 2025.

General Contractor Relationships (GCR) Segment

The GCR segment involves new construction or renovation projects (MEP services) awarded by general contractors or construction managers.

GCR Strategic Shift: The Company is actively reducing risks and exposure to large, complex, non-owner direct projects. Current management believes the historical industry pricing and associated risks for this type of work do not align with stakeholder expectations. Efforts are focused on improving project execution and profitability by pursuing opportunities that are smaller in size and shorter in duration where the Company can leverage its captive design and engineering services.

GCR services are provided through two methodologies:

Plan & Spec Bidding: A competitive bid process where price is the predominant selection criteria.

Design/Build or Design/Assist: Selection is based on "best value methodology," prioritizing qualifications and project approach, and secondarily on select cost factors.

GCR Financial Performance (2024):

Revenue: Decreased by 31.9% to $173.3M for 2024, compared to $254.4M in 2023. This decrease is primarily due to the Company’s continued focus on the mix-shift strategy towards ODR.

Gross Profit Percentage: Improved to 21.1% in 2024 (up from 17.0% in 2023), mainly due to the Company becoming more selective in pursuing projects.

Backlog: Decreased to $140.0M as of December 31, 2024 (down from $186.9M in 2023). This reduction is intentional, supporting the focus on higher margin projects. The Company estimates 72% of this backlog will be recognized as revenue during 2025.

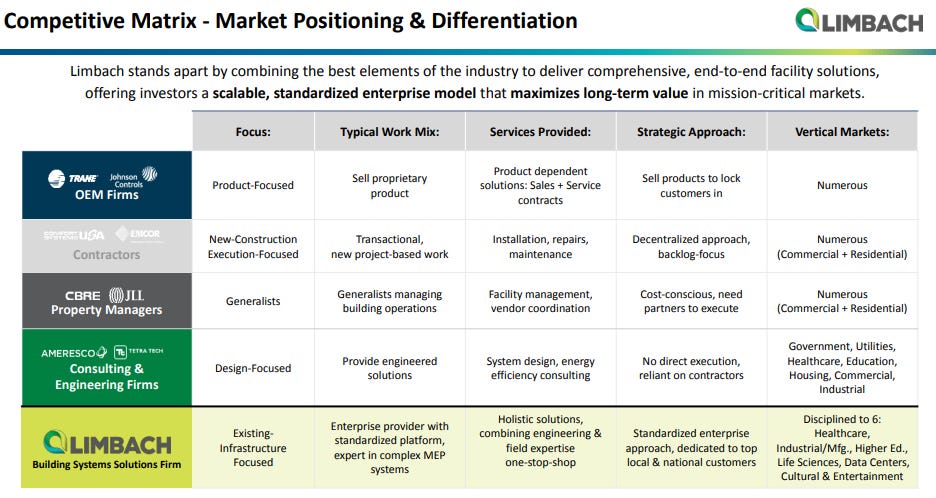

Competitive advantage

Growth Through Acquisitions

The Company seeks to increase cash flow and operating income by acquiring strategically synergistic companies that support the ODR growth strategy, increase the geographic footprint, address capability gaps, and enhance the breadth of offerings. In 2024, the Company completed two significant acquisitions with a third one in 2025:

Kent Island Mechanical, September 3, 2024, a provider of building systems solutions in the Greater Washington, DC metro area. The acquisition expands market share within the existing operating footprint and supports continued ODR growth.

Consolidated Mechanical, December 2, 2024, a premier provider of mechanical, steel fabrication, and maintenance services to owners of complex process systems in the industrial sector. The acquisition extends reach into the industrial sector, including power generation, food processing, manufacturing, and metal markets in Kentucky, Illinois, and Michigan.

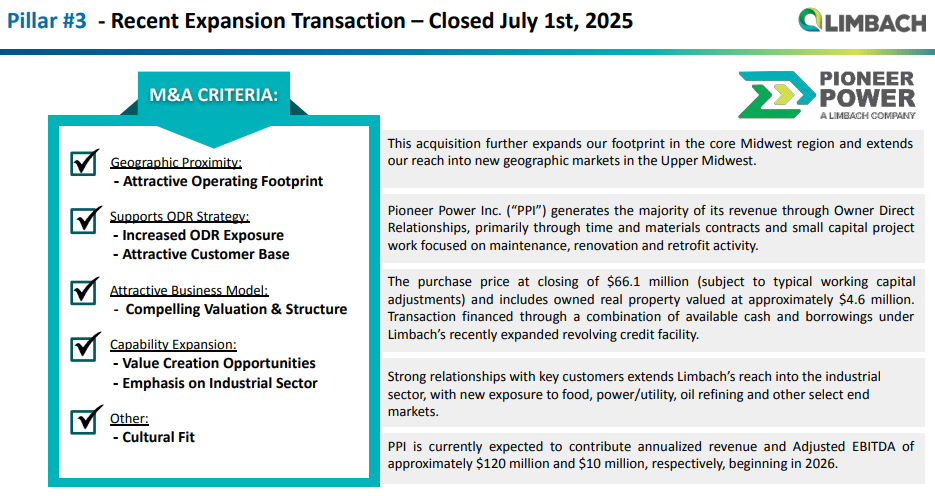

Pioneer Power Solutions

The Company’s ODR revenue increase in 2024 was also positively affected by approximately $31.5M from the ACME Industrial Piping, LLC and Industrial Air, LLC transactions, as these entities were not acquired for the full year ending December 31, 2023.

Operational and Regulatory Environment

Backlog Definition: Backlog is defined as the estimated revenue on uncompleted contracts, including contracts for which work has not yet begun, less the revenue recognized.

Competitive Factors: The industry is highly competitive and fragmented. The Company competes on factors including cost efficiency, reputation and quality of service, technical expertise, geographic reach, financial strength, availability of craft labor, and customer relationships. The Company must adapt to evolving trends such as increased demand for energy-efficient systems, sustainability initiatives, and advancements in automation.

Materials and Costs: Operations rely on a wide range of materials and equipment, primarily sourced domestically. Costs can fluctuate due to market conditions, global supply chain disruptions, and changes in commodity pricing. Tariffs, such as those announced by the U.S. government on imported steel and aluminum in February 2025, could result in increased costs, although the short sales cycle of the ODR segment often allows these costs to be passed onto the customer.

Seasonality: Severe weather can impact productivity in construction projects, shifting revenue recognition to later periods. Mild weather tends to reduce demand for maintenance services, while severe weather may increase demand for maintenance and time-and-materials services.

Regulatory Compliance: The Company is subject to federal, state, and local laws related to the environment (e.g., discharges, waste handling) and workplace safety (e.g., OSHA, wage and hour). The Company is also subject to laws related to unionized labor, as a large portion of its business uses labor provided under collective bargaining agreements.

Stay tuned for our Quick Take discussing recent developments, financials and prospects for the shares.