A Primer on Richardson Electronics

Our handy overview

Introduction

Richardson Electronics (RELL) is a provider of niche industrial solutions often developed in partnership with specific customers. It reports in four segments.

In short

A recovery in the wafer equipment market where Lam Research is Richardson’s biggest customer is expected for H2/24 getting revenue to double from the present low of $20M and producing gross margin expansion.

The company’s GES segment collapsed in Q2/24, but business is project-based and there are huge opportunities with ultracapacitors for wind turbines, magnetrons for synthetic diamond and hydrogen production, batteries, superstructure and ultracapacitors for electric and/or diesel locomotives and the like.

Management believes that the GES segment will be the secular growth driver propelling the company to $500M+ in sales in a couple of years.

Strategy

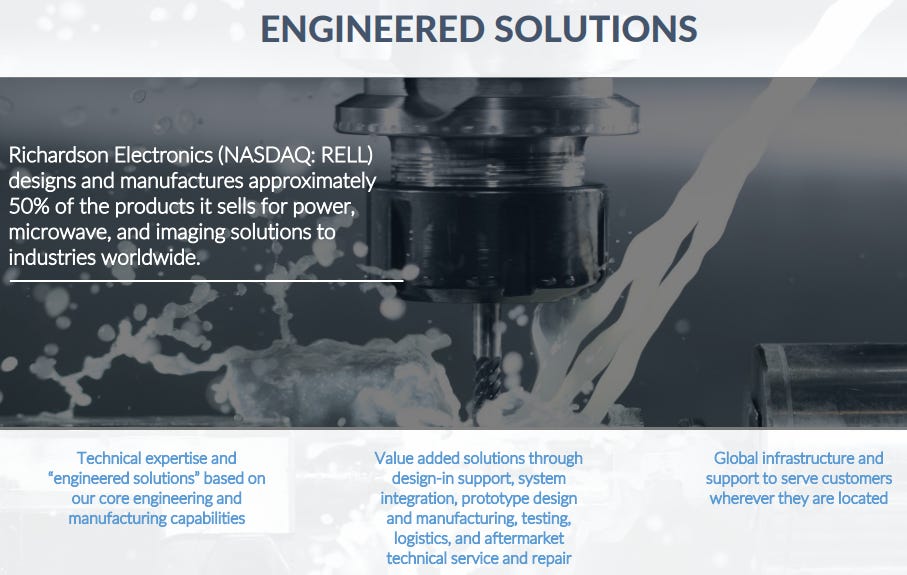

The Company provides engineered solutions for customers, adding value through design-in support, systems integration, prototype design and manufacturing, testing, logistics, and aftermarket technical service and repair through its global infrastructure. These engineered solutions are based on their core engineering and manufacturing capabilities and often lead them to identify new opportunities.

Richardson also produces a host of proprietary products like thyratrons and rectifiers, power tubes, ignitrons, magnetrons, phototubes, microwave generators, Ultracapacitor modules, and liquid crystal display monitors.

Distribution agreements where they have longstanding global deals with a host of suppliers that benefit from its global reach. As a result, the company holds substantial inventory of over 100K SKUs.

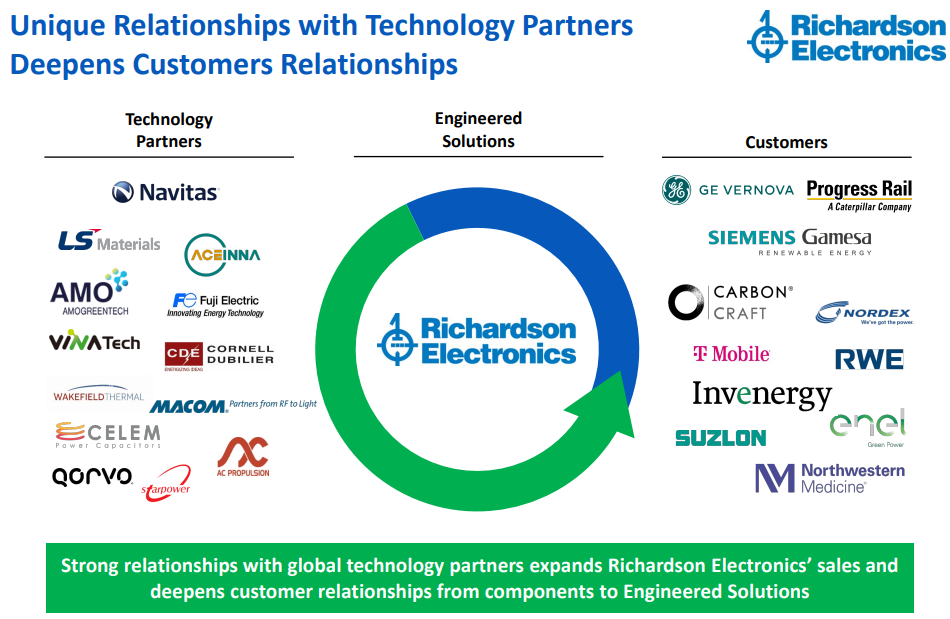

Technology partnerships

The latest technology partners are Navitas, MWD, Quantic Electronics, new RF and Microwave technology partners, and Ideal Power.

Segments

Canvys: custom displays for medical and industrial OEMs

PMT

Consists of two sub-segments:

The Electron Device Group (EDG) is the legacy tube and semiconductor wafer fab equipment business.

The RF and Microwave Group (PMG).

The largest customer is Lam Research (LRCX), which uses Richardson products for the production of semiconductor wafer fabrication equipment but there are other, smaller customers here like Tokyo Electron and Applied Materials.

This business is cyclical, went from$40M in FY23 to under $20M in FY24 but an upturn is underway in CA25.

GES

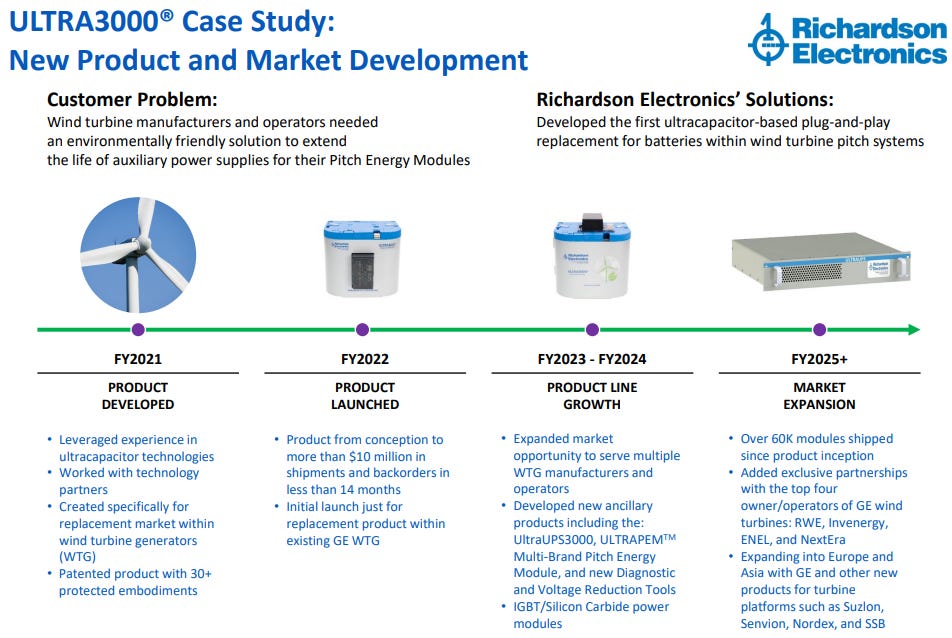

The ULTRA3000 is a patented ultracapacitor specifically engineered to replace lead-acid batteries in GE wind turbines.

The company serves the top four owner-operators of GE Wind Turbines in North America, RWE, Invenergy, Enel, and NextEra but is also growing this program globally, expanding into Europe and Asia with GE. The company has shipped some $30M of ULTRA3000 to date (Q2/25).

The ULTRAPEM3000 is similar to the ULTRA3000 but meant for other brands like Suzlon, Senvion, SSB and Nordex.

The ULTRAPEM3000 is in exclusive beta testing at Suzlon of India, but as replacement and OEM solution. This is a 7K exclusive opportunity in India alone and 2K more in the US (for which they already received orders), a $34-$50M opportunity.

The patented ULTRAGEN3000 is a GSM (Generator Start Module) for wind turbines but can also be used in electric and diesel locomotives, where it has no competition. They have 25 orders already from two of the top OEMs.

The ULTRAGEN3000 (Q2/24CC): ”in beta testing with several refrigeration truck manufacturers where the ULTRAGEN is replacing lead acid batteries. There are currently 500,000 refrigeration trucks in North America and we estimate this market opportunity to have a TAM of $200 million.”

The ULTRAGEN3000 also has a host of additional applications construction equipment, excavators, loaders, and backhoes.

The patent-pending ULTRAUPS3000 is a Hybrid Ultracapacitor UPS (Uninterrupted Power Supply) for wind turbine control systems and other industrial applications.

It is in beta testing, which is going "very, very well" according to management (Q2/24CC): “The ULTRAUPS 3000 will be used by Siemens and by other owner-operators of GE wind turbines going forward.”

For Siemens, only one module per turbine is required but it's 5x as expensive as the ULTRA3000. As a reminder from the Q3/23CC: “we've only retrofitted about 10% of the 30000 GE wind turbines that are in the United States and Siemens has 10 times that many.”

Microwave generators for producing diamonds with demand for the YJ1600 far outstripping the company’s production capacity with 5K in backlog per the Q4/23CC. They sell for roughly $3K a piece (at 35% gross margin) so that’s $15M in backlog. They also produce a stream of recurring revenue for replacement tubes, that last about two years.

Microwave generators for producing hydrogen and acetylene, which is more valuable so the hydrogen is basically free, it's a very profitable way to generate hydrogen. This is a much bigger generator, selling at $100K and the tube is a $10K item, but no word on orders yet.

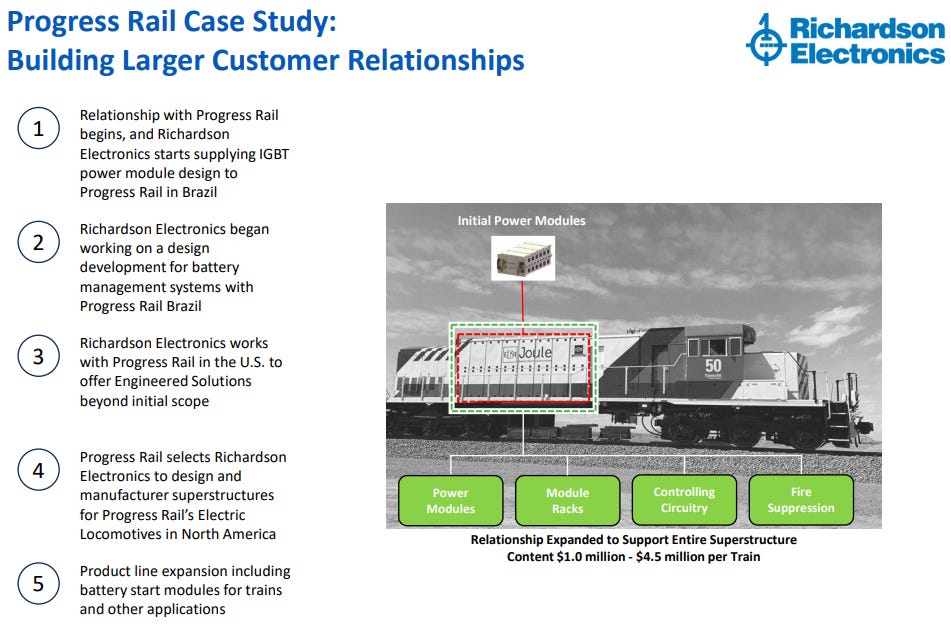

Electric locomotives designed, manufactured, tested, and built lithium-ion phosphate battery modules battery modules, and superstructures (battery compartments) for its partner Progress Rail, “meeting and exceeding all their requirements” (Q2/24CC). These were just prototypes but still amounted to $24M in revenue. Management expects orders to come in in H2/24 and this could easily be a $100M+ opportunity.

But there are additional opportunities (see slide above). Progress Rail has two customers, one in Australia and Long Island Railroad and these projects are for starter modues for the two largest owner-operators of diesel locomotives.

However (Q3/23CC) “They are 25000 or they are about locomotives -- diesel locomotives in the United States, about half of them are Progress Rail and everyone has a battery start and those units are anywhere from $1200 a piece to $5000 a piece and we're providing prototypes for those units as we speak.”

States like California are mandating a transition from diesel locomotives so there is a regulatory tailwind.

Healthcare

Richardson Healthcare manufactures, repairs, refurbishes, and distributes high-value replacement parts and equipment for the healthcare market. Their customers include hospitals, medical centers, asset management companies, independent service organizations, and multi-vendor service providers.

The products offered by the Healthcare division include: diagnostic imaging replacement parts for CT and MRI systems, replacement CT and MRI tubes,

CT service training, MRI and RF amplifiers, hydrogen thyratrons, klystrons, magnetrons, flat panel detector upgrades, pre-owned CT systems, additional replacement solutions under development for the diagnostic imaging service market.

Richardson Healthcare focuses on providing a combination of newly developed products, partnerships, service offerings, and training programs to help its customers improve efficiency while lowering the cost of healthcare delivery.

The division has seen growth in its CT tube business, particularly with the repaired Siemens Straton Z tubes and their proprietary ALTA tubes. They are also working on a repair program for the Straton MX, MXP, and MX-P46 tubes.

The company derived some $20M/y in tubes from Talus but they are going to close down in the coming 2-3 years leading Richardson to build up a $30M inventory, adding another $5M in CA25, and then start to draw down the inventory and finding a replacement for Talus.

Revenue can be choppy quarter-to-quarter (+48.8% to $3.8M in Q1/25, -22.8% to $2.3M in Q2/25) but margins stayed well in the 30s.

Management is considering strategic alternatives for the healthcare business.

Canvys

Canvys engineers, manufactures, and sells custom display solutions to OEMs across global industrial and medical markets. These solutions include touch screens, protective panels, custom enclosures, all-in-one computers, specialized cabinet finishes, and application-specific software packages and certification services. Canvys' products are used in a variety of applications:

Medical applications include optical coherence tomography (OCT), intravascular imaging, pulsed-field ablation, computer radiography, lithotripsy, cataract surgery, medical device control, radiotherapy, microwave ablation, and robotic-assisted surgery.

Commercial and Industrial applications include passenger information systems within trains and buses, and human-machine interface (HMI) technologies used in printing, vending, milling, and packaging machines.

Revenues declined considerably to $14.5M (from $17.2M in H1/24) in H1/25 but margins held up

Financials

Revenue, big dip in CY23 as the semiconductor wafer fab business was in a cyclical downturn and a number of GES projects got stalled:

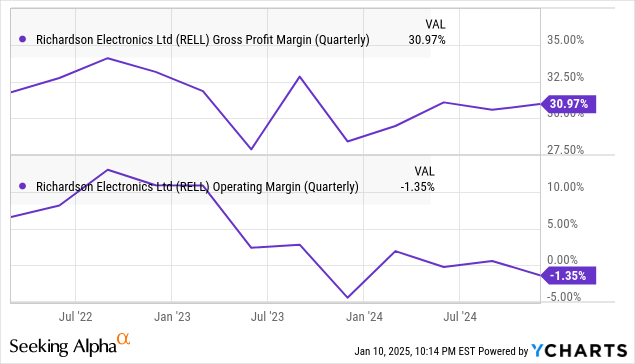

Margins:

Cash flow, pretty decent recovery mostly on inventory draw dawn (inventories peaked at the end of 2023):

The company has a clean balance sheet with $26.6M in cash at the end of Q2/25 and even pays a small dividend.

Investment case

The investment case depends mostly on its unique business model, strong GES growth and a cyclical recovery in its semiconductor wafer equipment business that took EPS to $1.55 in FY23 when GES was still embryonic. This time around GES will add to earnings.

https://finviz.com/published_idea.ashx?t=RELL&f=011025&i=RELLd191497789i