A Primer on Silicom

The recent share outbreak is notable

Primers are to help familiarise with the business model, competitive position and moving parts.

Company Overview

Silicom is a provider of high-performance networking and data infrastructure solutions designed to optimize efficiency in Cloud, Data Center, and Edge environments.

The company’s solutions serve as the infrastructure backbone for workloads including AI inference, SD-WAN, SASE, cyber security, and fabric switching.

The business operates primarily through a “Design Win Model,” involving evaluation and qualification phases that can take 12 months or more before moving to full-scale deployment.

As of March 2026, the company employed 123 personnel dedicated to research and development across Israel, Denmark, and the U.S..

Growth Engines

Management has identified three structural shifts in technology as primary growth drivers:

AI Inference Solutions: The company is focusing on the transition from training-centric to inference-driven AI models. Its FPGA-based solutions target the latency wall (bottlenecks between components) and the hardware lottery (the limitations of rigid architectures), allowing customers to adapt hardware to new algorithms in near real-time.

Post-Quantum Cryptography (PQC): Driven by the security risks quantum computing poses to current encryption, Silicom provides hardware-based accelerators. Their FPGA approach offers crypto-agility, allowing for hardware updates as new cryptographic standards evolve.

White-Label Switching (WLS): Silicom is capitalizing on the trend of disaggregation, where network operators move away from proprietary hardware toward flexible, cost-efficient white-label platforms.

Core Products

Server Network Interface Cards (NICs): High-speed adapters that facilitate communication between servers and switches, often including bypass functionality to ensure traffic continuity during failures.

Smart Cards: Programmable adapters that offload tasks from the CPU, such as encryption and data compression. Specialized FPGA-based cards are used for packet capturing and High-Frequency Trading (HFT).

Smart Platforms (Edge Products): Full computing platforms used as Customer-Premises Equipment (CPE) for SD-WAN, SASE, and NFV deployments.

Market Trends

Disaggregation and Decoupling: The industry is moving toward separating hardware from software, which has increased demand for Silicom’s Edge devices and Smart Cards.

Core Competition: Major competitors in the server adapter space include Nvidia, Intel, and Broadcom, though Silicom differentiates itself through customization for smaller and mid-sized accounts.

Competitive advantage

Customization. Silicom’s ability to customize off-the-shelf hardware into proprietary solutions gives it an edge in a market dominated by commoditized cloud infrastructure — a capability few competitors can match at scale. The typical workflow: a customer evaluates an existing Silicom product, confirms the performance, then commissions a custom variant. During the coming months after a design win, Silicom customizes the card to meet the customer’s exact specifications. This is a switching cost story in disguise. Once a customer’s appliance or system is designed around a Silicom FPGA SmartNIC or edge platform, replacing it requires a full re-qualification cycle — costly and disruptive.

White-Label / Embedded Model. Silicom’s technology becomes embedded in clients’ branded products through “white-label” partnerships. This is strategically important: Silicom becomes invisible to end customers but deeply embedded in a vendor’s product stack — making displacement even harder.

FPGA Programmability as the Technical Foundation. FPGAs are inherently flexible silicon — they can be reprogrammed for different workloads (encryption offload, packet processing, AI inference acceleration, etc.), which makes them ideally suited to Silicom’s customization model. FPGA products typically yield gross margins above the company’s 27–32% target range, providing a structural advantage as these solutions grow as a percentage of revenue.

Post-Quantum Cryptography (PQC). Silicom’s technological moat centers on its FPGA-based solutions, which generated the company’s second post-quantum cryptography design win in Q3/25. PQC represents a forward-looking requirement that most competitors have not yet commercialized.

CEO Eizenman said (Q3/25CC): “Our PQC-ready smart cards put Silicom ahead of the adoption curve, at the forefront of this future transition.” The “harvest-now-decrypt-later” threat is already driving enterprise and government procurement — Silicom having a mature, tested PQC product is a real lead over most networking hardware rivals.

One-Stop Shop. The ability to deliver both edge systems and integrated NICs creates a “one-stop shop” that major cybersecurity and SASE providers value, as evidenced by three design wins in Q2/25 alone. This integration capability differentiates Silicom from pure-play component suppliers and supports pricing power in a commoditized networking market. With over 400 active design wins and 300 product SKUs as of 2025, Silicom’s portfolio spans industries. The breadth of the SKU library means customers can often start with an off-the-shelf product and expand, lowering Silicom’s cost of winning new business over time.

Performance-focused niche. Its products target throughput, latency reduction, offload, and acceleration for cybersecurity, SD-WAN, data center, and edge use cases, where product performance matters more than commodity pricing.

Design Win Flywheel. With 400+ active design wins and 200+ customers, the business can turn technical success into recurring production revenue over time. Recent wins suggest the moat may be strengthening through deeper OEM partnerships, especially in Edge, SmartNIC, and security applications. Silicom Ltd. serves over 200 OEMs. Each design win is a long-duration revenue stream (typically 3–7 years). The company’s pipeline as of Q1/26 is described by management as “the strongest and most expansive” on record, spanning Edge systems, SmartNIC, and FPGA-based solutions.

Growth Market Competition: In AI and PQC, Silicom competes with specialized hardware vendors like Napatech, Avantech, and BittWare, as well as the internal engineering teams of potential customers who may choose to build solutions in-house.

Key Risks to the Moat

Customer concentration. The top three customers generated 28% of FY25 revenue, and one alone accounted for 14%. A large customer loss can be painful.

Technology displacement risk. Management highlights risks from potential integration of adapter functionality directly into servers — i.e., if server SoCs absorb more networking functions, the standalone SmartNIC market could shrink.

Long sales cycles. Design wins take time to ramp. New growth opportunities are still in early stages and not expected to contribute significantly to 2026 revenues.

Scale. Silicom is a $100M-ish revenue company competing in a space with Marvell, Broadcom, and Intel/Altera operating at a completely different scale. Its moat is real in the custom/OEM niche, not in high-volume commodity networking.

Manufacturing and Operations

Supply Chain: While Silicom uses standard components, it is dependent on key single-source or limited-source suppliers, including Intel and Broadcom.

Facilities: The company operates manufacturing and R&D facilities in Yokne’am and Kfar Sava, Israel, as well as offices in Denmark and the United States (New Jersey and Virginia).

Conflict Minerals: The company is subject to due diligence and reporting requirements regarding conflict minerals, which may impact supplier availability and engineering costs.

FY25 Performance

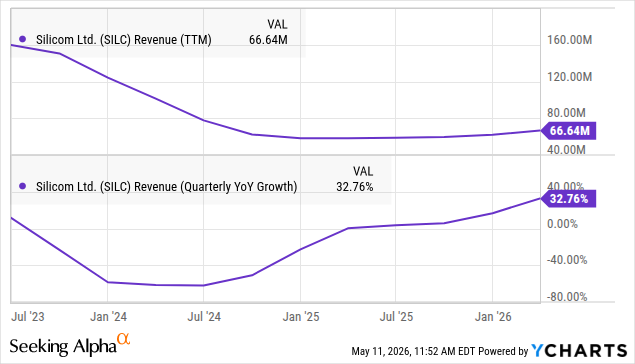

Total Sales: $61.9M, a 6.6% increase from $58.1M in FY24. This increase reflects a resilient core business and the initial ramp-up of new design wins.

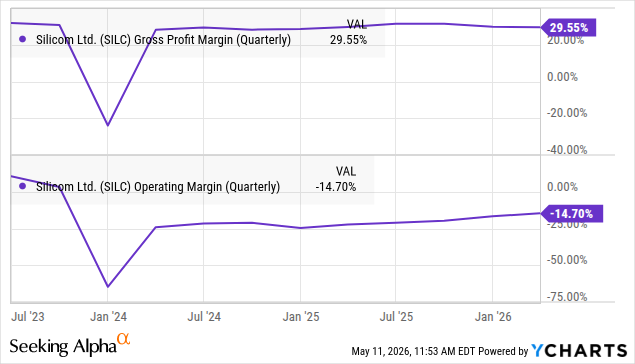

Gross Profit: $18.9M, representing a 30.6% margin (up from 28.6% in FY24). The improvement was driven by a more favorable product mix and lower inventory write-downs.

Operating Loss: 19.8% of sales, an improvement from a 22.8% loss in 2024.

Net Loss: $11.5M, compared to a $13.7M loss in the prior year.

R&D Investment: $20.1M, which constitutes approximately 32.4% of total sales.

Geographic Sales Distribution: North America accounted for 74% of sales, followed by Europe (18%) and Asia-Pacific (8%).

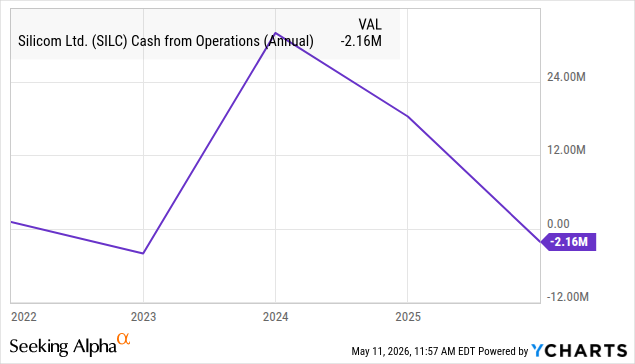

Cash and Marketable Securities: As of December 31, 2025, the company held approximately $73.6M across cash, bank deposits, and marketable securities.

Working Capital: $85.9M with a current ratio of 4.15, indicating a strong liquidity position.

Inventory: Increased to $52.7M (up from $41.1M in FY24) to support anticipated customer orders.

Debt: The company has no long-term debt.

Stay tuned for our Q1/26 update