A Primer on Velocity Financial

Introduction

Velocity Financial (VEL) is a vertically integrated real estate finance company. Its business model involves originating, securitizing, and managing a nationwide portfolio of loans secured by real estate (primarily 1-4 unit residential rental properties and commercial properties) to generate attractive risk-adjusted spreads for their shareholders.

The company largely serves investors that are somewhat less interest rate sensitive and put a premium on certainty of execution.

Velocity originates loans through an extensive network of independent mortgage brokers and direct borrower relationships.

The company has been growing steadily, and unless there is a significant downturn in the housing market, this is unlikely to change anytime soon.

Business model

The company makes money through:

NIM (net interest income, the interest income minus interest expense on debt used to fund the loans).

Gain on Sale of Loans.

Upfront Loan Origination Fees.

Unrealized Gains/Losses on Fair Value Loans, accounting for some loans at fair value, recognizing unrealized gains/losses based on market value changes.

Other Income from activities like loan servicing fees and income from real estate-owned properties.

Sources of funds

Securitization of Loans by pooling their originated loans and selling bonds to third-party investors through securitization trusts. These securitizations are typically fixed-rate.

Warehouse Facilities (lines of credit) are used as a short-term funding mechanism for newly originated loans, aggregating these loans until a sufficient volume is reached for a securitization. These warehouse lines are floating rate and tied to SOFR.

The company has also utilized corporate debt as a source of funds.

Sources of equity include retained earnings, and the ATM is sometimes used.

Velocity holds a portion of the bonds from their securitizations, which can be sold to fund future growth.

Securitization

New loan originations are typically financed using warehouse facilities, which are short-term borrowing arrangements.

Once Velocity has originated between approximately $175 million and $300 million in new loans, they pool these loans together to be securitized. This pool of loans is then structured into a real estate mortgage investment conduit (REMIC). A REMIC is a special purpose vehicle that holds a fixed pool of mortgages and issues multiple classes of interests in these mortgages to investors.

Through individual trust vehicles, Velocity issues bonds to third-party investors. These securities represent claims on the cash flows generated by the underlying pool of mortgage loans. The issuance is generally done as private placements pursuant to Rule 144A under the Securities Act. This means the securities are offered and sold only to qualified institutional buyers.

The majority of Velocity's securitizations utilize a REMIC structure.

For financial reporting purposes (U.S. GAAP), each REMIC is considered a variable interest entity and is consolidated in Velocity's financial statements. The securitization is accounted for as a secured borrowing, meaning the loans remain on Velocity's balance sheet, and the issued securities are treated as debt.

For tax purposes, the REMICs are treated as a sale. This can result in Velocity recognizing taxable income or loss based on the difference between the fair market value and their cost basis of the REMICs, potentially creating deferred tax assets or liabilities.

Velocity, through its wholly-owned subsidiaries, is the sole beneficial interest holder of each of the trusts created for the securitizations. This means they retain certain rights and risks associated with the underlying loan pool.

The proceeds from the sale of the securities to investors are then used to pay down the outstanding balances on Velocity's warehouse facilities, effectively refinancing the short-term debt with longer-term funding.

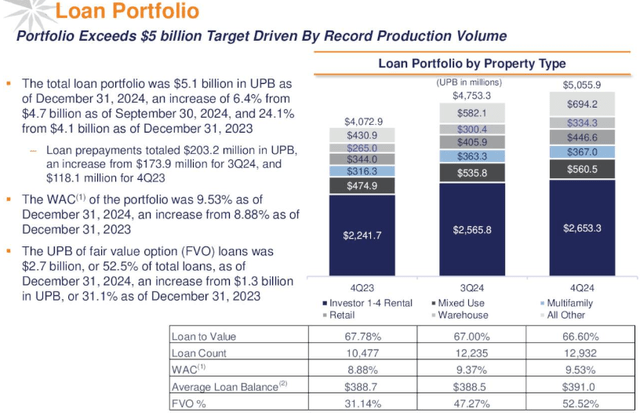

Loan Production and Portfolio

Velocity is showing impressive growth in loans, especially for commercial properties:

Its loan portfolio now exceeds $5B (UPB stands for unpaid principal balance):

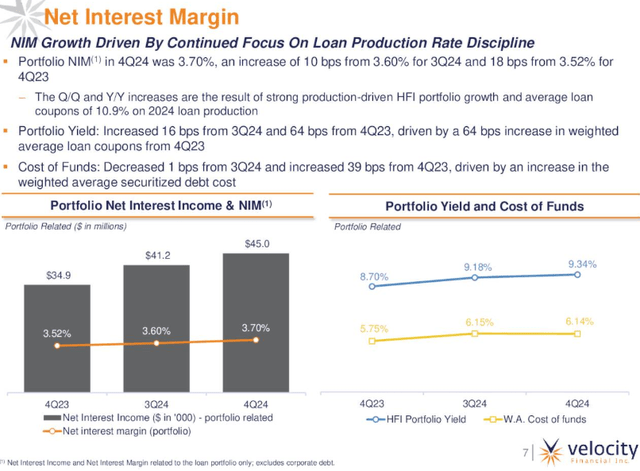

NIM

The NIM (net interest margin) is obviously a crucial variable for the company's profitability and is a function of the WAC (Weighted Average Coupon) on new loan originations and the weighted average of the cost of funds, which is influenced by:

Improvements in the securitization market can lead to tighter spreads.

Changes in these base rates can affect the cost of short-term (warehouse) funding, which flexible rate and linked to SOFR, even if management argues that its business is less rate-sensitive than other mortgage segments.

The interest rate on any corporate debt.

Some additional factors come into play:

A strong loan production allows Velocity to add more of the higher-yielding, newly originated loans to its portfolio, which can drive up the overall portfolio yield and improve the NIM.

Portfolio Yield (the average rate of return on Velocity's entire loan portfolio) is influenced by the WAC of both new and existing loans.

While not directly part of the NIM calculation, NPLs (Non-Performing Loans) can negatively impact overall profitability by reducing the interest income generated by the portfolio. However, Velocity's effective NPL resolution efforts, which often result in gains, can mitigate some of these negative effects.

Given that its funding costs are largely fixed rate one might be inclined to think that Velocity would be sensitive to interest rate declines, but it's mortgage loans are also mostly fixed rate, from the FY23 10-K:

Our loans are structured to provide interest rate protection. The majority of our loans are fixed-rate loans and a smaller portion of our loans are floating after an initial fixed-rate period, subject to a floor equal to the starting fixed rate. The loans are mainly financed with long-term fixed-rate debt

Business strategy

There are multiple initiatives from management to grow the company

Management aims to be the preferred lender within their established network of approximately 3K+ mortgage brokers, increasing the volume from these brokers, as a large percentage of these brokers have originated a limited number of loans with them. The company is growing its team of account executives and marketing initiatives.

Expanding their network with new mortgage brokers, helped by a strong reputation and targeted sales efforts.

Developing new products beyond its primary product (a 30-year fixed-rate amortizing term loan) like the short-term interest-only loans and HUD multi-family and healthcare loans that came with the acquisition of Century.

M&A (like the acquisition of Century Health & Housing Capital).

Acquiring portfolios of loans that meet their investment criteria, opportunities tend to increase during less favourable origination conditions.

Maintaining disciplined credit standards and margins while increasing origination volume, emphasizing low loan-to-value ratios in the originations.

Leveraging its established franchise with strong brand recognition. Its 19-year history in the real estate lending community positions the company as a preferred lender for mortgage brokers due to its proven ability to execute and the track record of securitizations enhances its reputation with investors and provides efficient access to debt capital.

Utilizing customized technology and proprietary data analytics. Investments in automated systems and data analytics are seen as critical for controlling the cost of originating and managing loans without sacrificing credit quality. Access to years of proprietary data allows for efficient and effective lending decisions.

Maintaining a strong funding and liquidity position through access to diverse and durable funding sources, including securitizations and warehouse facilities with ample capacity.

Effective in-house asset management and successful loss mitigation through a hands-on management of delinquent loans and its special servicing team's ability to resolve NPLs favorably contributes to earnings and supports their overall financial stability as they grow.

Competitive advantage

Established Franchise with a strong reputation in the market for high-quality execution and timely closing, which are the most important qualities their mortgage brokers value in selecting a lender.

Successful Securitization Track Record and Market Understanding, applying the same asset-driven underwriting process to all loans in its portfolio, regardless of whether they originate or acquire them. Their credit and underwriting philosophy encompasses individual borrower and property due diligence, taking several factors into consideration.

Access to 19 years of proprietary data allows them to perform analytics that inform their lending decisions efficiently and effectively, crucial for controlling the cost to originate and manage loans without sacrificing credit quality.

Its existing loan portfolio provides a significant and stable income stream for future growth. The majority of their loans are fixed-rate, and they are mainly financed with long-term fixed-rate debt, resulting in a spread that could increase over time but not decrease.

Direct management of individual loans is critical to minimizing credit losses. They have a dedicated asset management team that focuses exclusively on resolving delinquent loans, often resulting in favorable gains. This hands-on approach, combined with outsourced servicing relationships, is seen as a distinct competitive advantage.

Their organic growth strategy relies heavily on further penetrating their existing network of mortgage brokers and expanding it with new brokers.

By originating loans through an efficient and scalable network of approved mortgage brokers, they maintain a wide geographical presence and a nimble operating infrastructure capable of reacting quickly to changing market environments.

Velocity operates in a large and highly fragmented market with substantial demand for financing and a limited supply of institutional financing alternatives. They specifically target a niche consisting of investor real estate loans across 1-4 unit residential rental and small commercial properties, where banks are currently limiting their lending.

Velocity offers competitive pricing to their borrowers by pursuing low-cost financing strategies and by driving front-end process efficiencies through customized technology designed to control the cost of originating a loan.

Its business model is described as less rate sensitive than other mortgage segments, allowing them to successfully originate loans in both higher and lower rate environments over the last 20 years.

A main reason is that its customers are primarily brokers and borrowers recognize the reliability and the certainty of execution Velocity provides. This is particularly important for borrowers who need to close on properties by a certain date. These investors are focused on acquiring and managing properties and view interest rates as a cost of doing business. This contrasts with homebuyers who can be more rate-sensitive and may delay or forgo purchases based on interest rate fluctuations.

The company offers unique products like the 30-year fixed-rate amortizing term loan, which is highly valued by its borrower base and may not be a standard offering from other lenders in this space.

Velocity primarily finances its loan portfolio with securitizations, which are a form of long-term fixed-rate debt, matching the duration of its assets (fixed-rate loans) with the duration of its liabilities (fixed-rate securitized debt), helping to mitigate the impact of interest rate mismatches.

Velocity operates in a substantial part in an underserved niche servicing individual investors owning ten or fewer properties, where demand is high and the supply of institutional financing alternatives is limited. Limiting the direct rate competition compared to the more traditional residential mortgage market allows Velocity to maintain its margins even during interest rate changes.

NPL resolutions

Velocity Financial achieves Non-Performing Loan (NPL) resolutions through a multi-faceted approach primarily managed by its special servicing department and in-house asset management team. Here's a breakdown of the process:

A proactive approach aiming to resolve delinquencies early and mostly (90% in Q4/24) directly with the original borrowers.

In cases where the borrower cannot resolve the delinquency, the process may proceed to foreclosure. Velocity's asset management team then takes a hands-on approach to manage these assets (Real Estate Owned or REO).

Velocity actively works to sell the REO properties it acquires. The goal is to preserve the value of the assets and minimize losses, often resulting in net gains. The REO from the 1-4 unit residential side tends to be liquid and relatively easy to sell due to potential appeal to both investors and owner-occupiers.

Sometimes, even during the foreclosure process, a resolution occurs when a different investor comes in and buys the property. In such cases, Velocity can be satisfied up to the total amount owed, including costs and fees. Velocity states they have not sold delinquent loans to distressed debt buyers as part of its strategy.

Across all resolution methods, Velocity's efforts aim to achieve favorable gains on the resolution of its NPL loans. They have consistently averaged a gain on NPL resolutions over the past several quarters.

Valuation

Adjusted book value per share is the GAAP book value per share ($15.70 in Q4/24) plus a management estimate that includes the potential impact of marking assets carried at amortized cost to their fair value ($18.73 in Q4/24).

There are 749K options and 403K RSUs outstanding for a fully diluted share count of 34.6M, at $20 per share yields a market cap of $692M. The shares are cheap on an earnings basis, trading at a single digit p/e with analyst FY25 EPS expectations of $2.22.

What makes the company special

It operates in both commercial and single housing, bought mostly for investment purposes, making borrowers somewhat less price sensitive and placing more value on swift execution.

The company has an extensive network of brokers, creating a nimble, capital-light business.

Velocity is somewhat less interest rate sensitive than other mortgage lenders (see below).

The company has a strong NPL solution mechanism.

Concerning less interest rate sensitivity compared to other mortgage lenders, this comes from:

Velocity's focus on a less rate-sensitive borrower base where supply is more difficult to attain.

Its provision of long-term fixed-rate financing.

Its strategy of matching asset and liability durations through securitization

Its presence in an underserved niche

Its reputation for reliable execution contributes to its business being less directly impacted by fluctuations in interest rates compared to lenders primarily focused on the traditional homebuyer market.

From the Q4CC:

Our customers tell us that banks are limiting their lending in our target niches and we believe that we will continue to allow -- that will allow us to capture market share.... Unlike, I mean unlike most mortgage lenders the first question or the first concern is not rate with our borrowers it's certainty of execution.

Given that its funding costs are largely fixed rate one might be inclined to think that Velocity would be sensitive to interest rate declines, but it's mortgage loans are also mostly fixed rate, from the FY23 10-K:

Our loans are structured to provide interest rate protection. The majority of our loans are fixed-rate loans and a smaller portion of our loans are floating after an initial fixed-rate period, subject to a floor equal to the starting fixed rate. The loans are mainly financed with long-term fixed-rate debt