A Quick Take on Cerence

We like companies with rising cash flow..

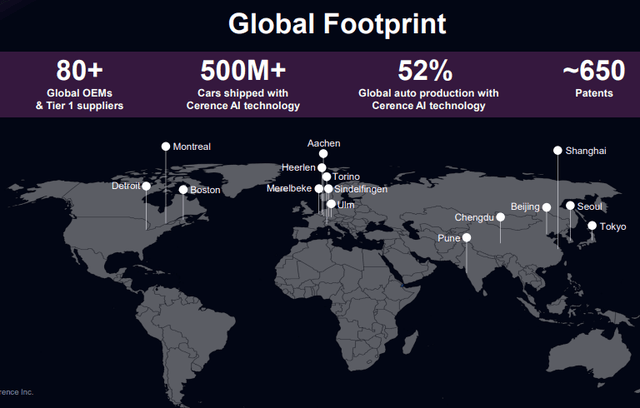

Cerence is the market leader in automotive virtual assistants, with a vast installed base and strong relationships with major OEMs and Tier 1 suppliers.

The business model is attractive and increasingly focused on high-margin, recurring revenues from connected services and usage-based models, producing increasing PPUs.

Growth drivers include expansion into new markets, higher price per unit deals, and innovation with the xUI AI platform and proprietary language models.

Despite recent revenue headwinds from business model shifts and auto industry challenges, underlying metrics like variable license revenue show robust momentum.

We are impressed with the increase in cash generation and think more investors should be, and indeed, the shares are up 20%+ since we rated them a buy for our Investor group at Seeking Alpha a couple of weeks ago.

Cerence (CRNC) is the market leader in virtual assistance for the transportation market. It has an attractive, high-margin, scalable business model, and it's moving beyond its core automotive market to markets like TVs and call centers.

Market leader

The company is the market leader with an enormous footprint, applied in 500M+ cars already. This has both advantages and disadvantages:

The company is well established and entrenched, working with nearly all automotive OEMs and their Tier 1 suppliers.

With such a large installed base, it becomes harder to grow, although there is the new car market.

Product innovation is not only necessary to generate additional revenue, it also defends the company's leading competitive position.

Attractive business model

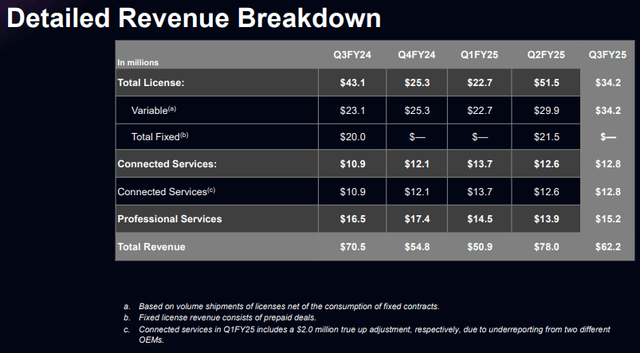

The company generates most revenue through high-margin license revenues, which usually have a one-time fixed, as well as a variable component. The fixed payments are one-off, so they create lumpiness in q/q revenue:

In addition to these attractive license revenues, there are also recurring subscription services (from cloud, which are a growing proportion of revenues), see our Primer for more details.

Maintenance and support contracts also generate recurring revenues.

The company recorded $0 in fixed license revenue in Q3, compared to $20M in Q3/24. This is part of a deliberate strategy to move toward more recurring, usage-based revenue models.

Growth

Growth comes from:

New customers

New cars

Adjacent verticals

New markets

Increasing PPU

Customer Growth and Design Wins

The recent deal with the Volkswagen Group will utilize xUI as the basis for its next-generation system. The linked PR shows some nice use cases.

Work with JLR (Jaguar Land Rover) was expanded to bring more generative AI capabilities to its current platform while co-developing a future xUI-based experience.

Cerence is seeing an increased Price Per Unit (PPU) with these new xUI deals.

Six major customer programs started production in Q3, including BYD, smart, Audi, Geely, Mahindra, Nissan, and PSA.

AI Roadmap and xUI Platform

The company has to maintain its position at the forefront of technology to win new customers and maintain and expand with existing ones; no surprise, new product development is an important part of the growth strategy.

Cerence xUI is the next-generation hybrid Agentic AI assistant, which the company is developing. It is on schedule with its multiyear roadmap, with recent milestones like increased language availability and advanced contextual reasoning.

The platform is set to be showcased at the International Auto Show in Munich in September.

The company is also developing its own agents (for stuff like real-time knowledge, integrated navigation/EV charging) and allows OEMs to integrate their own.

The proprietary CaLLM (Cerence Automotive Large Language Model) family of language models acts as an orchestrator to ensure a seamless user experience across different agents, from the Q3CC:

Our calm family of proprietary language models is critical to this effort, enabling streamlined interoperability by serving as the orchestrator that helps ensure a consistent behavior and seamless integration across agents to deliver a seamless user experience. And we believe that the flexibility and openness of our architecture alongside our unmatched automotive expertise continue to be differentiators for Cerence, especially as OEMs navigate the complexity and ambiguity of the current market while still looking for ways to improve the user experience in their vehicles.

Additional verticals and markets

Moving beyond automotive is another way to grow the TAM and revenue. Given that the core capabilities have a much wider application, this should be possible in principle.

For starters, the company can leverage its core technology to enter other transportation markets such as two-wheel vehicles, trucks, public transit, and fleet vehicles.

But the company can also move beyond the automotive and adjacent markets, and that's what management has been doing. For instance, a new partnership was formally announced with LG to use Cerence's text-to-speech (TTS) technology to power voice interaction in its global television lineup.

Cerence is also developing a call center agent focused on service-related automotive interactions, with potential applications in other industries. Then there are self-service kiosks, in partnership with Code Factory.

Given that these are significant expansions of the TAM, these developments are promising. However, the company is a new entrant in these markets, so any revenue impact is expected in late FY26 and beyond.

Non-auto verticals like televisions will likely have a lower PPU but much higher volumes than automotive, and this will be additive revenue. Even better, it is not expected to require an increase in operating expenses, as growth will be funded by internal productivity gains, from the Q3CC:

No, I do not expect OpEx growth. I mean, for example, Tony and I did a review today on how we're becoming more efficient by using artificial intelligence internally to help us write our code to do some of our Q&A work, to build more tools that allow us to do analytics against our software at a much faster rate. So we think there's just in there, we can get 15% to 20% productivity improvement within our engineering team just by doing that work over the next year and expanding that to a broader.

Increasing PPU

The trailing 12-month PPU (Price Per Unit) increased to $4.91, up from $4.47 in the prior year, driven by better pricing and higher adoption of connected solutions, so there is considerable land-and-expand going on, which greatly helps underpin growth.

The PPU increase was driven by higher volumes on the embedded side, related professional services revenue, and catch-up "true-ups" from customer royalty reporting, from the Q3CC:

We've talked about this before. Remember that our customers self-report their royalty volumes. And so we have to accrue a certain amount until we get those royalty reports. And in some periods, we have catch-up kind of true-ups to what we've accrued to what this actually came in. So we also had some additional true-ups, which impacted the embedded line and the professional services line as well. And those are normal for the business, but they -- I think they were a little bit higher than normal this quarter. And then lastly, we saw an increase in the euro exchange, the dollar that benefited all of the line items as well.

Expanding the connected services keeps this going. There have been multiple additions. Under the Car Life Suite, additions as voice-powered smart car manuals, contextual car status, dealer appointment scheduling, and car-learning modules.

Under Cerence Connect, one can mention smart home integration and IoT, and third-party integrations. Then there are additions to the Digital Twin Services, like connected vehicle digital twin and use case expansion.

Last but not least is the addition of the Multi-Model and Multi-Platform Mobility module, which contains services for adjacent segments like motorcycles, e-bikes, scooters (and even elevators!)

Finances

The graph below doesn't look very promising as growth has been negative the last couple of years, except for H2/23.

Several factors play a role:

The change in business model from fixed license payments to royalties and recurring SaaS revenue reduces initial contact payments.

Despite growing penetration (now powering 52% of worldwide auto production), the overall software spend per vehicle has faced pricing pressures and slower adoption of some advanced features, affecting total revenue.

The auto industry has experienced production constraints, supply chain issues, and economic uncertainties, which have impacted automotive electronics/tech orders globally, and by extension, Cerence.

But we should certainly not despair as these factors hide underlying strength. For example, the variable license revenue was $34.2M, up 48% y/y, reflecting strong utilization and more in-period revenue recognition.

The number of connected cars shipped grew by 12% y/y.

The company shipped 12.4M units in total, capturing 52% of worldwide auto production.

Revenue was $62.2M, beating the high end of the guidance range ($52M-$56M). However, this still represented an 11.77% year-over-year decline, primarily due to a strategic shift away from fixed license deals.

Some of the Q3 revenue upside was due to OEMs producing ahead of potential tariffs. The impact of tariffs is expected to remain limited in Q4, but the situation is fluid, needless to say.

Gross margin is trending upwards, while operating margin fluctuates with the fixed license payments.

Adjusted EBITDA was $9M, significantly above the guided range of $1M to $4M.

Below is the figure we like and think investors should appreciate more:

The company generated $16.1M in free cash flow, marking its fifth consecutive quarter of positive free cash flow.

The cash bonanza has enabled the company to reduce its total debt by $87.5M so far in FY25 using cash on hand. This includes repaying the remaining $60.1M of its 2025 convertible notes in June.

The company ended the quarter with $79.1M in cash and marketable securities, and management is comfortable operating at these levels.

The company has $198.8M in long-term debt.

Guidance

Management provided a cautious outlook for Q4 but raised its full-year guidance, reflecting the strong Q3 performance.

Q4/25 Guidance

Revenue: $53M to $58M. The sequential decline is attributed to a pull-forward of production by OEMs into Q3 ahead of potential tariffs, as well as normal seasonality.

Adjusted EBITDA: $2M to $6M.

FY25 Raised Guidance

Revenue: Raised and narrowed to $244M to $249M (from $236M-$247M). The new low end is above the previous midpoint.

Adjusted EBITDA: Raised to $42M to $46M.

Free Cash Flow: Raised to $38M to $42M.

Risk

Management touts its aggressive IP protection policies, as they have patent infringement lawsuits against Samsung, Microsoft, Nuance, and now Apple.

We are not patent lawyers, so this is difficult to handicap for us, but what is a little worrying is that three of these four companies have vastly larger resources compared to Cerence, so they can prolong these cases, raising the costs for Cerence.

The macro climate poses another risk. US growth at the moment seems supported by investment in AI-related stuff, mostly data centers, and not much else, and job creation has slowed to a crawl already. The rapid descent is worrying.

Valuation

SBC and dilution have been moderate. There were 669K RSUs. We couldn't find any info on outstanding options in the 10Q or the 10K, so we take 44M shares, at $10 per share (which is when we published the article for our Seeking Alpha investor group a couple of weeks ago) produces a $440M market cap and an EV of $559.7M. The shares trade at a fairly modest 2.27x FY25 EV/S and 12.7x EV/EBITDA.

Now it’s a little more expensive, at $12 per share, the market cap becomes $52,8 and the EV at $647.7, yielding an EV/S of 2.6x and an EV/EBITDA of 14.7x. Since we were touting the company's cash flow, here is another one to consider:

Basically, the shares sell at just over 10x free cash flow, and that's on a TTM basis. Given the steep rise in free cash flow on a forward basis, this valuation metric is likely to be lower still (although based on the FY25 guidance, not by much).

And there is an added cracker, which is that this amount of cash generation enables rapid debt reduction, as we have already seen this year, as they have taken out the 2025 notes and then some.

It also provides means to invest in growth (and IP lawsuits), whether through internal development and/or M&A.

Conclusion

Yes, the recent growth trajectory looks disappointing, but we think this is mainly the result of the changing business model. There are other metrics, like market penetration and especially cash flow, that look a whole lot better.

PPUs also began to rise in H2/24, and with the company moving to adjacent and even unrelated segments, even without having to add much in the form of OpEx, we think there is plenty of growth ahead for the company.

That growth might not be spectacular, but at some point, all the fixed payment license fees will lapse, and a clearer picture will emerge.

We think the shares aren't expensive and offer a pretty decent risk/reward here.