A Primer on DroneShield

Effective anti-drone technology is more necessary than ever

DroneShield (DRSHF) is an Australian-American producer of anti-drone technology rapidly catching on as it basks in the secular tailwind from the Ukraine war and conflicts in the Middle East. The shares have come down after a steep runup on a new financing but the company is already profitable.

The Market

A worldwide $10B TAM.

As drones are becoming cheap and prolific and can be used by anybody (state and non-state actors), they are becoming problematic in securing almost any facilities, military or non-military (like critical infrastructure), drones are the new AK-47, the ultimate weapon for asymmetric warfare.

Drones can be used in key areas such as non-warzone-based critical infrastructure, battlefields, drug and weapon smuggling, human trafficking, lone wolf terrorist attacks, and even paparazzi/stalking.

DroneShield has separate web pages for a host of use cases.

While Israel’s defense against the recent Iranian attack with swarms of drones (and missiles) was very successful, it has an estimated cost of $1.5B. Clearly, it’s not sustainable to knock out $20K-$50K a-piece drones with $1M+ a-piece missiles.

DroneShield Technology

DroneShield's products like the DroneGun and DroneCannon emit RF (radio frequency) signals that disrupt the control and navigation links between a drone and its operator, jamming signals overpower the drone's communication frequencies, seizing control from the remote pilot.

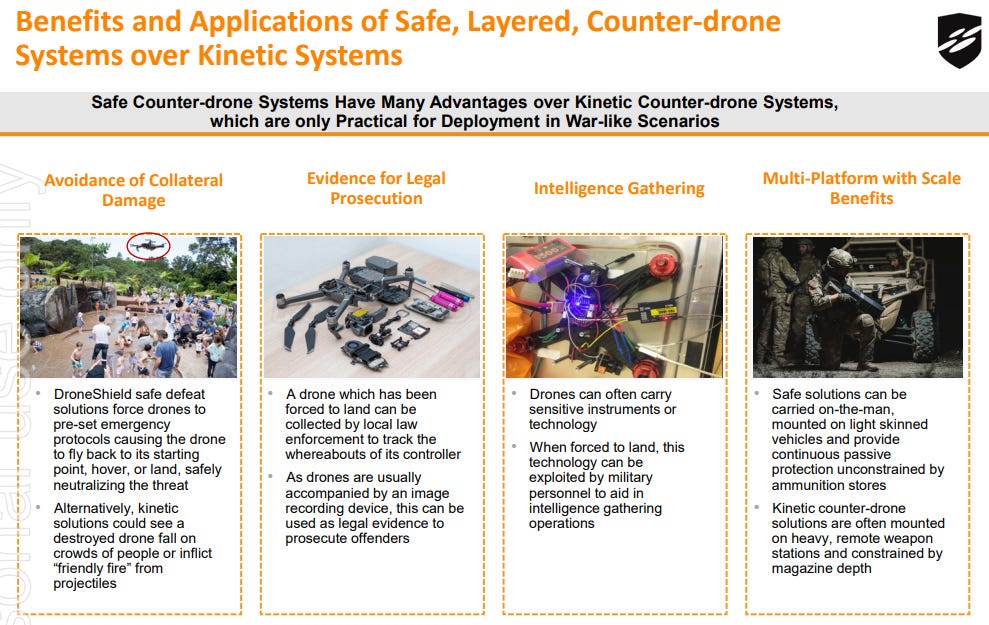

The technology does not use hacking techniques, but rather non-kinetic jamming to control drones, forcing the drone into a vertically controlled landing or returning it to its launch point, allowing for safe retrieval and analysis of the threat.

Advantages

Non-kinetic jamming provides an unlimited number of "rounds" since it doesn't rely on expendable munitions, making it more economical than kinetic defenses.

It mitigates collateral damage risks by avoiding explosions or uncontrolled crashes that kinetic weapons may cause.

The DroneGun is highly portable at just 16 lbs and can jam drones from over 2 km away for easy deployment.

The DroneCannon Mk2 provides a wide-area non-kinetic effector capability integrated into systems like Lockheed Martin's Agile Shield architecture.

Does it work?

There are case studies.

Here is a US Navy evaluation: “DroneShield deployed a DroneSentry-X on the U.S. Navy’s M80 Stiletto vessel for an exercise and extended demonstration. The system was deployed on the Stiletto maritime demonstration boat for a period of six weeks, successfully completing a wide range of performance and evaluation metrics. The system demonstrated overall detection capability, detection and defeat ranges, on-the-move operation in various sea states, and effectiveness against drone swarms, involving a wide range of robotic and unmanned threats.

And there are order wins and rapidly rising revenue, testifying to market acceptance.

NATO stock numbers were assigned to its products as a sign that it meets all NATO requirements. More recently it signed a NATO Framework Agreement, not only a strong endorsement of its technology but also a likely significant boost to revenues.

Products

DroneGun Mk3: operating on a standard swappable NATO battery providing a run time of 2 hours and weighing 4.72 lbs.

DroneGun Mk4: A heavier version of the Mk3 with a longer range.

DroneGun Tactical: Heavier, rifle-like 16 lbs portable DroneGun with a range of approximately 2 km and a runtime greater than two hours.

DroneCannon Mk2: a fixed, non-mobile device weighing 48.5 lbs that can be set to always be on or can be hooked up to DroneShield's command center for targeted use.

RfPatrol: a passive, portable UAS (Unmanned Aerial System) detection device that can be integrated into larger soldier battle management systems, allowing for data to be relayed directly to comment from the field. RfPatrol can be operated in two modes, Stealth and Glimpse, allowing the user to control how they receive alerts.

DroneSentry-X is a cross-vehicle compatible, automated 360-degree detect and defeat device. It provides awareness and protection using integrated sensors to detect and disrupt UAS moving at any speed—suitable for mobile operations, on-site surveillance, and on-the-move missions. There are several versions of the Sentry.

There are a host of additional slides with technical details here.

Business model

Three revenue streams

1) Hardware (units and accessories)

2) SaaS; device software updates on RFAI (radiofrequency spectrum engine) DroneOptiD (optical AI engine) and SFAI (sensorfusion AI engine). The long-term goal is SaaS revenue making up 50% of revenues.

3) R&D contracts.

New products, and recent additions are the Area-Specific Satellite Denial Systems, the DroneSentry-X Mk2TM, the SensorFusionAI, a Long-Range Radar, DroneSentry-C2 Tactical.

Recent orders

$2.2M Repeat order from a European Government customer (Nov/23)

$10.4M DroneShield equipment as part of an Australian aid package to Ukraine (Oct/23)

Finances

Growth is accelerating and the company turned profitable in FY23.

Q1/24 results were quite promising despite Q1 being the slowest quarter. Cash receipts ($7.1M) were low as most of the cash comes from the US government which pays 30 days after deliveries so most of the cash will arrive in Q2. Operational cash outflow was $10.67M as a result but this isn’t representative, the company is cash flow positive on a 12M TTM basis.

SaaS revenue doubled to $561K, still small but rapidly growing.

The company has production capacity which can generate $400M in revenue a year suggesting no immediate need for CapEx and the likelihood of improving gross margins with capacity utilization.

Cash $56.4M (and $100M+ to come after a financing, see below), no debt.

Outlook

The 5-year outlook is for $300-$500M/y in revenue with half of that coming from SaaS, with the revenue supported by 130-150 people in staff, which suggests strong operating leverage as the company had 120 staff at the end of Q1/24.

Rapid revenue growth, a shift to higher-margin SaaS revenue, and substantial operating leverage are a great mix for improving financials.

Financing

There are already a lot of outstanding shares and considerably more to come.

April/24 two tranches, tranche 1; $70.2M at $0.80 and another $30.3M at $0.80 (tranche 2) and a maximum of $15M oversubscription.

This adds another 125M shares and there is some more to come from share-based compensation.

$80M of the financing will go into building inventory given the strong pipeline, $10M will be used for expanding its AI capabilities.

Valuation

Analysts expect sales of US$63M in 2024.

With 750M+ shares out, the company has a market cap of US$457.5M at $0.61 per share (AU$607.5M at AU$0.81 per share) and an EV of US$302.5M.

The company is valued at 4.8x FY24 EV/S on a sales basis.

Valuation is still very expensive on an earnings basis FY23 p/e of 59x) but given the revenue growth (224% in FY23), gross margin expansion, and operating leverage these metrics will come down.

Risk

Rapidly evolving drone capabilities: “Commercial technology advancements will continue to increase the threat level by incorporating swarming, thermal imaging, LiDAR, GPS-denied navigation, and more.”

Rising competition (see below)

Dilution, which should be done for quite a while given the latest financing and the fact that the company is profitable and cash-generating already.

Competition

Different technologies are discussed here. Below a number of competing solutions:

This list is by no means exhaustive even if there is a wide disparity in the systems complexity, cost and range so not all of them are perfect substitutes for DroneShield products. Many are already in use in the US military.

Laser based systems is an alternative technology for which there is a lot of interest, but its range is shorter.

On the other hand, it’s always possible that a more effective and/or economic solution will arrive (like laser-based systems, like the ones under development at Lockheed Martin and Raytheon).

Conclusion

The proliferation of drone capabilities, threats, and use cases (besides war) creates a powerful secular tailwind for companies like DroneShield.

DroneShield provides effective and economic solutions, the latter is especially important given the high cost of many other systems.

It introduces new products regularly, with SaaS revenue coming from software updates.

The company managed to triple revenues last year and is already profitable and cash-generating.

The company has a rapidly expanding pipeline.

While the shares are expensive at the moment, revenue growth, gross margin expansion, and expected strong operating leverage these metrics will come down.

The main risk is a more efficient technology arriving that will provide more protection for the same money.