A Quick Take on electroCore

The company seems back on track while the shares are slumping, what gives?

The shares went from $6 to $19 despite revenue growth from its biggest sales channel, the VA, slowing, and the reason only became known during the Q4/24CC, the company had stopped hiring salespeople.

The curious thing is now that the company is hiring again despite a VERY challenging quarter in the VA (the DOGE chainsaw), and VA sales are growing again, the shares have slumped well below the $6 where they started.

Given the huge growth opportunities and an enormous TAM that the company has hardly scratched the surface of (all discussed below), this seems way overdone to us.

electroCore (ECOR) has been on quite a rollercoaster:

But underneath, things are distinctly less volatile. There are positives:

The company signed a new five-year VA contract.

Return to sequential growth at the VA, its biggest channel.

After a lull, the company is hiring salespeople again.

The company hardly scratched the surface of its enormous TAM, with multiple growth vectors available.

The company produces stellar gross margins in the mid 80s.

After a series of extensions, the company finally signed a new five-year deal with the VA. Considering the turmoil the latter has been in, with numerous contracts (as well as employees) being terminated without apparent cause, this should be taken as a positive.

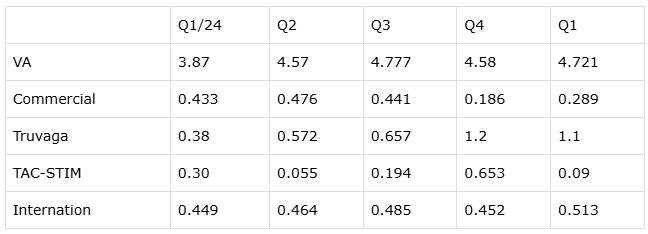

After the Q4/24 results, our biggest worry was the sequential stagnation (actually a small decline) in the revenue from the VA in Q4/24. In fact, revenue growth from the VA had been slowing down considerably from Q2/24 onwards:

The reason for the VA slowdown since Q2 isn't a mystery, the company stopped hiring salespeople by the end of Q2/24.

The only thing is, they didn't tell us that until the Q4/24CC (our emphasis):

Our 1099 team grew rapidly from 34 groups in January 2024 to 48 groups in July 2024, but the total number of active groups has remained constant since then. Revenue growth rate has slowed somewhat since the number of 10.99 groups leveled off. We expect the size of our team to grow in the second half of 2025 as we balance investments in future growth with the path to profitability.

So investors who previously bid the shares from $6 to $19 despite the slowing growth at the VA and not knowing the reason why that happened now dump the stock to below $5, while growth and hiring are back?!

Figure this, despite Q1 being the quarter with the maximum upheaval at the VA, showed a return to sequential growth.

What is more, this looks like accelerating as they are adding headcount again (Q1CC, our emphasis):

We started adding field sales headcount in the second quarter of 2025, March and April '25 monthly revenues in our VA channel have accelerated to about $1.7M.

So the adding started in April, if they keep up that $1.7M/M pace, Q2 will deliver $5.1M.

The company is also adding headcount to specifically target Kaiser, which is still small in terms of revenue it generates compared to the VA, but there is significant potential here as well for H2.

Recapitulating

We are somewhat baffled by investors bidding up the shares from $6 to $19 while VA sales were slowing down and the reasons for that weren't known, while now selling the shares to $4.5 while:

We now know why VA sales growth slowed, the company stopped hiring

VA sales are growing again in Q1, despite a seriously challenging environment in the VA in Q1 due to the DOGE chainsaw.

No surprise, as they started hiring again.

What's more, all that time, Truvaga sales keep growing at triple-digit levels, albeit from a low base.

There are other positives, but also some negatives, so we'll discuss these below.

TAM

It might be worthwhile to point out the TAM for the gammaCore:

There are some 600K VA patients treated for headaches (24K of these for cluster headaches), only 1.6% of these (9.5K) have received a gammaCore since 2022.

The company now sells in 175 VA facilities out of 6K, barely scratching the surface.

There are additional conditions for which the gammaCore could qualify, most notably PTSD, for which the company already had a meeting with the FDA. TBI (traumatic brain injury) is another condition for which the gammaCore has recently shown effectiveness.

There are potentially additional conditions beyond those two.

Then there are other payer channels like Kaiser which they already start to penetrate.

Then there is the acquired NeuroMetrix (which just closed) with its FDA-approved Quell platform (protected by 27 US patents) for treating fibromyalgia with some 550K patients in the VA. The Quell is selling to just 2 VA systems (which is why the acquisition is highly complementary). Once the manufacturing issues are resolved (this quarter), H2 looks promising, with management estimating gross margins at 60%+ once production restarts.

The Quell 2.0 system is sold over-the-counter (non-prescription) for lower extremity pain.

electroCore is transforming into a medical device company, leveraging its sales force and channels. Apart from acquiring NeuroMetrix, it closed a deal with an OEM, Spark Biomedial to sell its Sparrow Ascent, FDA cleared non-invasive transcutaneous auricular neuromodulation device, into the VA.

There are international opportunities, for now limited to the NHS in the UK (generating $513K in revenue in Q1, up $64K from Q1/24).

Another positive is the company's DTC product TruvagaPlus, which is off to a very promising start, growing revenues 187% to $1.1M. It also launched on Amazon in February, selling 200+ devices since then. Return rates are steady at 10-11%.

Truvaga will be launched in the UK and Canada this year and is exploring channels like influencers, affiliates, and resellers, and (Q1CC):

As of March 31, 2025, we have enrolled 144 Truvaga Plus partners including 49 gConcierge accounts who offer both product lines. We look forward to adding Quell fibromyalgia to these accounts as well.

Negatives

TAC-STIM, the $10K device selling into the military, is highly lumpy and had a soft quarter (just $90K in revenue), but management argues it has RFPs for several million dollars, so this could still take off.

Still losing cash, $4.4M in Q1 but that's going to slow to $3.8-$4.3M for the rest of FY25 (they had $8M left at the end of Q1) with management believing that they'll reach cash breakeven (at $9M revenue per quarter) late FY25 or early FY26.

$30M FY25 guidance is less than the analysts' average of $33.4.

Management apparently said something unfortunate with respect to the size of the sales force (they were going to triple it), but since we've not seen the literal quote nor the context, we can't independently confirm. It might have conveyed intention or plans, rather than reality on the ground, for instance. In any case, after completing a restructuring of the sales force, they've recently started hiring again, with most of the salespeople working on a pure commission basis.

Operating costs are rising considerably; they reached $9.5M in Q1/25 (not in the graph), although Q1 is seasonally high and there were separation costs as well. R&D expenses will remain constant for the rest of the year.

Finances

Revenue +23% to $6.7M.

Gross profit +$1.1M to $5.7M.

Gross margin: +100bp to 85%. Gross margins are expected to remain in the mid-80s.

Total operating expenses up $1.1M to $9.5M.

R&D expense up $243K to $642K, primarily due to increased headcount. R&D expense is expected to continue at this level for the next few quarters, with Most R&D focusing on sales support this year.

SG&A expense up $900K to $8.9M. SG&A expenses are expected to be in line with 2024 expenses for the remainder of 2025.

GAAP net loss up $400K to $3.9M ($0.47 EPS loss)

Adjusted EBITDA negative $3.1M, improving $100K.

Cash Position $8M

Valuation

There are 7.4M shares outstanding and 2.5M options and warrants for a fully diluted count of 9.9M, at $5 per share, producing a $45M market cap and a $37M EV for a FY23 EV/S of 1.23x.

For a company with double-digit growth, 85% gross margins, and a decent path to cash flow profits, that seems pretty modest to us.

Conclusion

The company experienced some headwinds with their own sales force restructuring and the VA, where DOGE cuts created significant upheaval, but the good news is that despite these, revenue growth at the VA has resumed on a sequential basis with an apparent acceleration in March and April.

So in essence, the company seems back on track, perhaps a little slower than we would have liked, but they still have myriad growth avenues ahead, and the new five-year VA contract is reassuring, as that could easily have gone very wrong.

There is also still a path to cash flow profits with some cash to spare, if management projections pan out and there is the off-chance of a large TAC-STIM order from the military.

While we understand management might have said some unfortunate things with respect to the size of its sales force, the company seems back on track after a disappointing Q4.

And while Q1 was hardly stellar, considering what was happening in the VA at that time, we count our blessings as the company escaped relatively unscathed.

The upshot: buy under $5