A Primer on Gatekeeper Systems

A shift from hardware to PaaS high-margin recurring revenues is just getting started..

In Short

The company is in the very first inning of shifting from hardware to a PaaS (Platform as a Service) model which will increase revenues from $1.2K-$2K per bus per year to $5K-$8.5K per bus per year and significantly increase gross margins.

The result is a more scalable business model creating significant operating leverage which deserves higher valuation multiples for the shares.

It is starting with its existing customer base, where it has installed 50K+ MDCs (Mobile Data Collectors), only a fraction of these are online (a necessary step for selling PaaS services) and it’s also winning new customers.

It can do the same with transit buses, and trains, the latter create even more revenue at 3-6x the ASP of buses or $30-$35K per train.

The company has significant tailwinds from regulation, Federal and state-level spending, and a technology upgrade cycle.

It has forged relations with multiple OEMs to get the MDCs installed at production.

Usually, companies that are in the first inning of some kind of SaaS model are making large losses and not selling at single-digit earnings multiple like GKPRF, producing quite a bit of cash flow as well.

PaaS

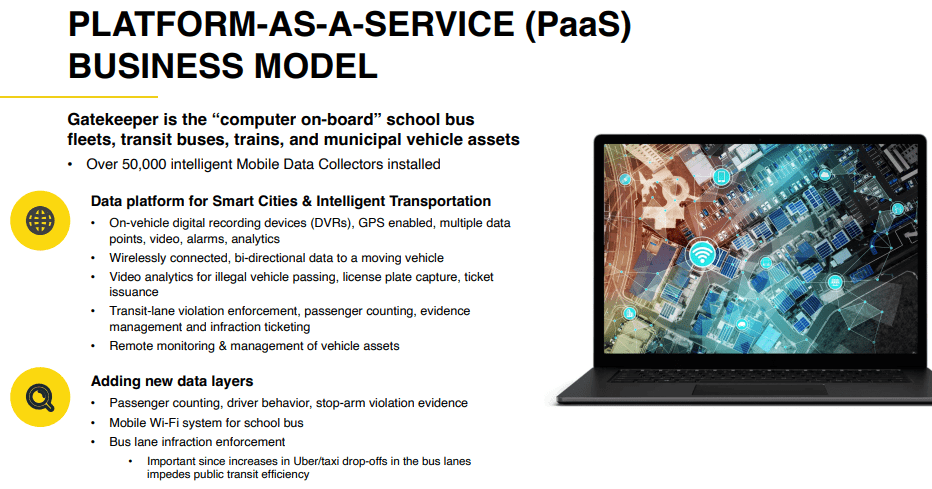

The company has installed 50K+ MDCs (Mobile Data Collectors), mostly in school buses.

From the Q2/24 MD&A: “These intelligent MDCs collect vehicle data such as video, audio, GPS, time, door open/close, and serve as the “black box” to aid in transit accident investigations. The MDCs are Wi-Fi enabled, mobile connected, or mobile enabled, allowing public transport assets to become part of the intelligent transportation solution in a Smart City ecosystem.”

Turning MDCs online and feeding the data to Gatekeepers hosted service (at $29/M per bus) opens up the opportunity to sell PaaS services, which potentially increases revenue per bus from $1.2K-$2K per year per bus to $5K-$8.5K per year (per CEO on the April/24 LD Micro presentation).

There is an installed base of 50K+ MDCs and only a fraction of these is online. The near-term goal is to get 10K of these online, which has the potential to significantly increase revenue, most of it recurring with a higher gross margin on a more scalable business model increasing operating leverage.

Usually, high-margin recurring software revenue generates much higher valuation multiples for the shares.

Hosted services

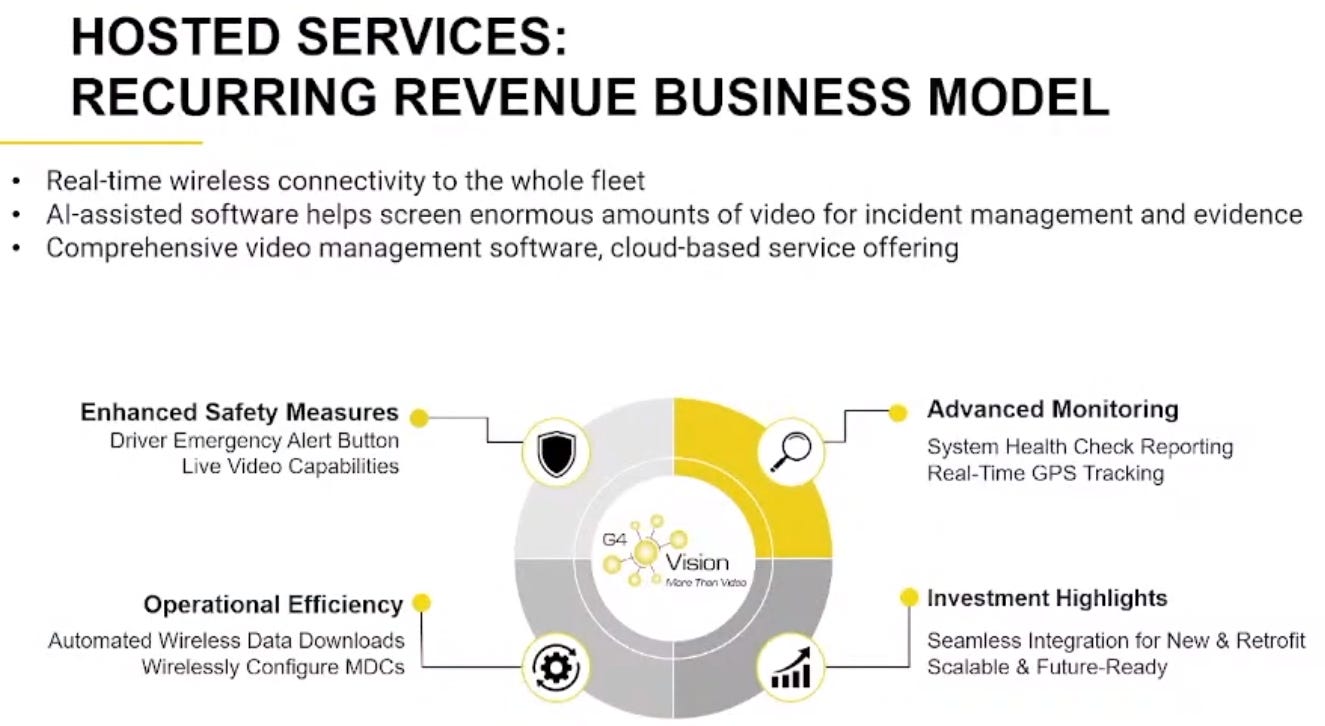

At $29/M per bus, it comes with AI-driven G4 Vision, which “enables real-time GPS tracking, video analytics, alerts on video camera tampering, behavioral analysis of passengers and drivers, driver emergency alerts as well as ticket processing of school bus stop-arm violations and transit lane violations. As a hosted service, G4 Vision can be scaled to provide real-time fleet management and alleviate the customer burden of manually analyzing increasing volumes of video data.”

One of these is Health Check, an AI-driven application that automatically monitors the health of a fleet's surveillance system. It works by checking the recording status of each DVR and uses Artificial Intelligence to check cameras for correct aim, lens impairments such as scratches, condensation or tampering in real-time.

G4 Vision Incident Management has saved SEPTA roughly $22M per year in false liability claims (which historically cost them $40M+ a year) with the help of its video evidence.

Additional Products

Video Analytics Software - records time, location, audio, and video, enabling quick and easy assembly of video evidence needed to deal with school bus problems such as bullying, grazing, vaping, or verbal abuse.

AI-based Safe Driving, warning for a host of dangers like lane departure, headway monitoring, forward collision warning, distracted driving, mobile phone usage, lens coverage.

Hardware like Interior Cameras, Exterior Cameras.

Student Protector - records license plate information day or night, of vehicles that illegally pass a school bus when the stop arm is deployed. Gatekeeper's optional proprietary software also automates the ticketing process of stop-arm infractions. There are an estimated 43.5M violations per year in the US with regulations allowing video evidence in 18 states already in place.

Pedestrian Protector – uses AI to assist the bus driver with blind spot detection and provides alerts of nearby pedestrians and school children near a school bus when stopped or operating at slow speeds. Advanced video analytics algorithms identify pedestrians while ignoring non-relevant objects like street signs, trees, and vehicles.

Mobile Wi-Fi - provides 4G or 5G internet connectivity for students and authorized users while the bus is transporting students or while the bus is parked in a neighborhood to provide internet access to students who do not have suitable connectivity at home.

360 Surround Vision Camera System - provides a surround view of the school bus and is automatically activated when the bus is reversing or making side turns. The surround view is displayed on a specialized rearview mirror system allowing drivers to monitor school children all around the bus.

Interior Camera - records the video and audio activity on the bus interior using adjustable vandal-resistant cameras.

Tactical Ready Kit - is a portable unit that allows law enforcement personnel to obtain a quick and easy display of the internal video and audio of a school bus in close proximity, even while in motion.

CLARITY an industry-first integrated video and school bus operating platform that will interface with Gatekeeper’s on-board mobile data collectors and video devices on school buses to integrate additional data elements such as GPS location, passenger counting, and video analysis for social distancing. CLARITY provides school districts with the scheduling and on-bus video and data analysis tools they need to manage the logistics of their school bus operations efficiently.

ALE; Automatic Lane Enforcement, ALE records the video evidence, captures the vehicle license plate, and prepares the instance for review and ticketing using the Company’s proprietary Traffic Infraction Management System (TIMS) software.

AI

The company offers a host of AI-based products like Student Protector, Pedestrian Protector, ALE, AI Dash Cam and G4 Vision.

Markets

School buses; there are 40K new buses per year, at $7.5K per bus, that's a $300M opportunity, apart from getting a bigger market share winning additional school districts, and getting its 3.5K+ existing districts customers onto its SaaS platform selling added services which only a fraction use at the moment.

Trains offer a huge opportunity at 3-6x the ASPs of buses, that's $30-$35K per train.

City buses offer an additional $150M opportunity.

Additional opportunities in first responders, taxis, and the like.

There are several tailwinds:

1) Federal and state level funding and regulation like the 2021 Federal $100B+ funding for transit and school industries,

2) Upgrade cycle like the move towards EV buses

School buses

In addition to the $100B+ in Federal money from the 2021 Infrastructure Bill, there is additional money like the $5B EPA Clean School Bus Program, which already led to EV buses being adopted in Texas, Oregon, and Washington. Then there are states like Florida and California working towards a broader adoption of EVs in public transit.

They have 10% of the market with 50K+ MDCs installed

Transit

The company rapidly got a foothold since entering in 2018 with notable wins like SEPTA (Southeastern Pennsylvania Transportation Authority) is the 6th largest transit authority in the US and is a Gatekeeper customer.

Gatekeeper is saving SEPTA $22M/y in false liability claims using its video evidence, which is paying for way more than the system costs SEPTA.

On October 12, 2023, the Federal Railroad Administration announced a final rule requiring the installation of inward- and outward-facing image recording devices on all passenger train lead locomotives providing scheduled intercity rail passenger or commuter service. This opens up a $300M opportunity.

They are compliant with the recommendation made by the National Transportation Safety Board (NTSB), which calls upon the Federal Transit Administration to install crash-resistant inward and outward-facing cameras and continuous recorders in all rail transit vehicle

The Company has engaged in discussions with four of the six largest international train manufacturers and has established relationships with several OEMs in the transit industry, enabling the integration of its PaaS platform as a factory install on new buses and trains like Thomas at High Point North Carolina, IC Bus in Tulsa, and Blue Bird in Port Valley (see here 14:10 min).

Other opportunities

OEMs; New Flyer of America

Smart City

Overseas markets

Recent wins

Finances

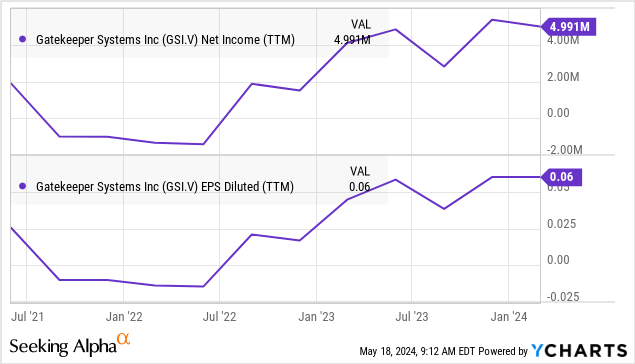

Growth is a little lumpy quarter-to-quarter, the company generates 50%+ gross margins and 18%+ operating margin (GAAP) with cash flow well into the black and rising:

$8.5M in cash, no debt, 100M shares fully diluted, CAD$70M market cap.

There will be some cost increases through investments in cybersecurity and salespeople.

Valuation

We see continued strong growth, margin expansion, operational leverage and cash generation although results can be lumpy quarter-to-quarter. The shares are cheap at 12x TTM earnings (and probably below 10x on a FY24 basis).

Conclusion

We see a modestly valued share that has multiple tailwinds and growth drivers, like:

Large Federal and state-level financial and regulatory support and the Transit technology upgrade cycle powered by developments in AI, machine vision, wireless technology, and EVs.

Shifting to a PaaS model increases the TAM, gross margins, and operating leverage should increase valuation multiples, as well as a huge opportunity increase in ARPU for existing customers as just a tiny fraction of the 50K+ installed MDCs are on the PaaS model yet.

Winning new customers, introducing new products and services, entering new segments and markets, and overseas expansion.

So far the growth is still a little lumpy but I expect that to decrease with the company getting more existing customers on its platform generating recurring revenues. This will produce margin expansion and operating leverage as well so earnings growth can be brisk.

TAM is huge, but what is realistic slightly conservative growth for next 3 years and related eps?