A Quick Take on LightPath

See our free Primer to get to grips with the moving parts.

Here are some updates and an investment perspective, as things are clicking into gear for LightPath.

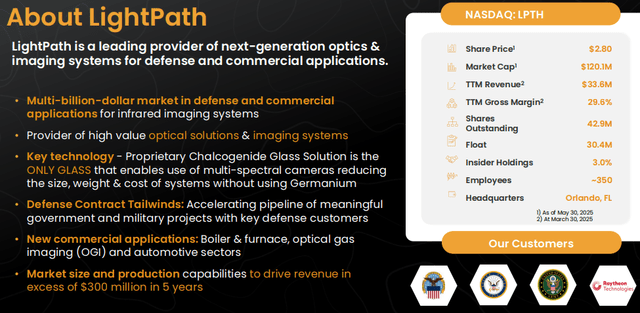

LightPath (LPTH) is a company with some interesting proprietary technology, its BlackDiamond technology, a family of infrared materials that serves as an alternative to germanium and gallium.

BlackDiamond is used for imaging and sensing solutions, offering significant technical advantages, producing substantial reductions in system size and weight, and often improving overall system performance (e.g., operating temperature range).

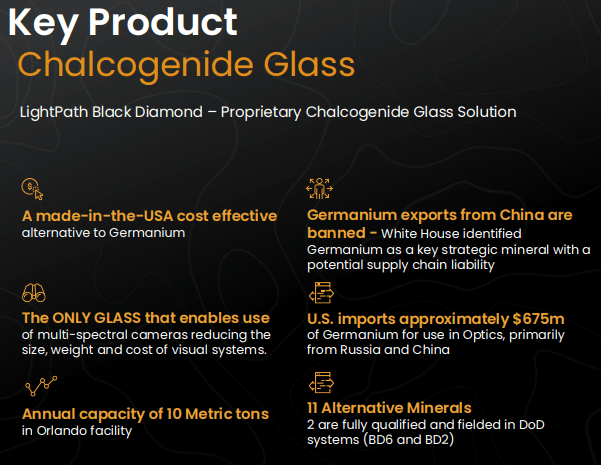

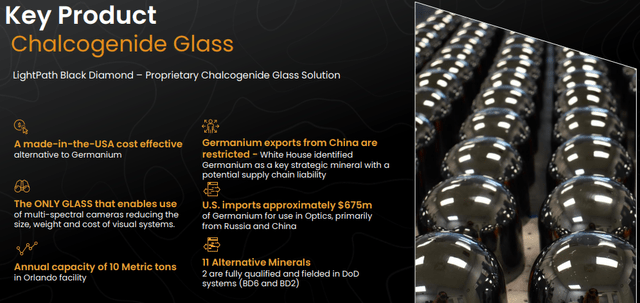

In addition to superior performance, competing germanium and gallium-based solutions are heavily dependent on China, especially given China's export limitations, which have been tightening lately due to trade tensions.

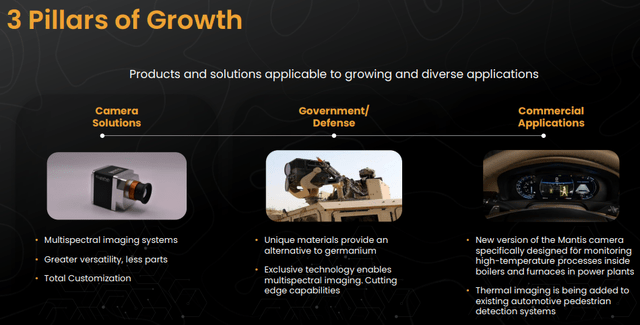

LightPath is increasingly vertically integrated, shifting from being a component supplier toward a solutions provider, moving up the value chain.

The company also has some unique technology, like camera technology coming from the acquisition of Visimid Technologies, its proprietary BlackDiamond glass, an alternative to Germanium with additional advantages in cost, supply chain security, and technical performance.

Products are organized into four groups:

Infrared components include molded and turned lenses and assemblies using various infrared glass materials, including the company's BlackDiamond glasses.

Visible components focus on aspheric lenses produced through glass molding technology.

Assemblies and modules include mounted lenses, optical assemblies, collimator assemblies, and other custom specialty optics.

Engineering services offer custom product development agreements, a critical pipeline for new product lines.

Competitive advantage

LightPath is the pioneer of PMO (Precision Molded Optics) and claims to still be preferred vendor for the most complex, high-end projects utilizing PMO.

LightPath is vertically integrated to produce infrared optics, from raw materials to assemblies and engineered solutions.

The company manufactures its own chalcogenide glass, including the proprietary BlackDiamond material is the only glass that enables true multi-spectral imaging, while also reducing the size, weight, and cost of infrared systems and as importantly, replacing Germanium which has a considerable supply chain risks given that most of it comes from Russia and China with the latter already having placed restrictions on exports.

LightPath is becoming a solutions provider offering design, assembly, and testing capabilities, allowing customers to avoid large investments in developing those capabilities in-house.

LightPath can provide custom high-performance optical components.

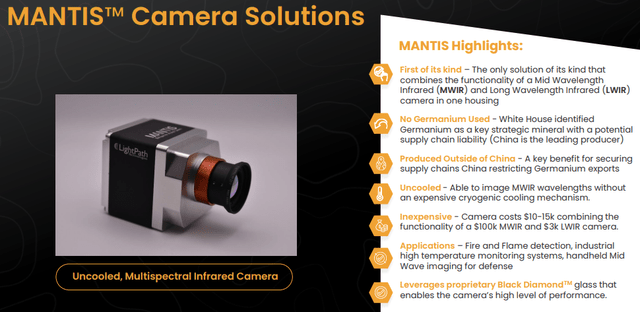

Proprietary cameras and optics

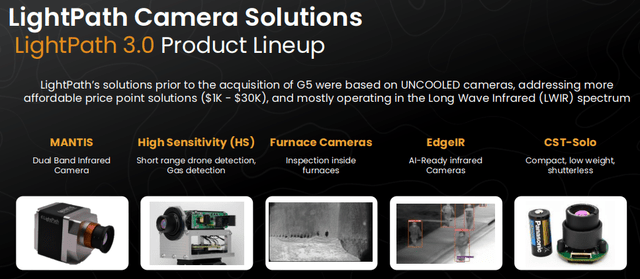

The company has built a portfolio of thermal cameras, like the MANTIS, a multispectral infrared camera selling at $30K a piece, a significant shift from the previous business model of selling lenses "for the price of a cup of coffee" (Q1CC).

The MANTIS capabilities are made possible by LightPath’s exclusive BlackDiamond materials licensed from the NRL (The US Naval Research Laboratories), a key differentiator, offering performance advantages over traditional materials like Germanium as well as reducing supply chain risks.

The MANTIS demonstrates LightPath's technical leadership in infrared imaging and their ability to develop technologies at a system or application level (LightPath 3.0).

The MANTIS has allowed LightPath to enter new markets and is used for:

Furnace inspection and high-temperature process monitoring (selling for approximately $30K each!).

Early detection of flames and fires.

OGI (Optical Gas Imaging) Cameras to detect fugitive gas emissions, such as methane, in the oil and gas industry.

ADAS (Advanced Driver Assistance Systems) with thermal imaging is expected to be adopted into all new cars by 2029 for emergency braking systems that can identify pedestrians in the dark, presenting a significant addressable market.

AI Accelerator Hardware Integration. BlackDiamond materials are integrated into cameras with AI accelerator hardware, enabling true edge implementation of AI models directly in the camera (named EdgeIR) for easy deployment by customers.

The company is developing new versions of the MANTIS, including a version for furnace inspection and a version for long-range detection.

The recent introduction of its OGI (Optical Gas Imaging) camera is another new system, used to detect fugitive gas emissions. New regulations that impose steep penalties on these emissions have made this a must-have capability for the oil and gas industry.

The company is leveraging its know-how to launch additional incremental products without significant development expenses. For instance, the company has recently introduced a new version of its OGI camera platform to detect fugitive ammonia and sulfur hexafluoride (SF6) emissions for industrial and manufacturing applications.

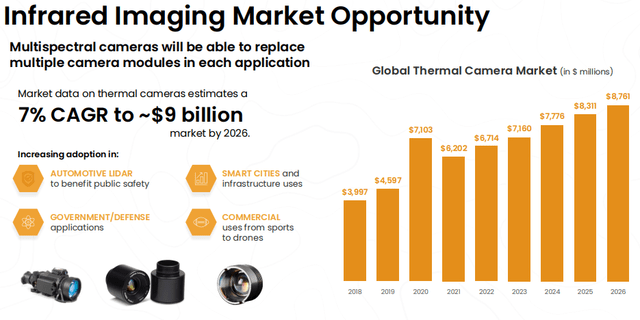

The Market

There is a considerable tailwind from the market, on top of BlackDiamond's competitive advantage and supply chain reliability issues for germanium and gallium-based solutions.

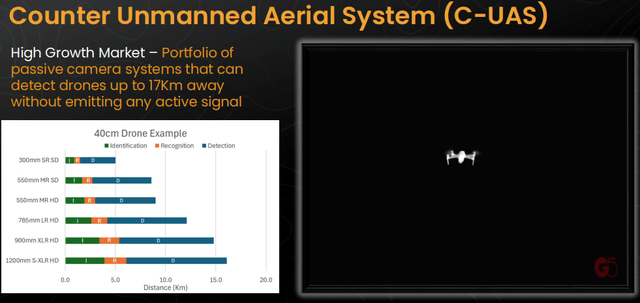

Additional use cases are emerging, like the high-growth opportunity in drone detection:

Growth

The company is also making a strategic transition from a mere supplier of components

G5 Infrared acquisition

The company announced the acquisition of G5 Infrared, and the deal closed in February. It added a product line of cooled infrared cameras for long-range imaging. The post-merger integration is proceeding well, with strong cultural fit and alignment on goals.

The acquisition is cementing the company's transition from a component supplier to a vertically integrated global solution provider for infrared imaging technologies, enabling it to service bigger projects. The primary advantages and reasons for the G5 acquisition include:

G5 Infrared adds a product line of cooled infrared cameras for long-range imaging to LightPath's portfolio, a significant expansion from LightPath's existing uncooled infrared cameras (like the Mantis) and optical gas imaging technology acquired through Visimid Technologies.

G5's products add significant new growth opportunities, particularly in the defense sector. Key programs and growth drivers brought by G5 include the SPEIR program with L3Harris, and additional large programs in border security and other counter-UAS initiatives (see below).

Management also fully expects for G5 to continue winning more large programs, each potentially bringing revenues in the range of $5M to $20M a year. Orders are already arriving,

The inclusion of G5's cooled cameras contributes to a more favorable product mix, with optical assemblies, cooled and uncooled cameras, and other subsystems now constituting roughly 50% of LightPath's revenue.

These products naturally have higher ASPs than the component business, which is expected to continue growing. This shift is a primary factor in the significant increase in gross margin (up to 29.1% in Q3/25 from 20.9% in the prior year quarter).

The acquisition is expected to provide an expedited path to achieving LightPath's long-term goal of 15% EBITDA margins. The combined companies are expected to generate $51M in revenue in the 12 months following the G5 acquisition (from February 18, 2025).

G5 had $13M in new bookings since its acquisition in February (see the orders above), with financial impact expected to be visible starting in Q4 FY25 and predominant in Q1 and Q2 of FY26. The first earnout for G5 requires achieving $21M in revenue and 20% EBITDA.

G5 does not make its optical components, but LightPath's optical component manufacturing can step in to support G5's needs and potentially address lead times for components.

LightPath has also placed very large orders for detectors for G5 to get ahead of demand, and there is capacity for increased assembly at G5 by adding shifts or people.

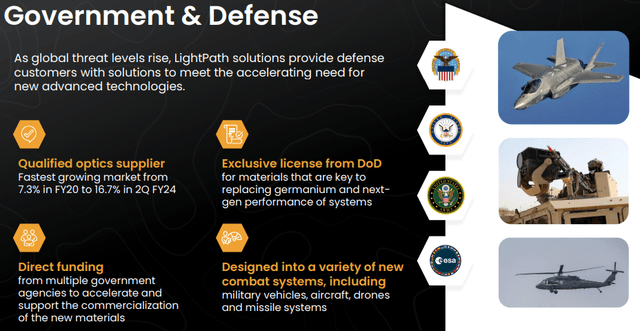

Defense Programs

Unlike Germanium, BlackDiamond materials are produced domestically and have a secure supply chain, which is a key advantage, especially for defense applications.

LightPath has partnered with the DoD and the DLA (Defense Logistics Agency) to replace Germanium in DoD applications. They have become a go-to partner for anyone looking to phase out Germanium.

After a successful phase 1 resulting in the qualification of several new proprietary BlackDiamond materials, the company has received Phase 2 funding from the DoD via the Defense Logistics Agency (DLA) to support the qualification of additional BlackDiamond glasses, from the Q3CC:

Since these materials are now key through several programs of record, we also receive monetary support from the DoD, Department of Defense to increase our capacity and processing capability. So for the most part the upcoming expansion which we're starting now in our manufacturing capacity is actually going to be financially supported by our customer, the government or end customer.

These materials are now being designed into multiple programs of record and demonstrate significant value beyond just replacing Germanium.

LightPath now has at least six large programs with individual revenue potential exceeding $10M per year, which could be transformative for the company.

The company also received an initial development contract from a new European defense customer to use BlackDiamond glass and a follow-on order from a European defense customer was received for infrared assemblies for use in FPV drone applications.

More than 30% of sales come from defense, most of which are in the US, and obtaining a European defense license opens the door for additional growth in Europe.

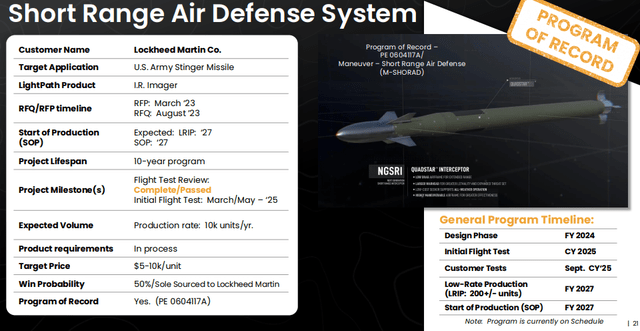

The NGSRI Program (Next Generation Short Range Interceptor - Stinger missile replacement) with Lockheed Martin. LightPath is developing a new camera system for Lockheed Martin that will be part of a missile system. This program is on an accelerated timeline, and the company has already achieved airworthy qualification of its subsystem.

Lockheed Martin is a competitive bid situation against Raytheon, and LightPath is limited in information disclosure due to its nature.

The program is run out of LightPath's VISIMID Group in Texas. A strong indication from the customer regarding the decision is anticipated by Fall 2025, although the formal decision is expected by October 2026.

If Lockheed Martin wins against Raytheon, LightPath could see revenues of between $50M to $100M a year, a potentially company-transforming opportunity for LightPath, which is on $30M a year in revenues.

The SPEIR Program (Shipboard Panoramic Electro Optic/Infrared System) with L3Harris. The G5 Group in New Hampshire is providing advanced infrared cameras for naval surface vessels to detect passive threats (e.g., unmanned vessels, drones, CUAS systems). This is a sole-source program of record that is expected to move into low-rate initial production (LRIP) soon, becoming a multi-million-dollar per year program.

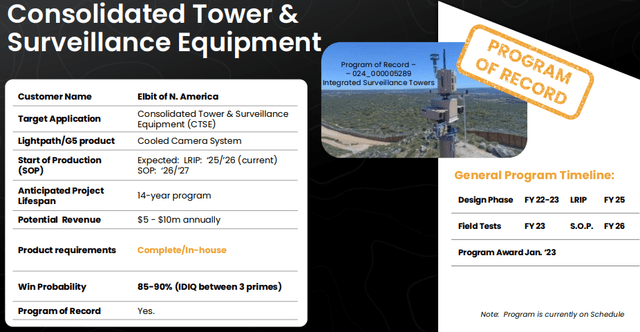

The Border Security Programs: G5 has additional large programs in border security. G5 is the sole provider for Elbit of America, one of three record suppliers for Border Patrol's towers. Elbit's system is considered the preferred system, and LightPath expects the majority of purchases to go through Elbit to G5. While an Indefinite Delivery/Indefinite Quantity (ID/IQ) contract, the first multi-million dollar order from Elbit was received in January, with real deliveries expected to start in the coming months.

BlackDiamond Optics Programs

The Apache Program, related to BlackDiamond glass, is progressing but has encountered some delays, from the Q3CC:

No. So the delays on our side, our team was not able to meet the timelines we've committed to or thought we would. It's sort of a combination of a couple of things. First of all, we took on a stretch project, so it's a very challenging product, otherwise we wouldn't get the premium getting for it. It's really a cutting edge in terms of the complexity of the product and it depends heavily on BDNL-8, one of our new materials. We were running out of capacity for a while as we were seeing sort of an unexpected influx of demand in a couple of other areas.

They are working on initial prototypes for Apache, which is also likely to offer international opportunities after US adoption but that will take at least five years.

The New BlackDiamond Program is a fairly new program based on NRL-licensed materials that is moving at a very fast pace. It involves the redesign of an existing system where LightPath's materials offer exponentially better performance.

The government is providing financial support for equipment to expedite its progress (Q3CC):

Meaning that the government is giving us pretty much any money we need or writing checks to give us equipment to move as faster than we are and for anything that we need this material. It's a redesign of a system, an existing system that with the redesign performs exponentially better than what it did before.

This program is expected to soon join the "club of multi-million dollar orders," potentially reaching $10M or more per year within 1 to 1.5 years from now.

So there is plenty going on, and the G5 acquisition has opened several more doors, and the expectation is that this number will expand.

The upshot (Q3CC):

So as you can see, those are what we would call our large programs, programs that each have a revenue potential that is north of $10 million a year and therefore each one of them can be somewhat transformative to a company our size. It used to be one or two of those and we would discuss them in great detail, but now having at least six of them in a mature stage, it becomes a bit less practical to discuss all of them in such great detail.

Commercial market

Besides the defence industry, there are multiple segments in the commercial market where its solutions have an edge.

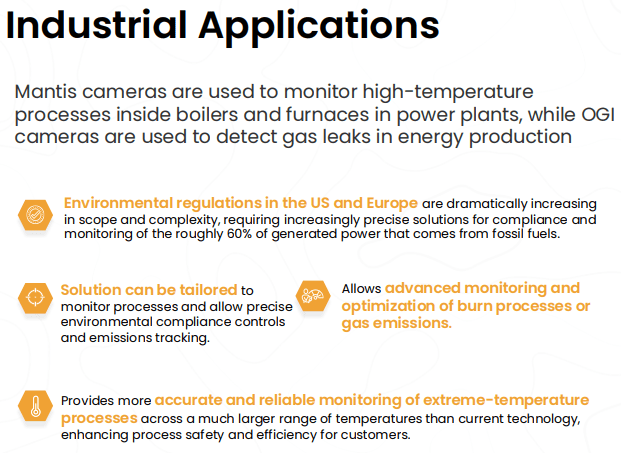

In Industrial Monitoring & Process Control, MANTIS cameras are applied for real-time, high-temperature process monitoring inside boilers and furnaces, providing safety, emissions tracking, and precise compliance for power plants.

Its cameras can also detect gas leaks and monitor environmental compliance in the energy sector, addressing increasing regulation and environmental scrutiny. For instance, its uncooled OGI cameras are deployed for 24/7 tracking of methane emissions at oil and gas facilities, supporting fugitive emission monitoring and sustainability goals.

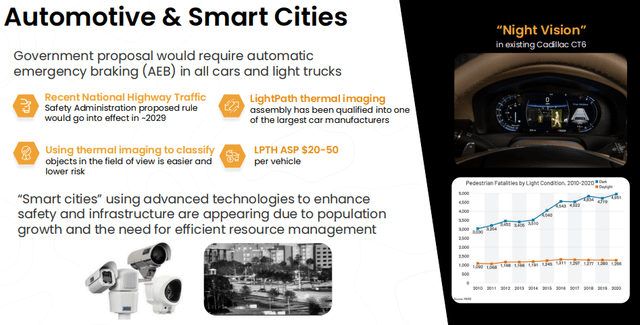

In Automotive, its thermal imaging assemblies have been qualified for mass production with automotive manufacturers, including advanced night vision technology already in use in vehicles such as the Cadillac CT6. Thermal imaging provides object detection and automated emergency braking, aligning with new federal safety proposals that may require such technology by 2029. Average selling price per vehicle is expected at $20–$50, with current shipping volumes exceeding 100K units.

In Smart Cities & Infrastructure, Thermal and multispectral camera systems are increasingly used for real-time monitoring, public safety, infrastructure inspection, and traffic management, as well as as pollution detection and urban resource management.

Finances

This is a little deceptive as the G5 revenues are added from February 19 onwards (until the end of Q3, the end of April, so it counted for most of the quarter).

Revenue was up 19.1% to $9.17M, beating estimates by $500K. Infrared components ($3.6M, 40% of revenue), Visible components ($2.8M, 31%), Assemblies and modules ($1.9M, 20%), Engineering services ($0.8M, 9%).

Gross margin was up 820bp to 29.1%, primarily due to a more favorable product mix with higher-margin assemblies, modules, and engineering services, showing the strategy is working, and more is coming (Q3CC):

One more quick for Al, then I'll jump back in the queue. The gross margin outlook. I'm just thinking about the growth in assemblies and modules sequentially. I imagine most of that is G5, and that was only, I think a month or whatever, six weeks maybe of G5. So next quarter you have a full quarter, you'll have a best, that product line, that segment will jump again sequentially, and that's a higher margin segment than some others. So that's just a natural gross margin expansion situation. Al, is that correct?

Operating costs have increased considerably, from the Q3CC:

Operating expenses increased 44% to $6 million for the third quarter of fiscal 2025 as compared to $4.2 million in the same quarter of the prior fiscal year. The increase was primarily due to higher legal consulting fees related to business development initiatives, including $0.7 million in expenses associated with the G5 acquisition, product development costs of $0.2 million, additional sales, general and admin costs from G5 of $0.4 million, a net increase of amortization expense of $0.3 million, as well as increased sales and marketing spend to promote new products.

LightPath is also investing in increasing manufacturing capacity for its BlackDiamond materials with financial help from the DoD, as well as in the development of its camera technologies, like the Mantis and the new Optical Gas Imaging Camera platform.

It's no wonder, then, that cash flow has taken a bit of a hit:

Some additional Q3 data:

EPS: -$0.09, missing by $0.04.

Net loss of $3.6M, compared to $2.6M in Q3/25.

EBITDA loss of $2M, compared to $1.5M in Q3/25. Management expects to be close to EBITDA breakeven or positive in the June quarter (Q4/25). Going forward, EBITDA will be emphasized due to complex accounting related to G5 financing and valuation.

Cash and equivalents of $6.5M.

Total debt of $5.5M.

Backlog (as of March 31, 2025) of $27.4 M.

Valuation

There are an additional 96K options, 396K RSAs, and 1.25M RSUs for a fully diluted share count of 44.6M, which at $2.9 per share delivers a market cap of $129.3M and an EV of $128.3M.

With analysts expecting FY26 (ending in June 2026) revenues to be $53.75M, which produces an EV/S of 2.39x. Even in FY26, analysts still expect a loss, though with a negative $0.12 EPS.

Discussion and conclusion

We were a little hesitant to fully recommend the shares in January for our members, as they seemed to have promising growth avenues, but revenues had been stagnant or even declining up until then, and the biggest growth opportunity, a Lockheed contract, wasn't a sure thing.

The situation with Lockheed hasn't changed significantly. This involves the NGSRI Program (Next Generation Short Range Interceptor - Stinger missile replacement) with Lockheed Martin.

This is LightPath's largest revenue opportunity and is progressing to plan. It is a competitive bid against Raytheon, so success is not guaranteed, and management is limited in information disclosure due to its nature.

The program, which is a camera program, is run out of LightPath's VISIMID Group in Texas. A strong indication from the customer regarding the decision is anticipated by Fall 2025, although the formal decision is expected by October 2026.

While NGSRI might constitute the biggest revenue opportunity, three things have happened that are turning around the fortunes of the company and management argues that the company has reached an inflection point:

Growth has returned

The company made an acquisition

The company gained multiple other big programs

So, in conclusion, we can identify that multiple things going for LightPath:

Its unique BlackDiamond technology has widespread use in the military and industry and brings important technical and economic advantages, with supplies of alternatives compromised.

The company is in the midst of what seems to be a promising transition from component supplier to a vertically integrated global solution provider for infrared imaging technologies, expanding revenue opportunities, increasing ASPs, and margins.

It made two acquisitions that seem to have a very good fit, with G5 adding many more doors for big projects. The company seems to have reached an inflection point with regard to these.

While in a previous assessment, we deemed that the future of the company was too dependent on Lockheed (its biggest revenue opportunity), we now think this would be the icing on the cake, and the company has a bright future even without a Lockheed win as it has a stake in at least 6 programs that could yield $10M+ revenues each.

Demand for its BlackDiamond materials, the crucial ingredient for most of its solutions, is rising so fast and it's so critical (most likely because of the Chinese export restrictions) that the government is financing its capacity expansion.

The shares aren't cheap, but we think there is considerably less risk than half a year ago.

The upshot: The shares are a buy at $3.

LPTH taking off on an $8M investment at $5 from a Drone company, Ondas https://seekingalpha.com/pr/20231861-lightpath-announces-8_0-million-strategic-investment-from-ondas-holdings-and-unusual-machines

Earlier this month they received an $18M order https://seekingalpha.com/pr/20219330-lightpath-technologies-secures-18_2-million-purchase-order-to-supply-advanced-infrared-camera