A Quick Take on Mobilicom

Appealing risk/reward

Mobilicom (MOB) is an Israeli company producing hardware and software solutions for drones and other ‘uncrewed’ devices like robots.

We introduced the company in our extensive primer, here we summarize and consider reasons for investing in the company.

Multiple reasons to buy

The drone and robotics markets are experiencing strong growth, creating potentially large tailwinds.

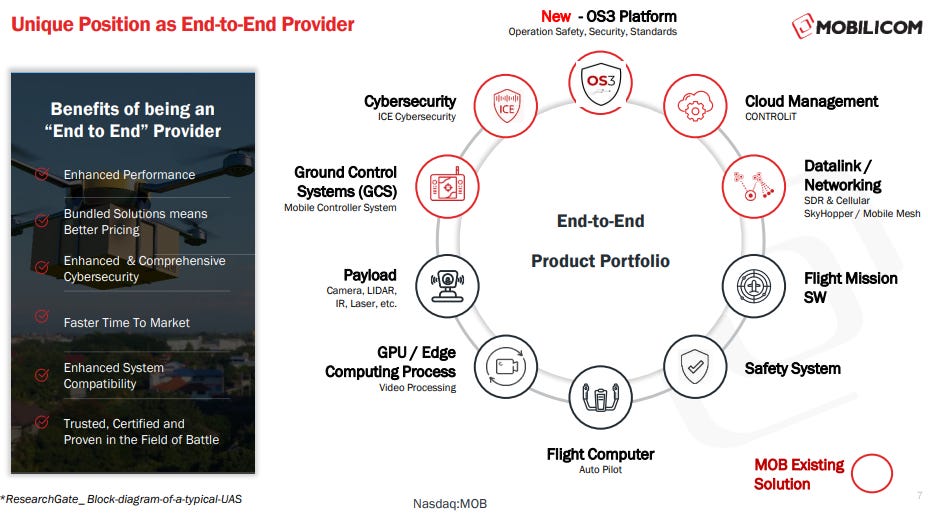

The company has comprehensive hardware (Sky Hopper datalinks, Mobile GCS (ground control systems), mobile mesh networking solutions, and software (OS3 Platform, ICE cybersecurity suite, Cloud Network Management) solutions, as well as system engineering services, providing a near end-to-end solution producing cross-selling opportunities:

Most of its solutions are thoroughly vetted through an extensive roster of 50 customers including 8 Tier 1 drone manufacturers, industry awards, and government approvals (through contracts with end customers). It also holds 2 patents and 34 patent claims.

Its OS3 SaaS platform has great potential as it’s a greenfield solution with no real competition and could easily be sold as an add-on to existing customers. These have an incentive to include it as they can share in the recurring revenue stream. It produces high-margin recurring revenues and elements of the platform, like the cybersecurity solution, already have customers for parts of it.

Margins are already very good at 50%-60% and could become better if SaaS becomes a bigger part of revenues.

H1/24 revenue growth was 230%, customers start small but scale up when they get orders or become part of government programs. There is a good chance for that to happen to several Mobilicom customers in 2025, keeping growth high, as is happening with a Tier 1 US producer:

The company outsources all hardware production, enabling it to scale rapidly as well as generate strong operating leverage, H1/24 revenue was up 3.3x from H1/23 while OpEx hardly changed. Management argues it will be cash flow positive at $10M-$12M of revenue but we think that might be sooner, given this strong operating leverage and the low cash bleed ($180K/M) already at low revenue ($3.6M run rate).

Finances

Revenues increased 232% year-over-year to $1.8M driven by initial production scale orders from U.S. and Israeli Tier-1 customers.

Gross margin 56%.

OpEx remained near steady, producing strong operating leverage (from the 6K):

The operating net cash burn rate for the six months ended June 30, 2024, was $1.1M averaging approximately $180K per month.

Cash $10M, further increased by recent $1.2M warrant conversion produces a 24M+ runway.

Valuation

There are 1.3M warrants left so we take an 7.6M share count which at $4 per share gives a $30.4M market cap and an $20M EV.

Conclusion

The company’s solutions seem more than sufficiently proven out by a strong roster of design wins and production orders from important customers.

Rapid growth is likely to continue as multiple customers will ramp up and growth could get another boost from new customer wins and OS3 wins.

Given the strong operating leverage and low cash burn, the company could well become cash flow positive at $10M-$12M in revenue, which only needs the sale of a few thousand systems, according to the CEO.

OS3 customer wins would be an obvious buy sign (as well as boosting gross margins). While that hasn’t happened yet (to our knowledge) parts of it have already sold.

With cash for years and a low cash burn, the risk/reward seems very favorable and it gives the company time to ramp up sales.

We are quite amazed at how the company is doing so much with so little ($2M/y in R&D) and produces such tremendous operating leverage.

today announced that one of its current customers, a Tier-1 Israel-based defense company that is one of the world’s largest loitering munitions providers, has selected the Company’s MCU-30 Lite and MCU-30 Ruggedized Mobile MESH products as key components for its new platform of perimeter protective drone fleets. This marks Mobilicom’s programs expansion with this Tier-1 customer by entering another platform, with prior design wins leading to production-scale orders as the customer’s new solutions have rolled out to market. The customer, which reports approximately $4 billion in annual revenue, is a prime vendor for Lockheed Martin in the U.S. and a major supplier of defense systems, including loitering munitions, sold to over 40 countries, including European Union and NATO member countries.

https://seekingalpha.com/pr/19982411-mobilicom-s-cybersecure-mcuminus-30-selected-by-one-of-the-world-s-largest-loitering

Any reason it's getting crushed today?