A Quick Take on Nayax

47% growth in recurring revenue and a 130% NRR

Four reasons to buy

The company benefits from the rapid growth in cashless payments and self-service retail markets.

The company produces terrific payment solutions and has multiple software platforms selling on a SaaS basis, offering a one-stop-shop solution for retail.

Recurring revenue is growing at 47% and the company produces a great 130% net retention rate, due to the quality of its offerings and the endless expansion and upgrade opportunities.

Gross margins are expanding and there is considerable operating leverage.

Against this one can argue that the shares are expensive on an earnings basis although earnings are set to rise fast with 35%+ revenue growth, gross margin expansion, and operating leverage kicking in.

A problem is also that the shares are rather illiquid and suffer from a large spread.

Introduction

Nayax (NYAX) is an Israeli company providing payment solutions for retailers, operating similarly to Par Technologies (PAR) for restaurants but with a broader scope.

While both Nayax and its competitor Cantaloupe (CTLP) benefit from the trend of self-service and cashless payments, Nayax distinguishes itself by catering to both self-service and traditional retail markets with its hardware and software solutions.

Primarily operating in the US and EU, Nayax has recently expanded into Latin America through acquisitions, a move mirroring Cantaloupe's recent entry into the region.

Products

Nayax provides a comprehensive suite of software and hardware solutions, offering a one-stop-shop for retail:

The company has multiple software platforms:

Payments Suite: International payments infrastructure that enables customers to offer consumers the ability to pay with their preferred local payment methods in their home markets.

Management Software Suite: A central intelligence hub for merchants that provides deep, real-time insights to optimize operations.

Loyalty and Marketing Suite: A consumer engagement loyalty and marketing platform that enables retailers to drive engagement with their target consumers.

From the 20F: Since 2005, we have invested significant resources to develop a large number of integration protocols that enable us to market our platform to many types of automated self-service points of sale with a simple “plug and play” installation approach. Our hardware and software are developed in-house, enabling us to manage manufacturing and production to our own specifications. Moreover, our software is easy to integrate with third-party systems via our comprehensive API suite, such as ERP systems and loyalty platforms.

Hardware Solutions:

Integrated POS: Proprietary devices designed for seamless deployment in-store or on existing machines, enabling digital payments. The company designs and manufactures its own hardware.

Nayax emphasizes "plug and play" installation for its hardware and software, thanks to its large number of integration protocols. The company develops its hardware and software in-house, managing manufacturing and production to its specifications. Its software easily integrates with third-party systems like ERP systems and loyalty platforms through its comprehensive API suite. Together these offerings solve many challenges for retail:

Market Trends

Nayax benefits from several key market trends:

Cashless Society: The increasing preference for cashless payments benefits Nayax's offerings like VPOS Touch and Onyx, easily installed on automated self-service machines across various sectors, including EV charging, vending machines, and parking lots.

Multi-Channel Purchasing: Consumers' growing demand for seamless personalized purchasing experiences across channels favors Nayax's comprehensive solutions.

Micro Market Growth: The increasing popularity of self-service stores in offices benefits Nayax.

EV Charging Expansion: Nayax is well-positioned to capitalize on the rapid growth expected in the EV charging segment.

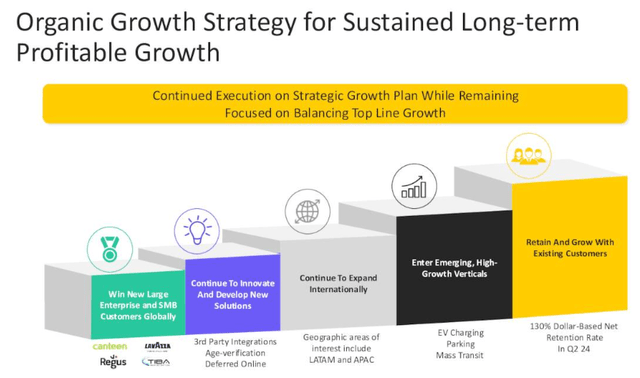

Growth strategy

Nayax's growth strategy combines organic expansion and strategic acquisitions (M&A).

Key growth pillars include:

New logo wins

Expansion into new verticals

Introduction of new products

International expansion

Strategic M&A

New customer wins

The company won 9K new logos in Q2 with 6K+ of these organic wins while 3K came through acquisitions (mostly from VMTech).

New products

An On-Cart payment solution for retail shoppers (together with Cust2Mate Solutions Corp.)

EV CloudPay, a payment solution for EV chargers

New verticals

EV charging stations through Nayax's EV Meter, a fully functional electric vehicle charging station equipped for commercial and residential sites.

Fuel Growth and EV Management: Nayax acquired Roseman Engineering, a company that provides hardware and software solutions (see below).

Latin American market, through its acquisition of VMtechnologia, a leader in Brazil's automated self-service industry (see below).

Parking, through a strategic partnership with TIBA Parking Systems, a company that provides hardware and software solutions for the parking market.

Hospitality: Nayax recently implemented its first hospitality solution in the Netherlands.

Notable Acquisitions and Partnerships

Nayax has made several strategic acquisitions and partnerships to fuel its growth:

Weezmo (July 2021): Specializes in linking online and physical purchases at points of sale using AI.

Tigapo (March 2021): Provides AI-driven software solutions for the amusement industry. Nayax holds a 53.55% stake.

OTI (January 2022): Provider of smart payment solutions.

Retail Pro (November 2023): This acquisition tripled Nayax's distribution network, adding 120 partner resellers and 150K point-of-sale lanes, creating cross-selling opportunities.

VMtech (April 2024): A leader in Brazil's automated self-service sector. This acquisition enables Nayax to expand into Brazil and Latin America.

Roseman Engineering (April 2024): Provides hardware and software solutions for EV charging stations, accelerating Nayax's presence in the segment.

Financials

Q2/24 results were excellent

39% revenue growth in Q2 2024, reaching $78M.

47% growth in recurring revenue, representing 68% of total revenue.

34% increase in transaction value, reaching $1.2B.

66% growth in gross profit, reaching $34.6M, driven by gross margin expansion.

Hardware margins increased to 28.7%, mostly due to improvements in its supply chain.

Recurring margins increased to 52%.

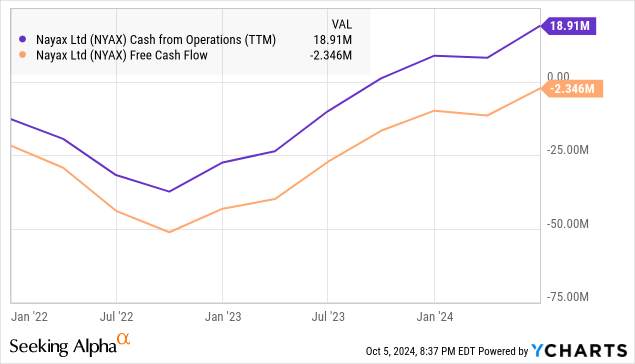

Operational cash flow of $9.2M, resulting in $86M cash on hand at the end of Q2 2024.

Adjusted EBITDA increased from $1.25M to $8.1M in Q2 2024.

The company sold 2.6M shares producing net proceeds of $62.7M in a March 12, 2024 financing.

Nayax's operational leverage primarily stems from gross margin expansion achieved through supply chain infrastructure improvements. Operational improvements, particularly in its Romania-based global service center, have significantly reduced call center wait times and improved support satisfaction rates.

FY24 Outlook

Revenue $325M-$335M (+38%+)

Hardware margins 27%-29%

Adjusted EBITDA $30M-$35M

Positive free cash flow

From the Q2CC:

This takes into account a slight contribution from the two acquisitions we’ve made this year, offset by our ongoing strategic shift to a hardware-as-a-service or rental business model

So basically the shift to the HaaS model actually produces a drag on revenue growth. The company also has a longer-term outlook:

Valuation

Fully diluted 39.1M shares, at $25.75 per share that’s a market cap of $1B and an EV of $969M, producing a FY24 EV/S of 2.93x and an EV/EBITDA of 30x.

Analysts expect a FY25 EPS of $0.41 so the shares are expensive on an earnings basis.

Nayax's current valuation is significantly higher than Cantaloupe's, but this is considered justified given its superior growth rate and more efficient operating leverage.

The company's potential to dominate the POS hardware and software market, similar to Par Technologies' role in the restaurant industry, makes it an attractive investment opportunity.