A Primer on Par Technology

A Business Overview

Introduction

This introductory overview will be followed by an article looking at the recent financials and prospects.

Par Technology (PAR) is a POS (Point-of-Sale) hardware and cloud software provider for restaurant chains. It has been patiently building up its SaaS software with new product developments and acquisitions and has now emerged as the cloud solution to beat. The company reports in two segments:

Operating Cloud (Brink, Data Central, Payments)

Engagement Cloud (Menu, Punchh, Stuzo)

It has two additional businesses:

POS hardware, with McDonalds as the biggest customer

A legacy government defense business that has just been sold (for $102M in cash).

Unified strategy

PAR envisions a "unified experience" for the restaurant industry. This means creating a single platform that seamlessly connects all aspects of a restaurant's operations, from back-of-house systems to customer-facing channels. This unified platform would empower restaurants to deliver innovative and personalized experiences to their customers while streamlining their own operations.

PAR Technology (PAR) has been executing a strategy for seven years, building a unified software solution for restaurant chains (fast casual or QSR, Quick Service Restaurant chains).

The company has many well-known customers like Five Guys Burgers, Arby’s, and Dairy Queen, followed by Cava (350 locations), Sweet Green (1K), Scooter’s (800), and MOD (500), and more recently Burger King (7K domestic locations).

After the acquisitions of Punchh, Menu, and recently Stuzo (and the upcoming acquisition of TASK) and building its own Payment services, the strategy is delivering success:

The whole is bigger than the sum of the parts, attracting bigger restaurant chains.

Creating a flywheel effect that produces relentless ARR growth.

The flywheel is now expanding into other segments, like table service restaurants, convenience stores, and geographical expansion.

Products; Brink

Brink is a cloud POS (point-of-sale) solution and PAR's most strategic product, producing opportunities to cross-sell additional PAR products once selected, from the Q1CC: We feel very bullish about our ability to drive cross-sell, especially as Brink works through its very large pipeline of deals this year.

And it's not only solutions like Data Central and Payments, also hardware is stapled onto almost all of Brink deals.

Demand for Brink itself is exploding, or at least it was in Q3/23 with double the amount of bookings (3.4K) compared to the previous highest quarter (Q4/22 with 1.6K bookings).

And this jump wasn't caused by Burger King. We couldn't locate Q1/24 bookings, so this may be a one-off, but the pace of logos wins has definitely increased so more data points indicate an acceleration in wins.

Payments

There are two services here, the front-end gateway Par Pay and the backend Payment Services.

Par Pay enables businesses of all sizes to accept electronic payments online or in-person, acting as the front-end technology by reading payment cards and sending customer information to the merchant acquiring bank for processing.

Par Payment Services is an all-in-one payment processing solution that aims to easily capture and leverage payments information with advanced insights into consumer behavior to simplify operations.

Data Central

Data Central is a back-office solution that leverages business intelligence and automation technologies to manage labor, food costs, and inventory, and perform enterprise reporting.

MENU

MENU is an acquired eCommerce platform for global restaurant brands, powering all digital customer touchpoints from mobile, web, kiosks to delivery marketplaces. It has the following functionality:

Omnichannel ordering: The platform supports various ordering channels, including mobile apps, web ordering, kiosks, and third-party marketplaces.

MENU Link: This feature integrates external ordering channels, including delivery marketplaces, into a single system for centralized order and menu management.

MENU Dispatch: An upgraded feature that simplifies last-mile delivery management, offering automated dispatching for both in-house and third-party delivery fleets.

Unified Management Center: A centralized hub for managing all aspects of digital ordering and operations.

Increased revenue potential: The platform aims to boost check sizes, improve margins, and tap into digital demand through various ordering channels.

Operational efficiency: By integrating multiple ordering channels and streamlining order management, MENU helps restaurants maximize operational efficiency and reduce errors

After considerable investments to adapt the product to the US market (and make a custom version for Burger King) the investments are now done and MENU will now start to scale, turning from generating losses to generating profits.

Punchh

Punchh is an acquired enterprise-grade customer loyalty and engagement solution that enables customers to deliver personalized promotions to their customers to increase customer lifetime value and same-store sales. It has the following functionality:

Loyalty and engagement platform: Punchh is designed to help restaurants, convenience stores, and retail brands acquire and retain customers through loyalty programs and engagement strategies.

Customer data unification: The platform allows businesses to consolidate customer data from various touchpoints, creating a unified view of customer interactions and preferences.

Personalized marketing: Punchh enables restaurants to create targeted marketing campaigns based on customer behavior and preferences, enhancing customer engagement and driving repeat visits.

Integration with Par's ecosystem: Punchh has been integrated with Par's other solutions, such as the Brink POS system, creating a more comprehensive offering for restaurants.

Industry recognition: Punchh has received recognition for its innovative approach to restaurant technology, particularly in the areas of loyalty and payments.

Enterprise-level focus: The platform is particularly well-suited for large restaurant chains and enterprise-level businesses, boasting a roster of blue-chip customers.

Strong performance metrics: Prior to the acquisition, Punchh demonstrated industry-leading growth, over 100% net dollar retention, and high customer satisfaction scores.

It will be merged with the recently acquired Stuzo over time.

Stuzo

Top loyalty product for convenience stores, opening up a new segment,

Acquired in March 2024 for approximately $190M paid in cash and stock.

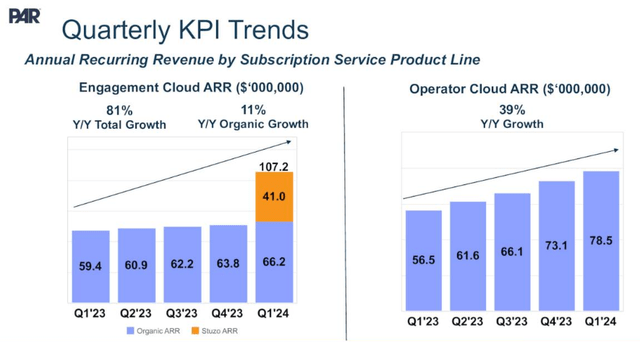

Stuzo is adding $41M in ARR.

Loyalty for convenience stores, opening a new segment, and lots of cross-selling opportunities, which are happening even faster than management thought at the time of acquisition. Will get back to $100M+ per year, but not necessarily this year.

PAR will merge the Stuzo loyalty software with Punchh but that will take significant time. In the meantime, it will still be sold and will simplify things as Punchh no longer has to compete in the convenience store segment.

TASK

Task is an Australia-based global food service transaction platform that offers international unified commerce solutions, including interactive customer engagement and seamless integration, tailored for major brands worldwide. This has made TASK’s transaction management platform the platform of choice for some of the world’s most successful and recognized food service brands including, Starbucks, and Guzman Y Gomez while its loyalty customer engagement platform is used by McDonald’s in 65 markets. With the addition of TASK, PAR will be able to serve the top enterprise food service brands across the globe with a unified commerce approach from front-of-house to back-of-house.

TASK has Starbucks Australia and McDonalds internationally as customers.

The acquisition will add $6-$8M in adjusted EBITDA/y and a large pipeline of deals and a significant customer base to cross-sell PAR solutions.

The acquisition ($206M all cash) is expected to close in Q3, financed in part from the sale of Par’s government business (for $102M) which has just closed.

The acquisition of TASK opens up international markets for PAR and could help getting the international business of Burger King, which actually has more stores than the 7K domestic ones PAR has already won.

Hardware

Hardware consists of POS terminals and drive-thru equipment.

Hardware has McDonalds and Yum Brands as customers, among others.

Hardware now has a nearly 100% attachment rate to Brink, which bodes well for the future given the pipeline for Brink.

$7.7M of $13.5M in professional services is recurring revenue from hardware support contracts.

Hardware margin was up 590bp to 22.3% in Q1/24 on improved inventory management and price increases.

Competition

Toast, which is more focused on smaller table service restaurants. Payments as the main revenue driver rather than software and just lost its only big chain, Jamba Juice, so it's less of a threat now. It remains to be seen how they will fare in table service chains, which is a segment that PAR is likely to make inroads into.

Oracle/NCR, which doesn't offer a specialized solution for restaurants and they have some problems. They pitched Burger King a lower price but lost to PAR nevertheless.

Qu is a small upstart but activating stores is very slow and wins due to aggressive pricing, not the sophistication of their products.

Olo is a competitor of Menu, but the latter seems to have played a big role in Burger King going for PAR. Olo lost Subway as customer, although that might not have much to do with the quality of the software.

Growth drivers

New logos

ARR growth

Scaling of Menu and Payments, which are in the first innings still.

Entering new segments like Table services, Convenience stores through new products and/or M&A

Cross-selling opportunities and price increases boosting ARPU

International expansion

Finances

Growth seems to have declined sharply but what really matters is ARR growth, as the government and hardware businesses can be lumpy. We’ll argue in a subsequent article that there are good reasons to see ARR growth accelerating to 20-30%.

The company still makes substantial losses:

So it’s no surprise that it’s bleeding cash, even if the trend is improving:

Valuation

Selling the government business ($102M) only pays for half of the TASK acquisition ($206M)

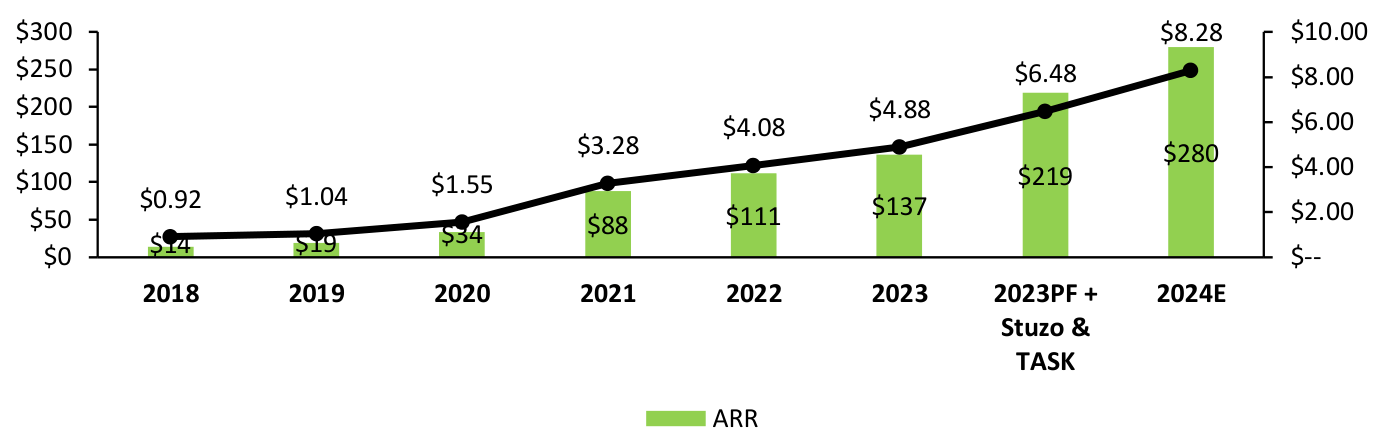

The company has a market cap of $1.46B (at $43 per share) and an EV of $1.78B, but it's better to value the company on its ARR (and ARR per share, see graph below), which is projected to increase significantly with known elements (Burger King rollout, acquisitions):

While the apparent growth slowdown, continued losses, and cash bleed don’t seem attractive at first sight we’ll complement this overview article with one that provides reasons to buy the stock nevertheless as we think things are going to improve pretty rapidly going forward.

Conclusion

This is just an overview of the company. We’ll have a follow-up article coming out soon explaining recent developments and reasons why Par is attractive, stay tuned..