A Quick Take on SKYX Platforms

For an in-depth description of the company see our Primer.

Introduction

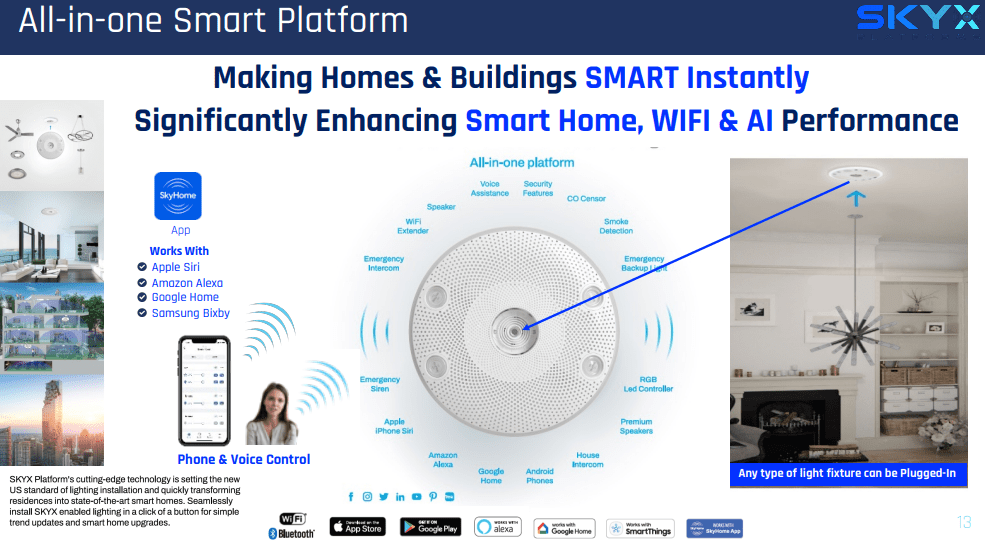

SKYX Platforms is a technology company focused on developing and commercializing advanced, safe, and smart plug-and-play electrical solutions for homes and buildings, centered around their patented ceiling outlet receptacle technology.

The company aims to disrupt the lighting, ceiling fan, and smart home industries with products designed to be easier, safer, and more cost-effective to install.

Reasons to be bullish

Killer patented plug-and-play products bring real installation speed and safety advantages.

The third-generation open smart platform creates a smart house instantly, integrates with existing smart services, and can create recurring revenues from services like communications, fire alarms, home intrusion alerts, emergency response services, and monitoring services. Management believes its products can double the speed and triple the range of Wi-Fi due to the placement of chips in the ceiling.

Razor and blade business model with the receptacle as the razor and the plug-in light fixtures as the blades, locks in customers for repeat business.

The company operates 60+ e-commerce websites that serve as a marketing tool and sell its products.

Given its safety and installation advantages, the platform could become a de facto standard if its use becomes widespread.

Growth

The company is embarking on multiple efforts to increase adoption:

Licensing its technology, for instance to GE Licensing.

Strategic partnerships with the likes of Ruee Appliances, EGLO, Golden Lightning, and JIT Electrical Supply.

Retail chains like Home Depot, Wayfair, Kichler, and Quoizel to expand distribution.

Co-opting insurance companies. Management believes its products can save insurance companies billions of dollars annually by reducing fires, ladder falls, and electrocutions. The company anticipates that insurance companies will start recommending its products once the entire range of its plug-and-play products is completed and could offer discounts on premiums for those that do.

Enlisting builders, like Jeremiah Baron Companies, hotels, and hospitality ventures, commercial buildings like offices, schools, hospitals, and elder living facilities, industrial facilities, rental properties, cruise ships, and retail spaces, where the safety, installation, and smart benefits add value. From Lance Shaner, Chairman & CEO of Shaner Hotel Group:

I clearly recognize SKYX’s extreme value proposition for hotels, buildings, and homes, and its significant global growth opportunity. I am now aligned to participate as a significant long term minded SKYX investor. I strongly believe that SKYX’s game-changing advanced and smart platform technologies will make hotels, buildings, and homes, advanced, smart, and safe instantly, while saving cost, time, and lives.

From the Q3/24CC:

our TAM in the US alone is $500 billion with over 4.2 billion ceiling applications in the US alone. Expected revenue streams from retail and professional segments, include product sales, royalties, licensing, subscriptions, monitoring and the sale of global country rights.

SKYX has filed an application with the NEC seeking mandatory safety standardization for its ceiling outlet receptacle platform and made significant regulatory progress (see our Primer).

New products, like its recessed lights, which is a multi-billion unit market will also go into Home Depot. Builders are also interested.

International growth, with the help of 97 global patents and trademarks, licensing (globally with GE LIcensing), international manufacturing in China, Vietnam, and Taiwan (the latter as back up in case of China problems), and strategic partners like Ruee Appliances. Management is also considering licensing country rights and expanding its sales footprint in some countries in Latin America, Europe and Asia.

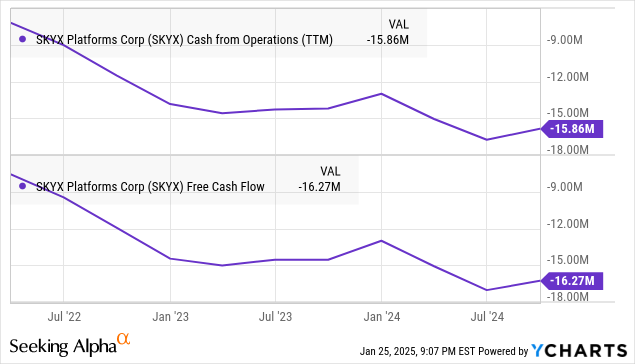

Finance

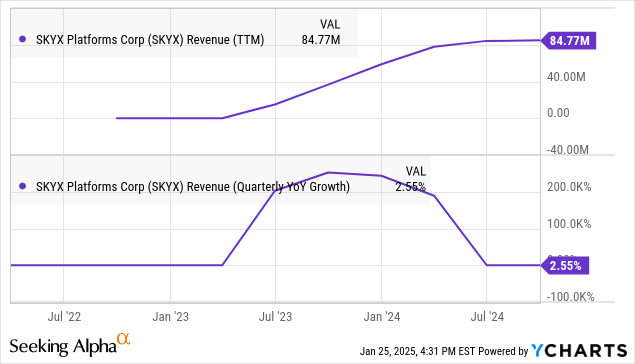

Q3 wasn’t an exciting quarter with revenue growth of just 2.5% to $22.2M. The company is gearing up in terms of production and inventory to start delivering products to partners like Home Depot and Wayfair and sales through its 60+ websites for an acceleration in sales in Q1/25.

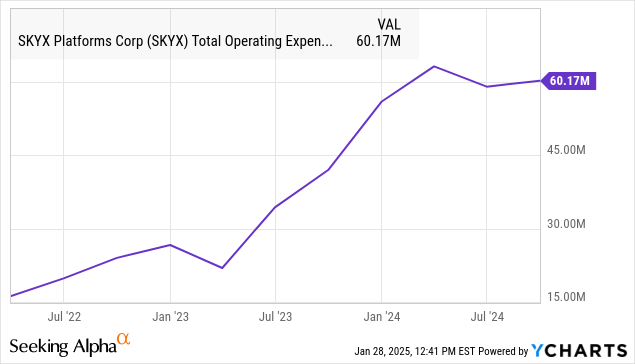

Gross margin increasing 100bp to 30.9%. OpEx is topping in dollar terms:

Operating cash outflow declined by 39% to $2.6M. Cash is a crucial variable at this juncture:

Ruee is helping the company leverage its trade payables to finance operations, enhance its cash position, and lower its cost of capital, which is referred to as the Dell Working Capital Model.

The company had $13M in cash and equivalents, down from $15.6M at the end of Q2. In October 2024, the company secured an additional $11M equity investment led by Lance Shaner, Chairman & CEO of Shaner Hotel Group with considerable insider participation.

Management expects to be cash flow positive in 2025 and expects its products to be in close to 15K US and Canadian homes by the end of 2024, with tens of thousands of incremental homes in 2025.

Valuation

With a fully diluted share count of 156.9M, the company has a market cap of $251M (at $1.6 per share) and an EV of $227M. Given FY25 sales expected at $126.5M the shares sell for 1.8x EV/S.

EPS loss is expected to halve from $0.33 last year to $0.17 in FY25.

Conclusion

This is a high-risk/high-reward play. The company has many elements in place to drive growth in multiple ways and create something of a standard, given the advantages of its platform in terms of safety, installation ease, and smart features.

There is even a chance it becomes a mandatory standard through the NEC, which would mean a huge boon, although this isn’t likely to happen anytime soon.

Given stable OpEx, a growth acceleration could quickly improve cash bleed and the bottom line. Management expects to start generating cash at some point this year and the $24M in cash seems enough to reach that point.

Given the recent runup in the shares, we would wait until there is tacit proof of an acceleration in growth, as the company is gearing up production and inventory.