A Quick Take on Smith Micro

Finally ready to replicate the 2019 success at Sprint 5x over with all investments done

Smith Micro (SMSI) produces white-label software for carriers. Its main product is SafePath 7.0, an advanced family safety platform that has T-Mobile and AT&T as customers launching this year. All the investments and additional cost-cutting are done while the revenue ramp is about to start.

In short

The company will return to producing very high gross margins (80%-90%) requiring little marketing (mostly done by the carriers).

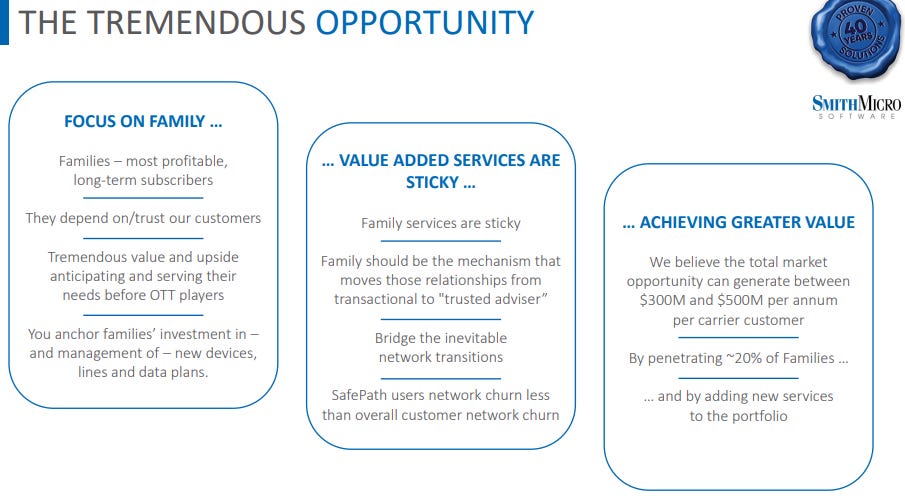

SafePath is a platform with different modules and endless expansion opportunities for generating additional revenue streams.

SafePath has been shown to expand fast when carriers get serious about marketing. At Sprint it scaled rapidly in 2019 (from $2.1M in Q1/19 to $7.85M in Q1/20) until that was cut short in the very early innings by the pandemic and the acquisition of Sprint by T-Mobile.

The integration of Sprint into T-Mobile took years and prevented replication of the SafePath success at Sprint, but it’s now all but done, with T-Mobile ready to launch in the fall.

AT&T is ready to launch in the summer so in H2/23 we are likely to have two Tier-1 carriers launching, together they are 5x the size of Sprint.

There are additional opportunities for ViewSpot, which has been improved to be suitable for the wider retail sector, not just carriers, greatly increasing the TAM.

Financials are set for a secular ramp as all the huge up-front investments (software integration and subscriber migration) are done, while none of the returns (subscriber growth) have yet materialized while the company is already close to profitability on an additional $4M a quarter cost-cutting effort.

The stock has an open-ended upside from expected rapid subscriber growth, to be followed by opening up additional revenue streams an international carrier wins (strongly hinted before year-end 2023) with gross margin expansion and operating leverage to boot.

Additional revenue streams can come from adding services and functionality to the SafePath platform and from the greatly expanded TAM for ViewSpot.

Products

Three white-label high-margin SaaS software packages selling to carriers

SafePath: Family location and safety software

CommSuite: Next generation messaging software

ViewSpot: Dynamic content in-shop marketing software

SafePath

SafePath 7.0 is a combination of its original family safety software and the best part of Circle Labs and the carrier business of Avast, both of which were acquired.

SafePath is a platform, consisting of several modules (SafePath Family, SafePath Home, SafePath IoT, SafePath Drive) which can add functionality and revenue streams, as they did in 2019 with the Sprint tracker.

Had its first big success at Sprint in 2019 until that rally was cut short in the early innings by the pandemic and the acquisition of Sprint by T-Mobile.

New contracts with T-Mobile and AT&T on a revenue sharing per subscriber basis similar to the original Sprint contract

Integration of Location Labs and Avast software is completed, as is the migration of the subscriber base of legacy products.

The big hold-up in the last couple of years at T-Mobile was the integration of Sprint, more especially its billing system, that now seems all but done.

Migrating the Sprint subscribers to the T-Mobile billing system caused Sprint subscribers to run off, producing declining revenues the last couple of years (and the same is true for Sprint CommSuite subscribers). This is now all but done.

Replicating the Sprint revenue ramp

Here is the original Sprint 2019 revenue ramp, in blue:

Investors should realize: 1) This revenue ramp was cut short in the very early innings 2) AT&T and T-Mobile together are 5x the size of Sprint 3) Both have a lot of customers from legacy software providing the carriers to hit the ground running. 4) Recent greatly improved revenue sharing per subscriber contracts signed by T-Mobile and AT&T.

While there is more competition in Family Safety software, Verizon showed earlier this year that carriers can ramp up subscriber numbers fast if they take marketing seriously.

Customers tend to trust carrier software over free retail products like Life360 which sells you children's data.

The company has a virtual monopoly in the carrier market.

With software integration and legacy subscriber transfer now almost completely done, the company can focus again on the roadmap of adding services and hence revenue streams to the SafePath platform.

Verizon

Showed strong subscriber growth for their Avast Family Safety software earlier this year (Avast has been acquired by Smith Micro).

Verizon was supposed to sign a new, much better contract with Smith Micro and move to SafePath 7.0. However, Verizon decided not to do this and embarked on developing its own software instead. This caused the stock price of Smith Micro to sell off from $3+ to $1 in March 2023.

We think that reaction was overblown as the existing Verizon contract is much worse and the risks of losing T-Mobile and/or AT&T are low as these signed new contracts last year and this year respectively.

$4M in revenue a quarter from Verizon will fall away next year, but this revenue was low-margin revenue as it was produced under the old contract Verizon had with Avast, although much of the associated cost have already been cut.

Verizon doesn’t have a great track record building its own software, we’ll have to see how this goes. It’s not entirely inconceivable that they will prolong the use of the Avast software or even come back for the SafePath platform, although there are no signs pointing to this at present.

ViewSpot

ViewSpot is an RDM (retail display management) system and a dynamic pricing system, enabling in-store marketing.

Customers are Vodafone Spain, Tracfone, Alcatel, and Verizon.

It produces minor revenues but it has been significantly upgraded which makes it applicable in the wider retail sector, not just carriers, greatly increasing the TAM (total addressable market).

Management argued during the Q1CC that there is a significant expansion of the pipeline and they expect deals to be closed this year.

CommSuite

CommSuite is a voice messaging platform that is used by the likes of Sprint (now under T-Mobile) and, Boost (now under Dish, and actually could have an opportunity to expand at Dish beyond Boost).

Its revenues have been declining as Sprint subscribers run off when they are transferred to the T-Mobile billing system.

Financials

The past two years have been difficult; revenue has been declining as a result of losing SafePath and CommSuite subscribers from Sprint that were transferred to the T-Mobile network and billing system, and costs have increased due to the two acquisitions, the integration of the three software packages into SafePath7.0 and just mentioned transferring of subscribers.

After Verizon decided not to engage in a new, SafePath7.0-based contract management embarked on a pretty drastic cost-cutting program that aims to shave $4M (from Q4/22) of cost per quarter from COGS and OpEx By Q2/23. It has eliminated 26% of its workforce.

Management guides profitability no later than end of Q3/23.

The company has issued a large number of shares to pay for the acquisitions and integration and migration cost and to pay for the convertible notes ($1.5M a month).

With Sprint achieving a $25M run rate early on (in Q1/20), AT&T and TMUS combined are 5x the size of Sprint and could approach a $100M run rate in high-margin recurring revenues by the end of 2024.

With $35M in OpEx and 85% gross margins that would produce $50M in earnings, with 70M shares outstanding (assuming all convertibles are paid in stock this year, that’s not a given) that would produce a $0.70 run rate which could well be the EPS in 2025.

Conclusion

We see an excellent risk/reward situation with virtually all integration and legacy app migration costs behind us and the two US Tier 1 carriers almost certainly starting serious marketing in H2/23, with AT&T starting this summer.

Revenues will slowly start to ramp while the costs will be stable from Q2 onwards, leading to margin expansion (from 70% in Q1 to 80%+ by H1 next year) and operating leverage.

$4M in quarterly revenue from Verizon will disappear next year. While this was low-margin revenue, the related costs are being decimated (also to the tune of $4M a quarter) so this creates some headwind for H1/23. Depending on the speed of the ramp at AT&T and T-Mobile, H1/23 could see some losses, but these will be temporary.

Additional revenue growth will come in time from new carrier wins, for instance in Europe, new ViewSpot customers which were strongly suggested by management for this year, and adding services and functionality to the SafePath platform.