A Primer on SoFi

One of the most compelling business models in finance

SoFi (SOFI) is a FinTech platform that added an online bank to its business in early 2022 with the acquisition of Golden Pacific Bancorp. Since 2028:

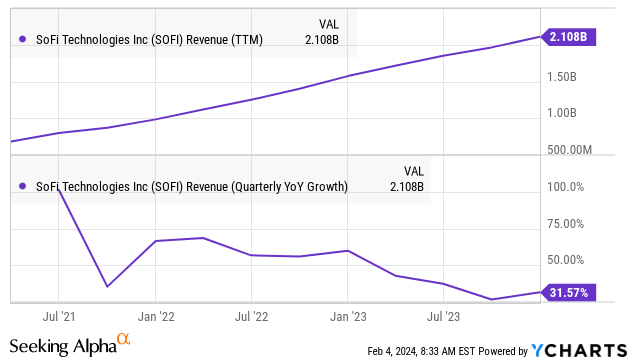

we have grown annual adjusted net revenue by more than 8x, annual EBITDA by almost 3x or $660 million, members by more than 11x, total products by 16x, and consolidated net interest income by nearly 5x [SoFi Q4/23CC]

In Short

One-stop shop FinTech platform that enables the company to introduce competitive products that are rapidly gaining traction.

The company benefits from platform economics producing economies of scale and scope and continuously improving the LTV/CAC (lifetime value/customer acquisition cost) ratio.

Its platform is so good it sells as a B2B business to other financial institutions and sales are accelerating.

Its banking business gains members for its Financial Services platform and offers multiple advantages like low funding cost, flexibility in keeping loans on the book or selling them, and requires no branch network.

The Financial services, and to a lesser extent the Technology Platform segments have reached escape velocity and will produce tremendous operating leverage going forward.

The company is gaining market share and the shares are cheap on a book value basis.

SoFi has three main segments:

Lending is its bank business.

Technology Platform is its B2B business where it let other businesses use its platform.

Financial Services is a rapidly growing platform with members using an increasing amount of financial products and they get tailor-made advice and suggestions based on AI.

Competitive advantage

Financial Services and Technology Platform segments require little or no capital and no credit risk or capital reserves, they will produce huge operating leverage at scale.

The company produces competitive stand-alone products but platform economics ensure the whole is much larger than the sum of the parts through economies of scale and scope.

The company has cheap sources for its lending business with its own rapidly growing deposits and cash flow.

Its bank business serves as an additional funnel for its Financial Services platform

Its lending business is very flexible, management can change rates, and sources of finance, keep loans on the book or sell them, hedge, etc.

The company amasses massive amounts of data dat feed their Financial Services platform algorithms and credit risk assessment.

Let us flesh out some of these:

Competitive stand-alone products

The company experiments with new products until they hit a winning formula.

For instance, SoFi Money doesn’t charge account fees on checking and savings accounts and provides very competitive rates.

SoFI Invest enables users to access IPOs at IPO prices.

Bank

Its bank business offers the following advantages:

Deposits provide a low cost of funds, in the order of 200bp below warehouse facilities, and SoFi can change them at will

Increasing the flexibility to hold loans or sell/securitize them

Supports origination volume growth with additional financing option

Deposits provide meaningful customer data.

It contributes to strong growth in SoFi Money products.

Flexibility

Sell/securitize loans versus keeping them on the book.

Decrease/increase their deposit rates to preserve or expand NIM/expand deposits

Shift marketing efforts between lending and Financial Services depending on circumstances.

Platform economics

Economies of scale; increasing revenue over a largely fixed cost structure.

Economies of scope; leveraging the platform with additional products, opening up more cross-selling opportunities.

Additional products create more entry points for winning more customers (for instance its Lending business has boosted the use of SoFi Money).

CAC (customer acquisition cost) will be progressively lower for new products as they can be marketed to existing members at the same time as it increases the LTV (long-term value) of customers.

From a presentation at GS: “We make about $800 in LTV day one if it's a new member. If it's a cross buy member that comes in through Relay at a very low CAC or comes through Invest or comes through Money, that profit goes from $800 to $1,600 to $2,000.”

Growth drivers

The relentless rise in members and products is creating a virtuous cycle (or flywheel effect) as more products create more entry points and increase the value proposition of the whole package while lowering CAC and increasing the LTV.

The growth is secular, not cyclical. The vast majority of growth is gaining market share.

From the Q4/23CC: “we have grown annual adjusted net revenue by more than 8x, annual EBITDA by almost 3x or $660 million, members by more than 11x, total products by 16x, and consolidated net interest income by nearly 5x.”

Lending Services

Three segments: Personal Loans, Student Loans, and Home Loans

Mostly HFS/HFT (Held for Sale/Trading), some HFI (Held for Investment)

HFS usually after 6-7 months of origination.

3 Funding sources:

1) Own cash.

2) Deposits.

3) Warehouse facilities (debt issued/debt repaid).

SoFi still gets all the interest payments from all the personal loans they ever originated that haven't been repaid (or defaulted).

SoFi can rebuy their loans after 6-7 months if these are safer than the ones they can originate.

Roughly 68% of its loans are unsecured (Q2/23).

They service al Personal Loans that have been originated (and not repaid or defaulted), irrespective of whether they have been sold or securitized.

End goal: 50% profit margin.

Constraints on Lending Business

Capital ratio: improved to 15.3% in Q4/23 from 14.5% in Q3/23, has considerable margin (the requirement is 10.5%)

Loan demand isn’t a problem either

Financing, they have multiple options (cash flow, deposits, warehouse), no constraint.

Credit quality isn’t a problem, from the Q4/23CC: “Our personal loan borrowers weighted average income is $171,000 with a weighted average FICO score of 744. Our student loan borrowers’ weighted average income is $154,000 with a weighted average FICO of 781.” Delinquency rates are moving slowly back to pre-pandemic levels with life of loan losses at 7-8%.

None of these constraints seems particularly binding at the moment, the company could expand its loan book (or sell loans) at a higher rate and indicated that there is $18B-$20B of capacity to increase origination.

They are choosing some contraction in FY24 to 92-95% of FY23 volumes as management expects a recession this year.

Credit risk mitigation

The loans have a fairly short duration.

SoFi tends to sell loans (usually after 6-7 months).

Securitization (risk isn't entirely gone here there is residual risk retention debt and in some cases securitization debt).

Whole loan sales, cuts all risks and obligations.

Interest rate hedging (interest rate swaps).

They also have and collect lots of info about borrowers.

They seek borrowers with relatively high incomes and credit scores.

They can also buy back loans they sold as they might very well be safer than new loans (as they are closer to maturity and have established a track record of servicing).

Securitization

Requires third-party ratings and additions of loans to compensate for possible default and prepayments (above the modeled amount).

It doesn’t eliminate all risks; it generates risk retention debt.

Some securitizations remain on the balance sheet (as securitization debt), but are paid by the borrowers.

NIM

They are flexible as they both control their deposit as well as lending rates.

The Net Interest Rate margin has actually trended up lately:

Financial Services

Is a typical FinTech platform business requiring little or no capital and not incurring any credit risk or requiring capital reserves

Despite the rapid rise in members, financial products per member remained stable at 1.5x illustrating that there are still tremendous opportunities here.

A host of products are on offer like Money (combining checking and savings accounts), Invest, Relay, Protect, Wealth, Credit Card.

A company using data and AI to tailor offerings to members.

Rapid growth in members (those that have ever used a product) and products (the aggregate number of lending and financial services products that members have selected on the platform since inception). These definitions are cumulative and therefore likely to overstate active members and product use.

It added 585K members (+44%) to 7.5M and 695K products (+41%) in Q4/23, but the segment has reached escape velocity and grew 115% and produced a $25.1M contribution profit (which margin expanded 1500bp to 18% sequentially showing tremendous operating leverage).

FY23 segment revenue of $437M is 2.6x the $168M of FY22.

There is more to come, two products (Credit Card and Invest) still produce significant losses but these businesses will scale and there are still plenty of economies of scope to be reaped with the average member using just 1.5 products (up from 1.1 in Q1/19) but it has been stagnant for a year, which is a little disappointing.

Technology Platform

B2B segment where they provide its platform to other companies

Acquired Galileo, a payments platform in 2020

Technisys acquisition in Q1/22 (with clients mostly in Latin America) opened up the market for big financial institutions as it is a multi-product core banking platform).

Galileo and Technisys are merged.

Monetization; 1) Up-front implementation fees 2) Flat transaction fees 3) Subscription fees

Apart from B2B monetization, the platform also enables SoFi a low-cost way to innovate and introduce new services, from the GS presentation: “So having the Tech Platform allows us to control our own destiny, innovating faster than we could by just using other people's technology. It also gives us an opportunity to be a low cost operator and being a low-cost operator typically becomes a competitive advantage.”

Growth is accelerating to 13% in Q3/23 and guided to the mid-20s going forward while most of the development costs are in the rearview mirror, producing great operating leverage.

End goal: 30-40% profit margin.

New Products

Recent product introductions are:

IPO at IPO prices (SoFi Invest)

By Now Pay Later

Alts SoFI; alternative investment and mutual funds (SoFi Invest)

Finances

Lending is guided to contract in FY24 (to between 92-95% of 2023 volumes as management is preparing for a recession) but the slack is taken up by Technology Platform and especially Financial Services, which together are guided to grow 50% in FY24.

Valuation

The company is expensive on a p/e basis but given the tremendous operating leverage especially in the Financial Services segment, this will come down. Indeed, management believes that they can produce $0.55-$0.80 in EPS in 2026.

As Stone Fox argued, we should be looking at adjusted EBITDA as most of the adjustments are non-cash charges and/or one-offs.

We think the company is cheap on a book value as it trades at a similar book value as JP Morgan but growing much faster and with more operating leverage.

Risk

SoFi avoids CECL provisions at origination (reservation for credit losses) as it qualifies them as AFS (Available for Sale), avoiding a 7-8% CECL loss in the quarter of origination 2) recognizing a fair-market value gain on the loan 3) Generating net interest income immediately.

SOFI is recognizing a day 1 profit of ~4.3% (this is Gain On Sale Margin or "GOSM") whereas peers are required to provide for loan losses of ~7%. . This is merely a timing difference and it reverses over time but it is especially beneficial to SOFI during the ramp-up stage of lending. [Source: IP Banking Research]

As long as SoFi "intends" to sell the loans it can classify the loan as AFS.

This might have been seen as a potential problem recently but several sales and securitization deals in Q4 have put this risk to bed, in our opinion.

Credit quality could deteriorate in a worsening economy but we’ve set out above that they have multiple ways of dealing with this. One way is to loan less, which is what the company is planning to do in FY24 as management believes the company will be hit by a recession.

Reasons to buy

Rapidly rising membership and financial products.

Innovative financial products, adding new ones regularly.

Platform economics: economies of scale and scope, especially financial products which also bring down the LTV/CAC ratio with more members and financial products.

Deposit advantage versus fintech (and reason for an increase in NIM).

Not having to maintain a branch network is an advantage over banks.

Offering attractive rates, winning market share.

Secular growth, most growth from winning share.

Amassing massive amounts of data with which to personalize offerings and advice and reduce credit risk.

Financial Services have reached escape velocity and will produce tremendous operating leverage.

B2B Technology Platform accelerating growth and leverage.

The company has many levers to maintain the NIM.

Revival of student loan business.

The shares are cheap on a book value basis.

We have updated the finances in a recent (July 2025) Quick Take: https://shareholdersunite.substack.com/publish/posts/detail/167690776?referrer=%2Fpublish%2Fposts