A Quick Take on SurgePays

Likely to keep on surging..

In short

Here is what you need to know about SurgePays (SURG). The company has a legacy business selling mostly low-margin third-party fintech products through a network of 8K local convenience stores for underserved and underbanked people.

Growth took off last year as the company ramped subscribers for its MVNO (Mobile Virtual Network Operator) on $30 per household subsidies from the ACP (the Affordable Connectivity Plan).

A virtuous cycle can ensue as the company is using the ACP to increase its network of third-party community shops and using the network of shops to sell its ACP subsidized MVNO subscriptions,

All the while reducing costs as it directly sourced cheaper tablets in China and selling the subscriptions through their shops greatly reduces CAC (customer acquisition cost) and increases retention.

The company is profitable and generates cash. The shares are at $6 and change selling at 0.65x EV/S, we think they could easily go double digits. The warrants look even better.

There is some risk when the ACP runs out of money somewhere next year, but it had bipartisan support and the company is using the ACP to quickly bolster its legacy business.

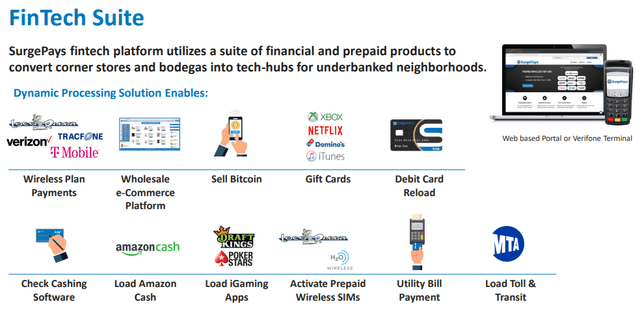

Network of partner community shops

The company has a legacy business selling third-party products (also selling prepaid cards for their own MVNO mobile telecom business) and services through a network of 8K local community shops and bodegas that serve the underbanked.

Explosive mobile broadband subscriber growth

A relatively new business is offering mobile broadband services to underserved Americans, for which they get $30 per month in Federal subsidy per subscriber under the ACP, the Affordable Connectivity Plan.

There are 48M US households that qualify, providing an idea of the TAM (total addressable market).

Per latest data, there were 18M households on ACP subsidies

In December last year, the company had just 30K subscribers, which rose to 150K in mid-July as the acquisition of Torch Wireless enabled them to market in all 50 states and generate economies as they have their own MVNO (Mobile Virtual Network Operator) mobile telecom business using the T-Mobile and AT&T networks.

They have automated marketing via bots on Facebook and acquired Shockwave, a sophisticated CRM cloud software, greatly easing the sign-up process (and directly connecting with their MVNO carriers and the FCC).

The company had 250K subscribers at the end of Q1 after two-quarters of relative stagnation as they arranged $25M non-dilutive receivables-based financing to buy (in the order of 300K) tablets in bulk in China.

These tablets are now arriving in large quantities, producing two advantages, much lower cost ($25-$28 per tablet) and removing barriers to growth as they are not going to run out of tablets anymore.

They will also start to sell mobile broadband subscriptions through their network of partner shops (see below) which:

Bolstering their legacy business

Late last year the company hired a manager, Jeremy Gies, specifically tasked to expand the network of partner shops.

The company is using the ACP subsidized broadband subscription as a way to get more shops on the network (it's easy money for the shop owners and the shop clientele is a prime target for this service as many are on SNAP and they can even use their SNAP card to sign up).

Three recent distribution deals:

1) GPO Plus

There are other opportunities (Q1CC): "We've got some other integrations that are going to be really interesting where we're working with eight independently owned ATM Company software where every time somebody swipes that reloadable debit card, kind of a given that customer doesn't have a checking account, most likely they're on some type of government benefit. Being able to ask them on the screen of the ATM, if anyone in their household is on government benefits and then being able to secure their mobile number through the ATM."

How fast can they scale the number of shops?

It takes some effort and cost to add shops to their network, from the Q1CC: "Right now, as all of these the components of bringing on a chain of stores or stores are, you've got to get your point of sale materials out, the poster, the door sticker, the gas pump starburst, the little rack card that sits up by the cash register that creates awareness for people that, hey, are you on government benefits? Well, you're entitled to this one as well. Ask at the register. That's very, very important."

They have a target of 13K shops by yearend but have a pipeline of 25K shops and are taking action to increase the speed of onboarding (making instruction videos, hiring 6-8 training and support staff, stuff like that).

From the Q1CC: "There's certain networks out there that we may look at taking over, acquiring that are just simply networks where people are doing one-off products to convenience stores where we can basically buy their pre-existing relationship of 100, 500 to 1000 stores, 2000 stores, then deploy our entire suite of products on that store, meaning that network has a much higher value to us as a Company than it did to that one-off product Company.

Competitive advantage

They have a capital-light business model, they don't own the shops, they don't own the telecom network infrastructure.

The company bought a CRM program, Shockwave that is integrated with the FCC's database and also AT&T and T-Mobile (their MVNO network providers).

The company is the only ACP Company that can sign up ACP subscribers through a national network of convenience stores.

Signing up ACP subsidized mobile broadband subscribers through their shop increases their retention rate and decreases attrition cost.

Expanding the network of convenience stores gives them an unprecedented position to serve the underbanked and underserved communities where they shop and makes the company increasingly attractive as a partner. This position can be leveraged in an almost unlimited way.

Better unit economics

Buying tablets in bulk in China is significantly increasing the one-time profit they make on the tablets as the cost fall from $93 to $65, that's a $28 per tablet improvement.

Signing up new ACP subscribers through their partner shops significantly lowers CAC (customer acquisition cost) to just the incentive for shop owners, $10-$12 per subscriber for in-shop sales versus $50 per subscriber for mobile tent sales, that's a $38-$40 improvement per subscriber (although there is a small recurring fee for the shop owner as well).

Reduce attrition as customers trust these shops they visit daily and have somewhere to go with problems or questions (the tent sales are mobile events, they pack up and leave after a week or two).

Reduce attrition costs. Replacing them with new subscribers through their shops and providing them with cheaper tablets is now $60+ cheaper per subscriber. New subscribers could very well be profitable almost instantly as the profit on the tablet might outweigh the CAC through the shops.

Offer family members of ACP customers (limited to one ACP subsidy per household) their prepaid MVNO service.

Finances

Q1 results

Revenue +64% to $34.8M

Gross profit +192% to $7.7M

Gross margin 22.1% (up from 12.5% in Q1/22)

SG&A -22% y/y

Net income $4.5M versus a loss of $1.2M in Q1/22

EPS $0.32 versus -$0.10 in Q1/22

Other notable items

FY23 revenue guidance $190M+ with positive cash flow

Cash $8.9M (versus $7M at the end of Q4/22)

Receivables +400K q/q to $9.7M (these are government receivables from the ACP)

End-of-year guidance: 500K+ mobile broadband subscribers and 13K+ partner shops

Risks

There is a fairly large (but declining) short position. However, there is a much larger insider (39%) position (and insiders have been buying).

Attrition is a risk but it can be reduced by educating subscribers that they can use the chip in their mobile phone as well (rather than just the tablet), and by acquiring subscribers through their partner shops. Also, attrition costs are greatly reduced by the increased profits on the tablets (down from $93 to $65) and the reduced cost of acquiring customers through their partner shops (down from $50 to $10-$12 per subscriber plus small monthly payment for the subscriber keeping on the network).

ACP could run out of money in the not-so-distant future (there is $9.1B left and monthly they add $300M-$400M), and will to be renewed. It had bipartisan support and it would be difficult to throw so many people off the internet.

Rapidly increasing the number of partner shops can revive their legacy business which would derisk the dependence on the ACP:

It makes the network more attractive for other deals and increases their bargaining position. They can also offer their own products, like their MVNO prepaid mobile service and there has been talk of partnering with a telehealth company.

Recession is actually positive for the company as they offer value to customers and no need for inventory, just direct transactions for shops

Valuation

Q1CC: "net mobile being purchased for over $1 billion with just over 2 million subscribers." If they reach the guided 500K subscribers their mobile broadband business alone could be worth $500M (5x the current valuation), but the dependency on the ACP might make investors a little more cautious.

On the other hand, if the ACP gets extended next year it could go well beyond 500K subscribers and in the meantime they are rapidly boosting their legacy business, de-risking the dependency on ACP

Management is guiding for 500K+ subscribers by yearend, which would produce a run rate of $180M just for their mobile broadband business, at 50% gross margin (ACP is $30, the MVNO cost are $15 per subscriber) that's $90M gross profit.

The shares trade at 18x Q1/23 EPS ($0.32). EPS should improve later this year due to the cost decline of tablets and more subscribers sign up through their partner shops.

OpEx runs at $12M a year today, and will probably increase a little so that's a pre-tax profit of roughly $75M or $3-$4 in EPS after tax (there are just under 20M shares, fully diluted). This would be the end-of-year run rate, not the FY23 result which will be a lot lower due to the continuous buying of tablets and other one-time costs.

Analyst average price target is $12.25.

Conclusion

Rapidly expanding mobile broadband business (250K subscribers already) with their own MVNO backed by $30 per month ACP subsidies while MVNO costs are $15 per subscriber and a one-off $90 per tablet.

Using ACP subscriptions to boost the number of partner shops for their legacy business selling fintech products through a network of local community shops and bodegas serving the underbanked.

Using government ACP receivables to obtain $25M financing to buy tablets in bulk at $65 rather than $92 and resolve the shortage of tablets that has throttled subscriber growth.

Selling ACP subscriptions through shops boosts relationships with the customer, reducing attrition and acts as an incentive to attract more shops to join, as well as producing a significant cost advantage ($10-$12 per subscriber versus $50 through ambulant tent-based campaigns). This strategy is already working.

They have 8K shops in the network but there is a pipeline of 25K shops for joining the network.

Unit economics are given a big boost by the $25+ additional profit on the cheaper tablets and the $35+ gain in CAC selling broadband subscriptions through their shops but these benefits will appear only gradual throughout the year.

FY targets $190M in revenue, 500K mobile broadband subscribers and 13K shops.

We see a revived legacy business expanding the network of shops, closing new deals and sell non-ACP subsidized MVNO prepaid cards to family members and a host of additional opportunities.

The shares are cheap, fully diluted they're selling at 0.65x FY23 EV/S (at $6.10 share price).