A Quick Take on urban-gro

urban-gro (UGRO) is a turnkey design-build company for the CEA (controlled environment agriculture) sector, where it realized most revenue from the cannabis segment.

We issued a buy alert for our Seeking Alpha marketplace on November 30 at $1.14 as we argued the shares are a recovery play.

The company suffered from a slump in the cannabis market, which was its main segment and growth engine.

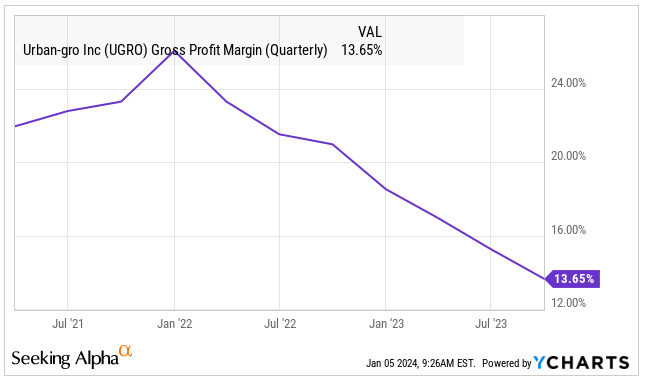

Not only did the Cannabis slump affect revenues, it also affected gross margins as well as sales in the cannabis segment were often accompanied by high-margin equipment sales:

However, we saw reasons for a recovery:

The company has been successfully diversifying away from the cannabis market to new markets, opening up whole new segments like the industrial, commercial, hospitality, recreation, education, and healthcare segments.

Normally it competes in these segments against much bigger companies but it has found a niche in the $10M-$30M turnkey project range which is too small for the big companies and brought the expertise of JT Archer as COO to drive these projects.

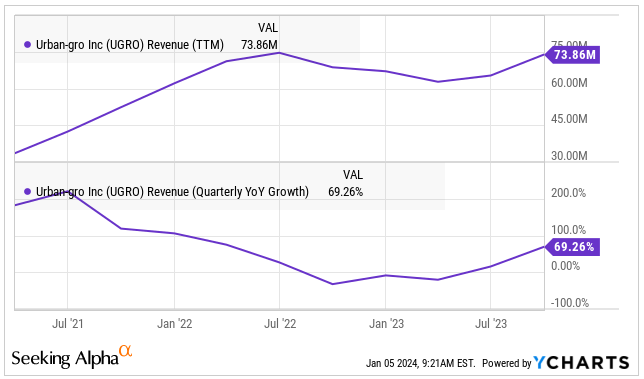

The diversification has been so successful that its Q3/23 revenues ($20.9M) were within a whisker of its all-time best quarter ($21.1M in Q1/22).

Will the recovery last? We think there is a good chance:

1) Over two-thirds of Q2 and Q3 revenue was generated outside the CEA market.

2) The company increased backlog by 6% ($5M) to $84M in Q3/23, despite taking out 27% of their backlog during the quarter (by finishing projects).

3) Revenue increased spectacularly:+11% q/q and +69% y/y to $20.9M.

4) Revenue is going to do even much better in Q4 where it is guided at $30M and, perhaps even more importantly, management expects the company to reach AEBITDA neutrality in Q4.

So basically the company doesn’t really need the cannabis segment to revive growth.

Cannabis revival?

We’re not counting on an imminent cannabis revival, but it should be pointed out the company still generates revenues from the segment.

Management has pointed out that customers are waiting for licenses in multiple states, a process that will gradually clear.

There are wild cards, like the possible passing in Congress of the Safe Banking Act, which would allow banks to provide services to the sector in states where cannabis is legalized.

The company still gains significant new contracts in Cannabis, like the $8M contracts in October 2023 and a $20M contract at the start of 2024.

A cannabis recovery would not only add to the already blistering revenue growth, but it would also increase gross margins as equipment sales recover.

Financials

Q3/23 revenue was $20.9M, 69% higher than in Q3/22.

The guided $30M revenue for Q4 amounts to 43.5% sequential revenue growth.

While gross margins are down on the loss of equipment sales to the cannabis segment, there is a great deal of operating leverage with OpEx declining in dollar terms, OpEx is now on a $24M run rate:

Management guides reaching adjusted EBITDA neutrality in Q4 and argues that they can support up to $40M in revenue per quarter with current OpEx.

Cash is the biggest risk with just $4.8M left and the company still losing cash $6.5M in operational cash outflow for the first 9 months of 2023.

The company arranged a $10M interest-only credit facility for working capital.

Valuation

The fully diluted share count is 13.1M, which at $1.70 per share produces a market cap of $22.27M and an EV of $17.5M.

With FY23 revenue guided at $86.5M, the shares are trading at 0.2x EV/S (and 0.15x EV/S for FY25).

Conclusion

The company has diversified successfully away from the cannabis market, revenues have reached previous highs and will soon surpass these.

While gross margins are still down, OpEx has been reduced producing considerable operating leverage with the company projected to reach adjusted EBITDA breakeven in Q4/23.

Cash is the main risk with just $4.8M left but the cash burn will greatly diminish with the strong revenue growth and operating leverage, and the company has concluded a $10M non-dilutive financing.

While surfing the successful diversification, even a modest recovery in cannabis would be icing on the cake as it will increase gross margins as well as growth. That latest $20M order shows that the company still generates significant wins in the segment.