Aehr Test System Turn-around

Time to buy?

For an introduction to the company and its business model, see our previous article published earlier this morning.

In short

Backlog and billings recovered in Q3/24, providing some near-term stability.

While presently in a dip, the company benefits from strong secular tailwinds as wafer-level testing is gaining traction in large, fast-growing applications (like SiC, SiPh, storage, NAND memory) and end markets (EVs and EV charging stations, 5G, alternative energy, cloud computing, and AI).

The customer base is broadening and the company is entering whole new segments.

The EV market will recover and SiC-based chips are relevant in other segments besides EVs.

Growth

The company experienced a significant decline in the past couple of quarters:

This is mostly on fewer orders from its biggest customer, ON Semiconductor (ON), good for up to 80% of Aehr’s revenue, the result of a slowdown in the EV market.

But there are signs of a recovery, bookings ($24.5M in Q3, up from $2.2M in Q2/24) and backlog ($20M, up from $3M at the end of Q2/24) recovered strongly so there is some basis for a more immediate recovery.

The company is broadening its customer base and entering whole new segments, below is an update on the segments.

SiC

While EV growth has been disappointing lately EVs are getting cheaper, and they last much longer in principle as they have far fewer moving parts.

In April 2024 Aehr received a first order from a new customer in the SiC segment, dependence on ON Semi is reducing.

SiC powerchips are not only used in EVs, but also in EV charging stations, alternative energy, industry, etc.

GaN

Aehr has introduced a new high-voltage machine that is extremely relevant for GaN chips and has already received some orders for this product.

See our previous article for the difference between SiC and GaN power electronics, they are complementary.

SiPh

Aehr currently has six customers using their systems for production tests of silicon photonics devices.

In the future optical chips can open up another huge market, especially in the AI infrastructure:

Recent developments

What got investors’ attention was a slide in an 8-K filing indicating new developments (the last three items):

Three additional slides have more detailed information. The first describes the new storage device opportunity including a major new customer and order.

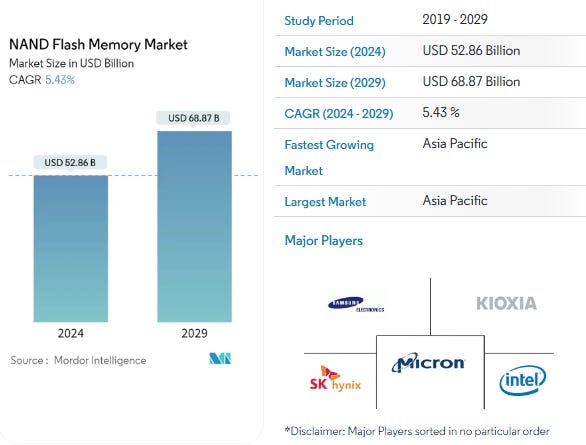

And perhaps even more interesting, the huge NAND flash market is starting to open up for the company

As a reminder, the NAND flash market is enormous:

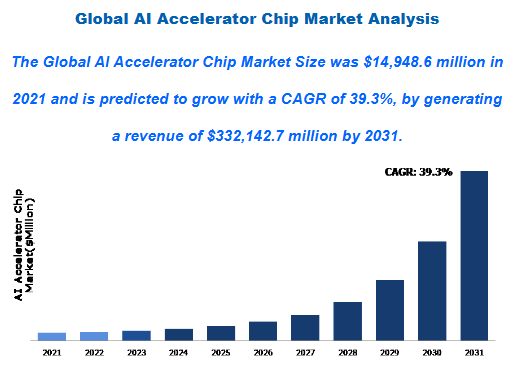

And if this isn’t enough, how about the AI accelerator market, which hasn’t even been mentioned by management so far:

This market is enormous and growing at a breakneck pace, with pacesetter Nvidia:

The sheer numbers will likely be smaller as these AI chips are terribly expensive ($30K-$40K each for Nvidia chips), but this is still a very interesting opportunity.

Not yet very concrete is the DRAM market but the company has had talks with several players and in time this could open up another huge market for the company.

Conclusion

SiC and ON Semiconductor are still responsible for most of the revenue, which has dipped due to slower growth in the EV market, but the EV market will recover, Aehr is getting additional SiC customers and SiC isn’t just relevant for EVs.

The company is broadening out its customer base both within SiC as well as venturing out in additional segments like GaN, SiPh, storage, NAND memory, and even AI chips, but this is a gradual process that will occur over multiple quarters and years, one has to keep that in mind.

However, the recovery in bookings and backlog should ease investor concern and significantly increase the risk/reward ratio, we think the worst is behind us even if additional softness in coming quarters from the EV market and ON Semi are well within the realm of possibility.

As noted EV is the bread winner and auto manufacturers have pulled back. That said EV is the future. Now with these other revenue streams which really were not present at the prior highs the momentum could go much higher than prior highs over the next 2-3 years.