Some comments to Jonah Lupton's article about Alarum Technologies

Not in disagreement but does he realize the very modest valuation?

The article can be found here but only for paid subscribers, but we feel we have to make some additional perspective:

Jonah: “Speaking of revenues, this year ALAR is expected to do $36.7M which is a 38% increase over last year”

Comment: Alarum is likely to do MUCH more than $36.7M in FY24. Focusing on the company growth obscures the fact that NN is growing at triple-digit rates (150% in FY23, 139% in Q1/24). Using company figures greatly underestimates the actual growth as company growth includes the (one-off) running off of the consumer business.

NetNut did $8.1M in Q1 already (+$300K for the consumer business), we will have preliminary Q2 data pretty soon and these will likely take us to $9M+ for NetNut, as management already argued during the Q1CC that the trends continued in Q2. Unless there is a pretty substantial slowdown in NetNut’s growth in H2, we’ll be well over $40M for FY24.

NetNut growing at triple-digit rates also implies they are rapidly gaining market share.

Jonah: ALAR had 38% EBITDA margins which looks pretty good next to 47% revenue growth.

Comment: Again, 47% is the growth of the company, greatly depressed by running off their consumer business. NetNut growth was 139% and NetNut is now the company ($8.1M of revenue from the $8.4M in company revenues in Q1)

Jonah: Unfortunately ALAR has already had a massive bounce off that recent drop and I have no interest in chasing at these prices.

Comment: You’re right not to chase IMHO, but as you discuss later in your article, the reasons for the crash on June 18 (from $33 to an intraday low of $23) was based on fake news (see comment section here) regarding competitor Oxylabs moving on Alarum’s turf (ISP proxy’s). Oxylabs was already in ISP proxy’s for years and ISP proxy’s are a very minor revenue source for Alarum anyway, as you rightly state.

However, you don’t discuss the reason for the sudden revival, Louis Navalier touting the stock. He has a massive following so it is bringing a massive new population of investor eyeballs on the stock, and these are more likely to be investors rather than traders.

Navalier has only taken the stock back to $40+, it was already at $40 before him, and preliminary earnings will be out within the next ten days which will likely be much better than the rather tame Wallstreet expectations (which were massively wrong in Q1).

Jonah: I suspect the 166% NRR is a result of new product launches like the SERP scraper in late 2023 and the website unblocker in early 2024.

Comment: No it’s not. The new products still generate very little in terms of revenue (per the Q1CC), which makes the NRR of 166% all the more remarkable as it’s almost entirely based on customers starting out small (basically sampling) and then greatly expanding usage (as explained here).

Jonah does seem to realize this later on in his article: “NRR of 1.66 is a pretty incredible rate, suggesting that churn is minimal and that the usage from existing customers is accelerating at a rapid pace.”

Jonah: If the data collection market does indeed grow at a 28% CAGR over the next 5-6 years, and ALAR doesn’t run into any legal/regulatory problems, then it’s very possible they could grow revenues at a similar clip with very attractive margins.

Comment: The company isn’t likely to run into regulatory problems: 1) Bright Data won cases against Meta and Twitter. 2) IPPN networks like NetNut enable the scraping of public data. 3) Data collection is too important for the economy (Generative AI is our best hope to revive economy-wide productivity growth) and there is too many powerful interests behind this to keep this flowing. 4) The model that is likely to emerge is LLM’s paying for the training data, this is already happening.

Jonah: according to Grand View Research, the global data collection market will grow from $2.2 billion in 2022 to $17.1 billion by 2030 at an incredible compound annual growth rate (CAGR) of 28.9%.

Comment: These figures don’t include the emergence of LLMs, which is a new important growth segment for the likes of NetNut, market growth is likely to remain very high for the foreseeable future. Add NetNut gaining market share and one might want to take this onboard in valuing the company.

Jonah: To protect the data, websites will do everything possible to block AI products from collecting this data and feeding it to their models. NetNut is a net beneficiary of this trend, as it can enable AI products to overcome these obstacles.

Comment: Agree! LLM’s are a new and important growth segment, but one should take this onboard in evaluating the company.

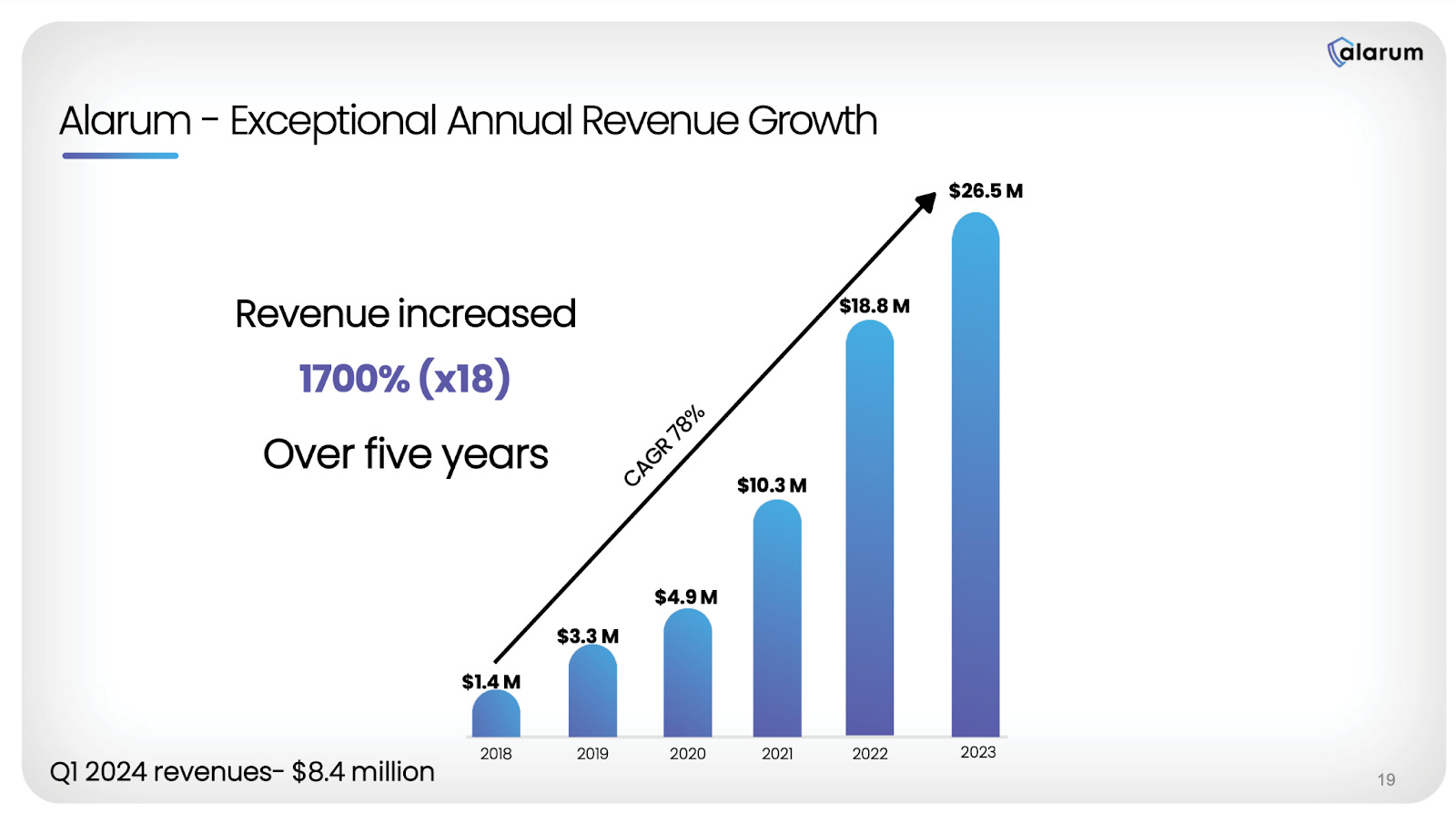

Jonah: Alarum has seen tremendous revenue growth in the past five years, growing from $1.4 million in 2018 to $26.5 million in 2023. This is an over 1700% increase in just five years.

Comment: thanks, it’s worth stressing this, but the growth of NetNut was considerably higher than that still, especially last year (150% for NetNut versus 41% for the company as a whole as the consumer business ran off).

NetNut benefits from rapid market growth and gaining market share and there is no reason to see these trends reversing anytime soon, given the emergence of LLM training as a new additional source of growth.

But given this, we’re surprised by his valuation exercise, which doesn’t seem to take the massive growth and profitability onboard, at least not entirely (see below).

Jonah: With the introduction of the AI Scraper, NetNut is changing the game. This technology automatically learns the design of websites, allowing fast and simple data collection with maximum data accuracy and around-the-clock updates. Most importantly, almost zero human hours are needed to correct something after collecting the information.

Comment: Indeed! This upcoming product promises a lot as he rightly points out even if it’s a 2025 story but likely to be a source of differentiation as well as reducing costs (through automation).

Jonah: Unfortunately ALAR has already had a massive bounce off that recent drop and I have no interest in chasing at these prices. If the stock pulls back then I might have some interest. ALAR is already up 437% YTD so please be careful. If you do start a position, don’t be reckless and don’t be afraid to use stop losses.

Comment: Right not to chase! Stop losses, dunno, one can be stopped out on fake news or volatility and not getting a chance to get back in lower if one isn’t online and following the markets all the time.

Our main problem with the article

At various points, Jonah seems to realize NetNut is growing at triple-digit rates, and has an incredible NRR of 166%, mostly caused by new users greatly expanding, and generating great margins (which are likely to increase with the upcoming AI scraper). He also touts LLM training as a new significant source of growth.

However, his valuation seems to be based on the one Wall Street analyst which has already been proven way too pessimistic in Q1, and company growth figures which greatly underestimate the actual NetNut growth as explained above.

We ask, is a company growing at triple-digit rates taking market share, producing a 166% NRR in an industry that will continue to grow fast for the foreseeable future, generating 78% gross margins and 38% EBITDA margin, producing cash and GAAP profits with new products gaining traction and additional ones coming up.

Q1 EPS was $0.45, given the triple-digit growth and operating leverage, it’s likely to be well above $2 which gives the company a 15x earnings multiple at most. Given the characteristics of the company we just mentioned (and the fact that it generated $3.4M in operating cash flow, has $15.1M in the bank and almost no debt), that seems very modest to us.

Lupton is fine but he doesn't go deep enough. The writeups are good as an initial kind of "basic+" but they are can't be called definitive.

@shareholdersunite Any info on what is causing the pressure on ALAR price? Political pressure maybe?