Weekly Update 20

We discuss runs in some of our recently featured stocks like LFMD, HIMS, HYDTF, and INVE.

The markets

While the markets keep ignoring the Strait of Hormuz, which we find rather baffling, as the stress to the world economy, already visible in large parts of Asia, is going to ratchet up pretty quickly with the last tankers that left the Gulf before the war have reached their destination.

Faith Birol, head of the IEA (International Energy Agency), argues this is worse than the three past oil crises combined, and it’s not just oil, it’s diesel, kerosine (doubling in price, leading to many cancelled flights already), fertilizer (which will cause inmense hardship next year as crop yields decline and small farmers can’t pay for fertilizer, even if they can get hold of it), helium, and lots of other stuff and second round effects (higher transport costs, for instance).

We could go on, but basically, we are sailing straight at a gigantic iceberg and have weeks to change course. As we argued from day 3 of the war, time is on the Iranian side, not ours, a point which they just buttressed by not even showing up for negotiations in Pakistan.

We don’t see an immediate offramp (which doesn’t mean there isn’t one, needless to say), apart from giving in to some of the Iranian demands (end of sanctions, stuff like that), because it very much looks like they’re not playing ball. They can’t be easily bombed into submission either, that should be pretty clear by now, if it wasn’t already. Besides, stockpiles of US critical weapons are at dangerously low, and the US blockade doesn’t seem to work very well.

Inmense damage has been done to Gulf economies already, with 60 oil and gas facilities (and even data centers) damaged, export earnings drying up, and tourism and transport hubs of the Emirates (25% of the economy) plunging even more than their oil & gas revenues, with hotel occupancy in Dubai at 20%.

The US Treasury had to organize an emergency dollar swap facility for the Emirates, which tells you everything you need to know. With the recycling of petrodollars drying up and even reversing, as some of these states will have to tap into their Sovereign Wealth Funds to rebuild their economies, this could quite easily spread.

Gulf finance is an important source for the epic AI data center buildout, and private equity is another one, which is already under strain as not everybody is convinced the sums add up.

Private equity is very vulnerable to a sudden decline of confidence; they’re basically shadow banks, unregulated, with liquid obligations but largely illiquid assets. Some funds like Blue Owl have already made redemptions as good as impossible, and they are unlikely to be the only ones under stress. We don’t know, as these funds are ‘private,’ so transparency is not their priority, to put it mildly.

And we know from 2008 that shadow bank collapses can have huge ramifications, as interlinkage and leverage tend to show up in unexpected places.

Then we have many Western governments with near-exhausted public finances, the US is running 7-8% deficits well into the future, and how will bond markets react to the possible combination of:

The reversal of the petrodollar inflow

A world recession

Higher inflation

Imploding private equity funds exposing wider financial fragility

The AI data center buildout, the main force driving US economic growth, running into much higher energy costs and other constraints, with finance drying up.

We already basically have jobless growth; unemployment could rise significantly if several of these elements play out.

This is all hypothetical, and the element we’re least sure about is what a private equity collapse could produce in terms of stress to the wider financial system. There are counterbalancing forces; the AI revolution could very well boost productivity and thereby compensate for the likely stagflationary pressure to some extent.

Meanwhile, markets keep on climbing as if nothing happens, happy with a few reassuring tweets, and some of our recently featured stocks have done well, three of them in more or less the same segment, so let’s turn to these.

LifeMD (LFMD)

We argued late March here that LFMD was finally catching a break.

With the end of scarcity and the regulatory clampdown on compounded GLP-1 meds, these telehealth providers have to get into the good graces of brand-name providers like Novo Nordisk and Eli Lilly, and LifeMD was early to strike agreements with both.

The problem with that is that these compounded GLP-1 meds are much more lucrative, but LFMD has painstakingly built an infrastructure for handling private and public payers, which gives the company an edge.

It’s comparable to the compliance infrastructure that perhaps our favorite stock, Hydreight, has built and is now offering as a service.

In our above-linked recent article, we issued a strong buy on LFMD at $3.50, mainly for the insurance infrastructure (which HIMS doesn’t have, for instance), which will revive growth and substantially lower CAC.

It’s early days, but so far it’s working out, although Q1 might provide a bit of a hurdle as they’re stepping up on expenses in order to accelerate member growth.

Hims & Hers (HIMS)

Another one that worked out pretty well, while we argued in early March that the low 20s should work out well longer-term, that longer-term turned out to be shorter than we imagined (we latched on early at the possible terrible economic fallout from the closure of Hormuz and didn’t expect back then that the market would largely ignore this).

The large short count makes any short-term stock predictions even more difficult than usual, but this can work both ways. It’s been there forever and hasn’t stopped HIMS reaching 60+ (and us making out as bandits on three multi-bagger trading positions for our SA Investment Group), but it’s something to keep in mind.

Collaborating with Novo Nordisk, rather than being sued by them, is definitely an improvement, and a logical one, as it’s a win-win situation.

Still, growth declined substantially, and brand-name GLP-1 is much less lucrative compared to compounded versions. Growth will mainly come from additional products and international expansion, as we argued in the above-linked article.

JP Morgan’s new coverage and $35 price target is a long way off from recent $60+ highs.

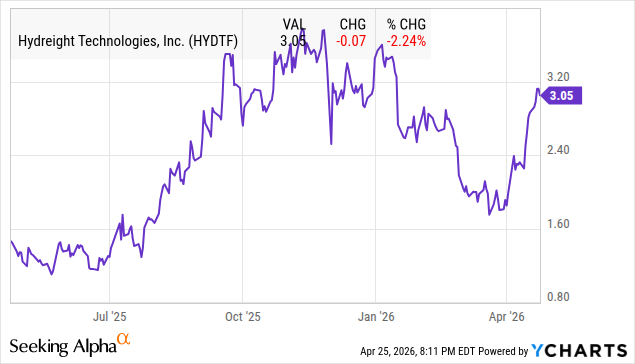

Hydreight (HYDTF)

Maybe our top pick at the moment, as we could come up with no less than 10 reasons to buy the stock last week, and we’ve made that article accessible to non-subscribers.

Not a lot happened in the few days since. The stock is up nicely; it also turns out that the company is buying its own shares. For an emergent growth company still in hypergrowth, it’s actually quite impressive that they are cash flow neutral already.

We think the valuation is still reasonable at $3, a little over 1.3x EV/S on the guided baseline FY26 revenue of C$150M for a company with this growth profile and profitable already (albeit minimal), that’s certainly not expensive.

And we know that at the end of Q1, they had 11K licenses sold for its VSDHOne platform, a dramatic increase from the 2.5K at year-end, and our article explains how they achieved that.

We still think it’s a strong buy here.

Identiv (INVE)

Another one of the recent companies we featured was Identiv, which we wrote about at the end of March, and the title (“Identiv Looks Very Interesting Here”) says it all.

They need scaling, but they have plenty of cash to achieve that and a secular tailwind from industry developments as these tags get ever cheaper, which primes them for mass adoption.

They are in a good position with a huge deal with IFCO, which is likely to fill some of the huge production capacity they have and bring them into adjusted EBITDA positive territory.

While they don’t have the field all to themselves, they are at the forefront of the technology (introducing new products last week), and for investors, it’s interesting that despite fairly low margins, the business model can scale impressively due to the huge production capacity they already have with a new plant coming online.

Then there is the huge cash balance ($128.9M), and with FY26 cash use projected to $14M-$16M, there are lots of things they can do with that.