10 Reasons To Buy Par Technology

A follow up to our overview article

The premier restaurant software providing a ‘Unified experience’

Chains moving to the cloud

Big chain wins; Burger King

Flywheel effect

MENU and Payments still loss making but scaling up rapidly

Payments are increasingly attached to Brink

ARR growth

ARPU growth

Margin expansion and operational leverage

The company is about to turn profitable and cash-generating

Leading POS cloud software

The company has history on its side, Brink began as a very small outfit, but management has built it out to the leading POS cloud software through internal improvement and development of new solutions like Payments, and through M&A (MENU, Punchh, Stuzo and TASK as the main ones).

Restaurant chains are moving to the cloud

They’re moving to the cloud and away from trying to produce their own solutions (like Burger King and Subway).

This comes at the right moment as Par’s competitive position is better than ever, which is why (Q3/23CC): “I’d say just in this quarter we’ve seen more RFPs and interest from the largest brands in the world than we have in my entire time at PAR as it relates to POS. And we also see that in loyalty within Punchh… it seems to have kicked off.”

Accelerating customer wins and increasing the pipeline

Here are the wins just for this year:

The customers are also getting bigger, as epitomized by winning the domestic business of Burger King in October 2023.

Increasing pipeline

Burger King will add its 7.2K US restaurants on Brink and a specialized version of MENU, spread over the next 18 months and adding $23M+ in ARR, but there are additional opportunities:

Adding Punchh ($900/year), Data Central ($1,500/year), or full MENU (MENU link is $500 while full MENU is closer to $1,500).

Burger King abroad has 11K restaurants.

Parent company RBI has other brands (Popeyes, Tim Hortons, Firehouse Subs) and 30K+ worldwide locations in 100+ countries. RBI will likely want all its brands on the same POS software.

Management has been much more optimistic about the pipeline in the last couple of quarters, Burger King has given them a lot of credibility. Deals are piling up (Q1CC): “As I said a couple of calls ago, we've never had so much deal flow on the brink, data central, and payment side before. We're looking forward to sharing more details on that as we win those deals, put out press releases. I think it's reflective in that as you win a large customer and then another, it helps other brands feel comfortable that you can handle that scale.”

Roark Capital is the owner of Inspire Branks which purchased Subway (37K stores worldwide) is among the most notable and they have expressed the desire to have them all on the same POS system, being in active RFP with Oracle and PAR as the main contenders. Subway has botched to produce its own POS system.

Expanding into new segments

The company is expanding into table service through its Brink POS Spring 2024 release.

It’s expanding into convenience stores with the Stuzo acquisition.

It’s expanding overseas with the TASK acquisition.

Flywheel effect

While the individual solutions are best-in-breed on a stand-alone basis, the whole is bigger than the sum of the parts, here is CEO Savneet Sing (Q1CC): “Each of our products generates better experiences on other PAR products, thereby enhancing total stickiness and expanding sales opportunities beyond what a single product sale could generate. The flywheel at PAR is real.”

For instance, Brink now comes with a nearly 100% attachment rate for the company’s hardware (POS terminals) and also increasingly with Payments and Data Central.

It’s not just the cross-and upselling opportunities, it’s also the whole getting bigger than the sum of the parts, improving the value proposition (and hence pricing!) for prospective customers and stickiness of existing customers.

Stuzo and TASK acquisitions

TASK has Starbucks Australia and McDonald’s international as customers and opens up overseas markets for PAR, with one opportunity the foreign Burger King restaurants (which outnumber the 7K domestic ones).

Stuzo is a top loyalty product for convenience stores, opening up a new segment and reducing competition with Punchh. Longer-term, these products will be merged.

Stuzo runs in over 25K convenience stores, the acquisition of Stuzo contributed $41 million to ARR, adding TASK adds another $40M+ and ARR would be $225M+. there are 150K convenience stores domestically.

These acquisitions reinforce the flywheel: here is what Greenhaven argued about the recent (Stuza and TASK) acquisitions: “Both accretive and both EBITDA positive, the acquisitions provide additional scale for PAR, accelerate profitability, add new markets, and add new customers. Each one of those factors – scale, profitability, new markets, and new customers – matters individually, but together they can create a lollapalooza.”

From Voss Capital: “For $400 million in aggregate, they have acquired what we believe will be $100 million in ARR and >$25 million in EBITDA in 2024 on a >20% growth rate (collectively a Rule of 40 acquisition).

MENU and Payments scaling

The company invested a lot in MENU last year and that will turn fast as the investments are done and MENU is starting to gain traction, with 1.2K activations in Q1.

Payments is also in the first innings where it is still loss-making but it will rapidly scale, turning losses around.

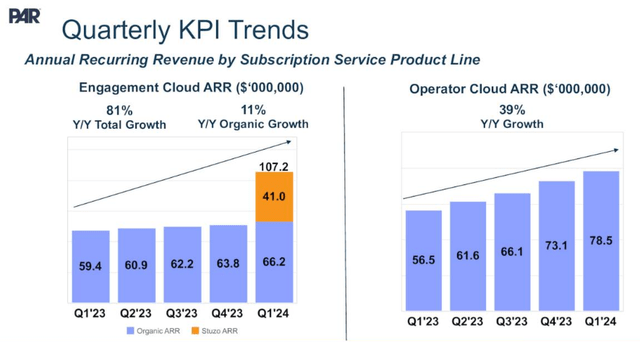

ARR growth

ARR from the two segments:

Annual Recurring Revenue growth is the main metric, rising as the company adds new logos, new sites, new products, and a rising ARPU (average revenue per unit).

Add Stuzo (which only counted for 20 days in Q1) and ARR now stands at $185.7M, a 60% increase y/y.

Adding TASK and ARR would be $225M+

Then Burger King will be added, which 7K domestic sites will roll out over the next two years and will produce 20%-30% ARR growth in FY24

ARPU rising

ARPU (average revenue per unit) is benefiting from price increases (new contracts and contract renewals) and cross- and upselling.

Contracts with new customers tend to have better price conditions than legacy contracts which is a reflection of PAR's increased value proposition and competitive position.

Operator Cloud ARPU increased by 22% and will increase further.

Brink at $2.7K/y, Punchh $900/y, Data Central $1.5K/y Menu $1.5K/y (Menu link for BK is $500y).

Engagement cloud ARPU increased by 7.5%

Margin expansion and operating leverage

The gross margin for subscription services (which includes part of hardware support contracts that consist of professional services) was 66% in Q1 but management argues that this will scale to 70%+.

Overall gross margin will benefit greatly from the selling of the low (7%) margin government business and the addition of Sturza and TASK.

Non-GAAP OpEx rose from $22.2M in Q3/22 to $25.8M in Q1/24, significantly below revenue growth and Q1/24 was a bit of an outlier due to the rollout cost of Burger King and Wendy’s. Management expects OpEx to be lower in Q4 than in Q1, excluding the acquisitions.

S&M was 21% of revenue in Q1/24 and will keep improving to below 15%.

R&D was 35% of revenue in Q1/24 and will go to 25%.

Cost containment and investment in MENU in the rearview mirror while MENU and Payments are starting to scale are the main factors behind the operating leverage.

Turning adjusted EBITDA profitable

The company still produced an adjusted EBITDA loss of $7.2M but management expects this to turn positive as soon as Q3 based on gross margin expansion and operating leverage and the contribution from the acquisitions (Stuzo produced $17M in adjusted EBITDA in 2023 and TASK is projected to produce $8-$10M in 2024, although this acquisition hasn’t yet closed).

There was considerable discussion during the Q1CC whether the company wouldn’t be able to reach adjusted EBITDA breakeven in the second quarter already and based on:

Flat OpEx + $7M organic growth at 70-80% gross margin adding $5-6M in adjusted EBITDA

A full quarter of Stuza will add another $4M or so.

The selling of the government business will reduce OpEx additionally.

Management didn’t discard this out of hand, but they guide conservatively and there are some uncertainties concerning Q2 hardware sales (which are expected to grow again in H2).

Valuation

The company had $71.4M of cash at the end of Q1, add the $102M from the sale of its government business to reach $173.4M, with long-term debt at $378.1M for a net debt of $204.7M while they also have to pay the $206M for the TASK acquisition.

At $43 per share the company has a market cap of $1.46B and an EV of $1.67B.

We think the main figure to consider is the one below with ARR in green and ARR per share in the black line:

For a market-leading SaaS provider with little churn we think that 10x ARR isn't an excessive valuation and this doesn't even cover their hardware business (and part of professional services). This isn't factoring in any new customer win from its bulging pipeline either. On the other hand, their cash will go down significantly and they will have to do a small raise or add some debt to pay for the $206M TASK acquisition.

Verdict

The company is at an inflection point, about to turn profitable whilst adding big new customers and a pipeline that has never been stronger.

Take a small position and wait for a dip to add (see graph, dips are fairly frequent).

Further reading

PAR’s Path to $80 Redux (Voss Capital)

Par Technology: Emerging As The Winner-Take-Most (Choice Equities)