100%+ Dividend Yield? What's the catch?

To say that the YieldMax MSTR Option Income Strategy ETF (MSTY) is an interesting financial instrument is a bit of an understatement:

This is AGCN, which we introduced a while ago, on steroids and then some, as AGCN generates a ‘mere’ 16% yield, and there was a catch, as we explained in that article. So there must be a catch here as well, right?

I mean, MSTY sells covered calls on MicroStrategy (MSTR) stock, which itself is a leveraged play on Bitcoin. How leveraged up can you get? How more volatile? Well, you see, that’s the whole point, as MSTY generates these huge yields (paid out in orderly monthly installments) by selling that volatility.

There is the risk of some NAV erosion as the upside on MSTR is capped, while the downside is cushioned by the option premiums, which are mostly paid out. This cushions the total return downside for holders, but not the NAV, and there are some other potential sources of NAV erosion.

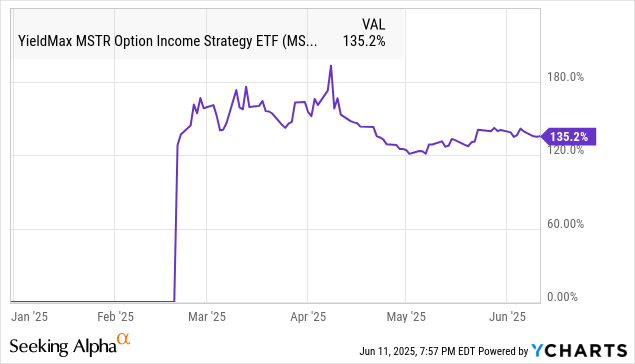

Should investors worry about NAV erosion? It has been minimal since inception, and with yields like this, within a year, investors have gained the entire NAV in dividends, and the rest is essentially a free income ride into perpetuity. An interesting strategy would be to reinvest those dividends.

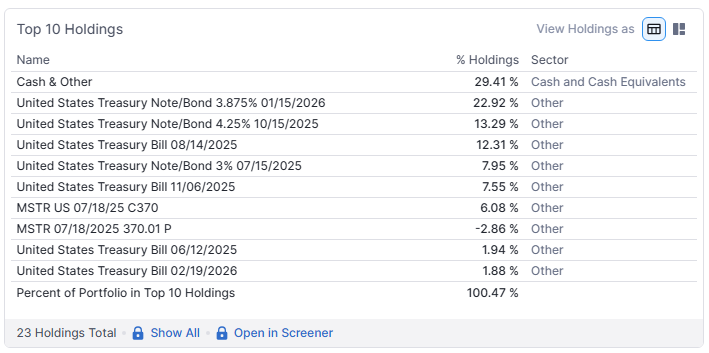

There are other legitimate issues to worry about. What will happen to the yield if Bitcoin spirals into a bear market and stays there for a prolonged period of time? This will take MSTR down more, but guess what, NSTY doesn’t actually hold much NSTY:

(One can find a more detailed or current list).

These written put options (there could be a few more) might be executed in a downdraft, but most of the portfolio is in Treasuries and cash. NAV is unlikely to crash overnight, as could potentially happen with MSTR, which is a leveraged play on Bitcoin.

But a multi-month, let alone a multi-year Bitcoin bear market, could do more serious damage to MSTRs NAV by repeatedly forcing the written puts to converge into shares (which are likely to be sold at a loss), although active management might be able to mitigate this.

Any reduction in MSTR’s volatility will compress option premiums and hence MSTY’s gargantuan yield, but that’s still likely to remain much higher than most other income-generating instruments, given the inherent volatility of MSTR, and MSTY is actively managed, it can adapt to market circumstances.

We’ve seen that recently with MSTR’s volatility declining without affecting MSTY’s yield all that much.

We’ve also seen people argue that MSTR is a better hold, as its total return is superior to MSTY and you can write covered calls on it, but it will also go down faster when Bitcoin goes down, and it’s trading at a significant premium to its NAV. We see MSTR as considerably more risky than MSTY.