A Primer on Gatekeeper

See also

Overview

Headquartered in Abbotsford, British Columbia, Gatekeeper Systems Inc. (GSI) designs, manufactures, and installs high-definition video-based safety and security solutions for transportation platforms across North America.

The company was founded in 1997 by current CEO Doug Dyment, who previously developed and sold a school bus video system to Silent Witness Enterprises, helping that firm achieve significant global revenue. GSI went public in 2013 via a reverse takeover.

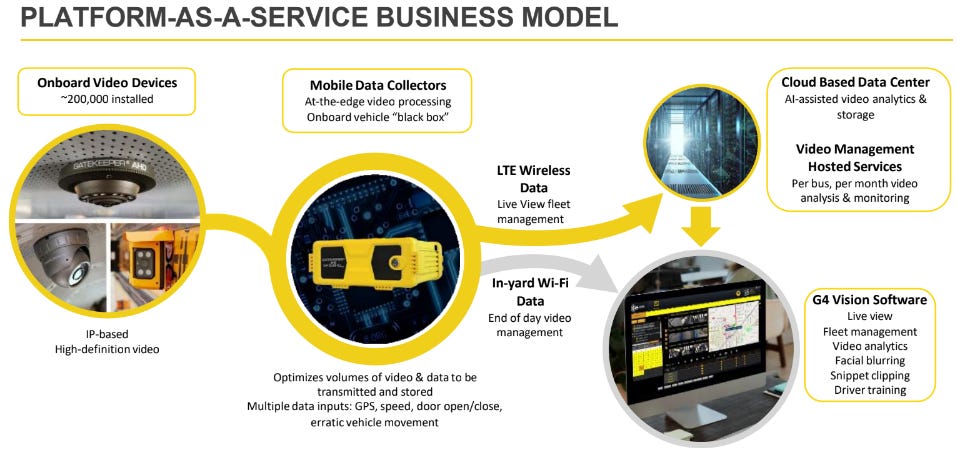

While GSI’s foundation is in hardware, it is aggressively transitioning to a Platform-as-a-Service (PaaS) model. This approach combines proprietary hardware with internally developed AI-assisted software and cloud-hosting services to create recurring revenue streams through subscription models.

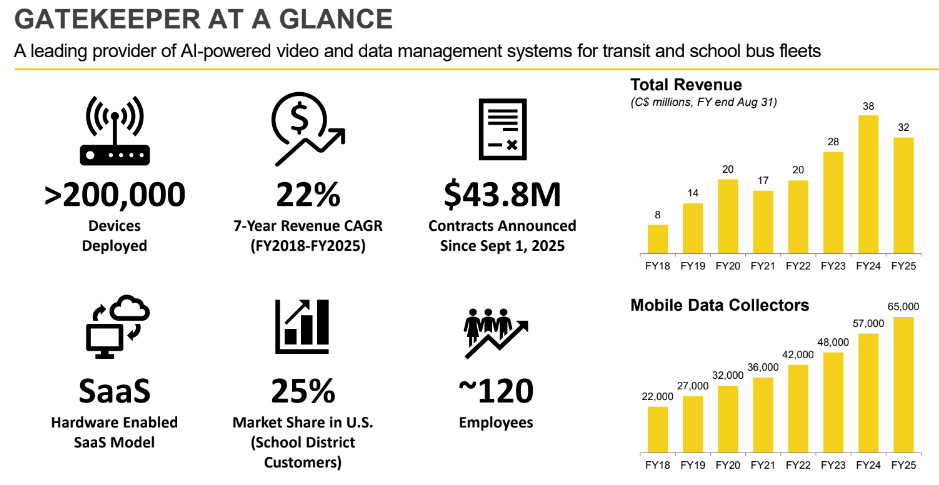

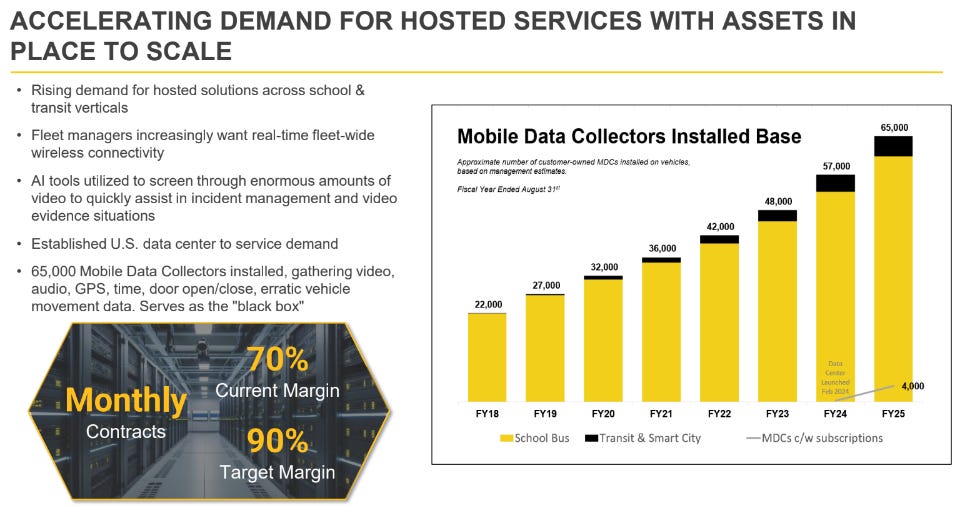

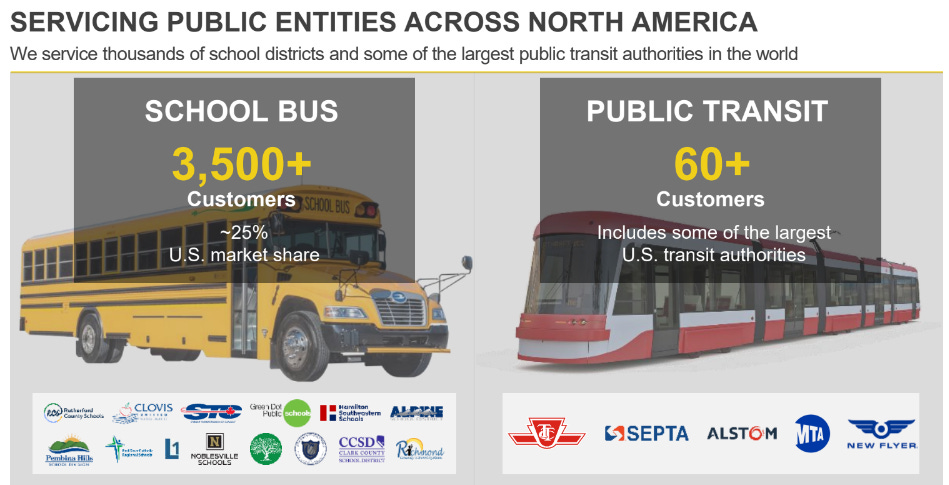

As of late 2025, the company has an installed base of approximately 65K intelligent Mobile Data Collectors (MDCs) and over 180K video devices across more than 3,500 school districts and 60 transit authorities.

Market Dynamics and Regulatory Drivers

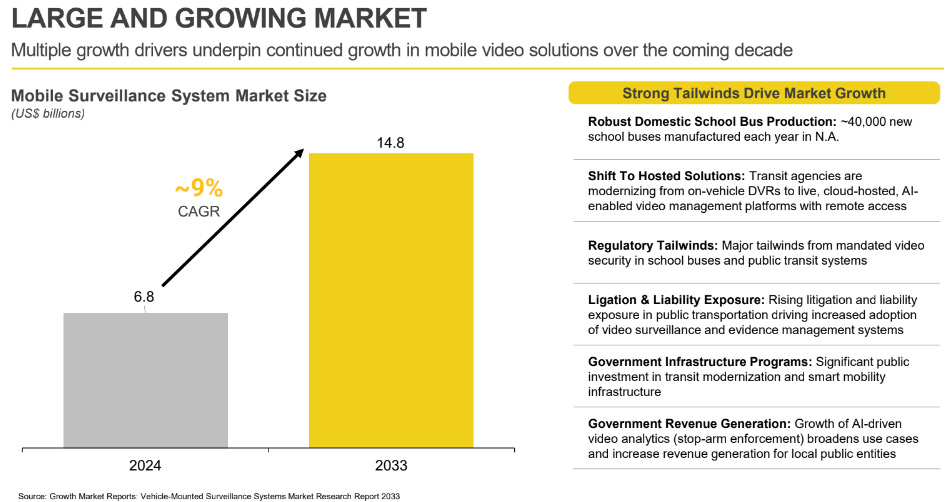

The global mobile video surveillance market is projected to reach between $3.9B and $4.7B by 2029–2030, reflecting a Compound Annual Growth Rate (CAGR) of 8% to 12%.

Legislative Tailwinds: Adoption is being accelerated by new safety mandates.

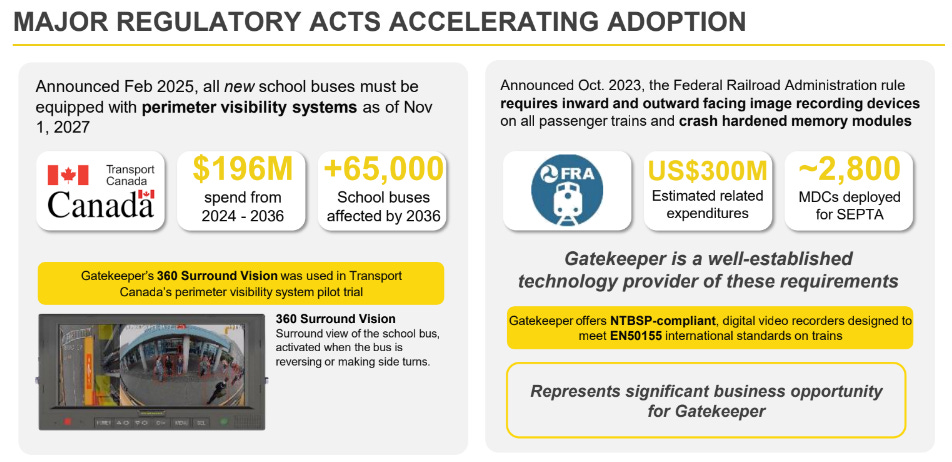

Canada: The Motor Vehicle Safety Regulations (SOR/2024-239) mandate perimeter visibility systems for all new school buses built after November 2027.

United States: The Federal Railroad Administration (FRA) now mandates inward and outward-facing cameras and crash-worthy memory modules on all lead locomotives for passenger trains, with a compliance deadline of October 12, 2027.

Competitive Landscape: GSI operates in a fragmented market. While large tech firms like Motorola (Avigilon) or Honeywell supply components, they often lack the turnkey, curated solutions required by transit and K-12 customers who have minimal IT infrastructure. Raymond James ranks GSI’s software platform at the highest level (4) compared to peers.

Products

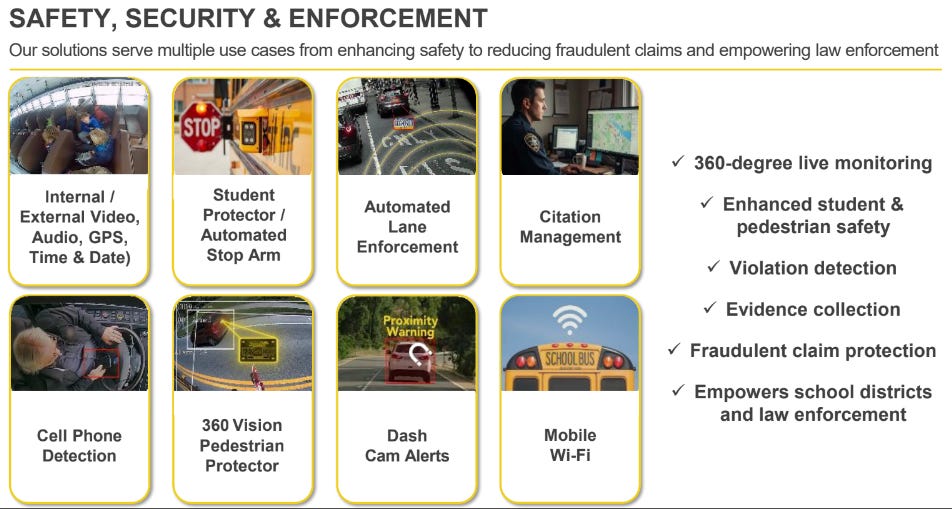

Intelligent Hardware

Mobile Data Collectors (MDCs): Military-grade “black box” recorders that collect video, audio, GPS, and vehicle data (speed, door status).

360 Surround Vision: Provides drivers with real-time views of blind spots, particularly critical for children crossing near buses.

AI-Enabled Solutions

Student Protector: Automatically detects and records license plates of vehicles illegally passing school buses.

Pedestrian Protector: Uses AI for blind-spot detection to alert drivers of nearby children or pedestrians.

Automated Lane Enforcement (ALE): Designed for “Smart Cities” to automate ticketing for vehicles violating transit-only lanes or passing streetcars illegally.

Software and Hosting

G4 Vision & CLARITY: Software hubs for fleet management, video analytics, and incident management.

Hosted Data Center: Launched in February 2024, GSI’s data center facilitates remote management and storage, appealing to U.S. clients who must meet federal data privacy requirements.

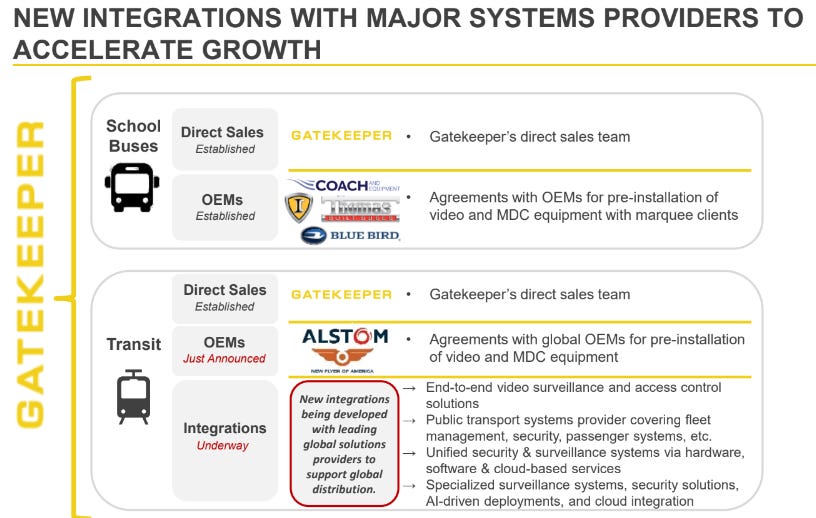

Key Market Segments and Marquee Contracts

K-12 School Bus Segment: This is GSI’s legacy market, where they hold an estimated 25% share of the US market.

California School Bus ($9.3M): Announced in late September, this was the company’s largest-ever win in the school bus segment, providing interior/exterior video and AI passenger counters.

Public Transit Segment: This segment is experiencing parabolic traction.

SEPTA (Philadelphia): A long-term partner that uses GSI’s video management to save an estimated US$22M annually in liability claims.

LIRR (Long Island Rail Road): A record $27M contract announced in September 2025 to upgrade audio-visual systems in compliance with FRA mandates.

Alstom: Selected as the OEM factory-installed video provider for Alstom’s light rail vehicles, including 130 electric streetcars for SEPTA.

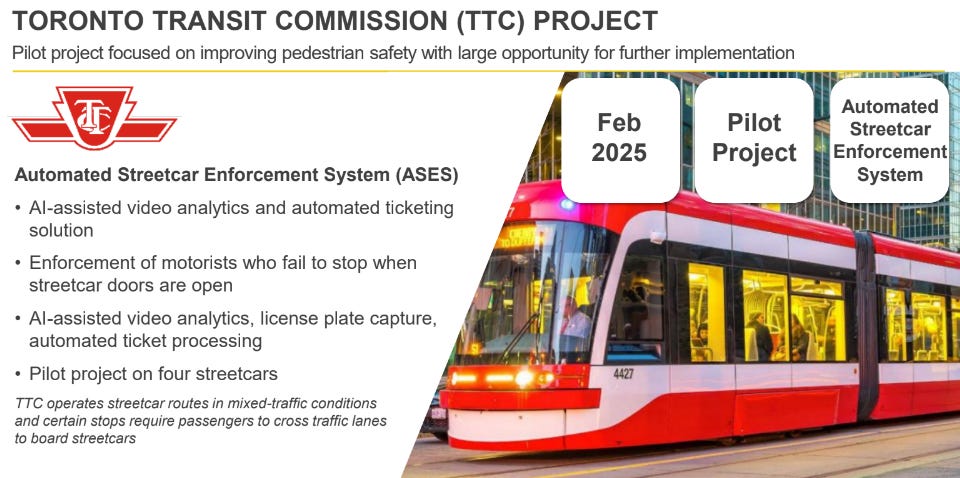

TTC (Toronto): Awarded a pilot contract for the Automated Streetcar Enforcement System (ASES).

Recent developments

Calendar year 2025 was a pivotal “inflection point” for Gatekeeper Systems. The company transitioned from a small hardware provider to a major player in large-scale government and transit contracts, backed by significant capital raises.

The company secured $43.8M in new contracts since the close of FY25 (August 31, 2025).

Strategic Financing & Liquidity

To support these massive new projects, Gatekeeper aggressively raised capital, ending the year with one of the strongest balance sheets in its sector.

Capital Raised: The company completed two major “bought-deal” financings in July and November, raising a combined $25M in gross proceeds.

Cash Position: As of August 31, 2025, the company held $14.8M in cash with no significant debt, providing the “foundation pillars” needed to bid on multi-million dollar government tenders.

Credit Facilities: Expanded its credit line with TD Bank to include a $7.5M Letter of Credit facility specifically to handle performance bonds for large-scale projects.

Transition to Platform-as-a-Service (PaaS)

2025 marked the first full year of operation for Gatekeeper’s AI Data Center (launched Feb 2024), shifting its revenue model toward recurring software income.

Subscription Growth: The number of Mobile Data Collectors (MDCs) under monthly-recurring hosted service contracts grew from ~300 at the start of the year to 4K by year-end.

Infrastructure Investment: Management intentionally accepted a $3.0M net loss for the fiscal year to fund a massive expansion of its sales team (attending 66 trade shows) and cybersecurity infrastructure.

Leadership & Global Expansion

New Board Expertise: In November, the company appointed Hamish Dobson, a veteran of Motorola Solutions and Avigilon, to its board. His expertise in AI-powered video security aligns with Gatekeeper’s shift toward high-end analytics.

Middle East Entry: Late in the year, they secured a proof-of-concept (POC) contract for the Etihad Rail project in the Middle East via L&T Technology Services, marking their first significant entry into the global freight rail market.

Financial Performance

Revenue Scaling: Raymond James forecasts revenue to grow from $31.8M in F2025 to $45M in F2026 and $67M in F2027, driven by the massive transit contract backlog.

Profitability and EBITDA:

F2025 Impact: F2025 EBITDA is expected to be negative (~$1.6M) due to one-time charges, including a $1.6M obligation and a $300K bonus recognized for the CEO to clear legacy agreements.

Future Margins: Long-term EBITDA margins are modeled at 28% by F2036, though near-term gross margins may moderate to 40% as GSI secures market share with major transit contracts.

Capital Position: GSI completed two equity raises in 2025 totaling $23.5M, leaving the company with “significant dry powder” for M&A or internal R&D.

Management and Governance

Leadership Team:

Doug Dyment (CEO): Largest shareholder; decades of experience in the mobile surveillance industry.

Kelsey Chin (CFO): CPA with experience managing numerous public companies.

Jeff Gruban (VP Transit): Leads the rapid expansion into transit and rail markets.

Board of Directors: Includes seasoned industry veterans such as Hamish Dobson (former Motorola/Avigilon executive) and David Stumpo (founder of APTREX and former SEPTA Chief Officer).

Investment Risks

Supplier Risk: Heavy reliance on Asian-based OEM manufacturers for technological inputs like cameras and motherboards; disruptions could delay project delivery.

Project Concentration: Revenues are largely derived from pre-determined project installations; delays in these large-scale transit contracts could impact quarterly financial results.

Regulatory Uncertainty: Changes in privacy laws or a shift in legislation regarding stop-arm cameras could alter demand in the K-12 segment.

Market Competition: Rapid technological changes require constant R&D investment to prevent loss of market share to new or larger entrants.