A Quick Take on SOFI 2

Powering ahead, up some 150% versus the last time we looked..

We did a Primer on SOFI in February 2024, and the shares are up almost 150% since, although most of the gains are fairly recent. Time for a progress report, as the stock has done very well lately.

This can continue as the growth in the FinTech, capital-light part of the model is very high and producing tremendous operating leverage through economies of scale and scope, which increase LTVs and reduce customer acquisition cost.

The company benefits from low funding costs through its digital banking business versus other FinTechs and not having to maintain an expensive branch network versus banks. It’s borrowers have high FICO scores and average incomes well into six figures, the company has multiple ways to reduce credit risk.

We think when we look another 18 months out the shares will be significantly higher again.

Company Overview and Business Model

SoFi Technologies, Inc. (SOFI) is a fintech company offering a wide range of lending and financial solutions, including loans, digital banking, and investing services.

It operates on a cloud-native platform and provides full financial services similar to a traditional bank, but at a lower cost due to the absence of physical branches and reduced personnel needs.

SoFi's operations are divided into three main segments: Lending, Technology Platform, and Financial Services.

Sofi offers a one-stop shop FinTech platform that enables the company to introduce competitive products that are rapidly gaining traction.

The company benefits from platform economics, producing economies of scale and scope and continuously improving the LTV/CAC (lifetime value/customer acquisition cost) ratio.

Its platform is so good that it sells as a B2B business (“Technology Platform”) to other financial institutions through its subsidiaries, Galileo and Technisys, and sales are likely to accelerate in H2 and FY26.

Its banking business gains members for its Financial Services platform and offers multiple advantages like low funding cost (deposits), flexibility in keeping loans on the book or selling them, and requires no branch network.

The Financial Services and, to a lesser extent, the Technology Platform segments have reached escape velocity and are producing tremendous operating leverage.

The company is gaining market share.

Competitive advantage

SoFi controls the entire value chain—from customer acquisition to product delivery—enabling efficient operations, better data utilization, and faster innovation compared to traditional banks and many fintech rivals.

SoFi's Financial Services Productivity Loop (FSPL) drives high cross-sell rates, with many members adopting multiple products quickly, fueling a virtuous growth cycle and revenue diversification.

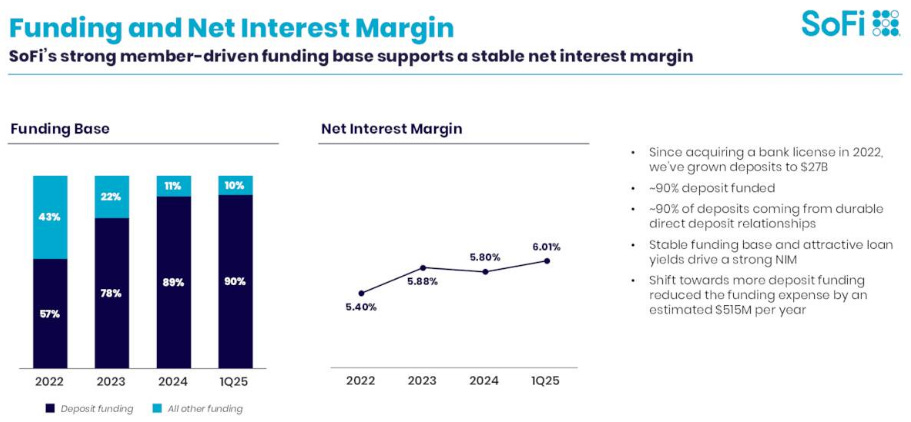

With a nationally regulated banking charter and $27B in deposits (mostly from direct deposits), SoFi benefits from lower funding costs, improving margins and enabling competitive APY rates on deposit products. Total deposits grew to $27.3B, management argues that this is lowering funding expense by an estimated $515M per year.

SoFi targets a younger, tech-savvy demographic with tailored, user-friendly digital experiences, providing convenience and flexibility that many legacy banks struggle to match.

The company’s loan platform monetizes a large volume of loan applications with minimal credit risk and capital requirements, supporting sustained high-margin fee revenue growth.

SoFi’s culture and technology allow rapid adaptation to market changes and regulatory environments, maintaining its edge in a competitive fintech landscape.

Recent Performance and Strategic Shift

SoFi has demonstrated impressive financial results and is undergoing a significant strategic pivot towards a capital-light, fee-based revenue model of its Financial Services (and Technology Platform) segment.

Revenue Diversification

In Q1 FY 2025, SoFi generated $315M in fee-based revenue, representing a 67% year-over-year (YoY) increase, and now comprises 41% of total revenue.

This marks a clear break from rate-sensitive lending, with growth driven by capital-light segments such as interchange (up 90% Y/Y) and its loan platform (up 44% Q/Q to $96M in Q1).

The loan platform business generates high-margin fees through strategic deals with partners like Blue Owl ($5B) and Fortress ($2B), allowing SoFi to seize loan demand without retaining loans on its balance sheet or assuming credit risk.

Financial Services

This is its FinTech platform offering a host of services, most notably SoFi Money, its high-yield, no-fee cash management account. It’s like a hybrid between a checking and savings account, allowing users to securely deposit money, earn competitive interest, and spend funds through bill pay, peer-to-peer (P2P) transfers, checks, and a debit card. Management argues that SoFi Money will be its second $1B revenue product, from the Q1/25CC:

For example, this quarter we completed the rollout of self-service wires, which gives members another frictionless way to move money. We are now the only company that offers digital person to person payments via phone number or email address and the ability to send money via Zelle, ACH or self-serve wires. Given the performance of SoFi Money, we expect it to become our second one billion dollars revenue business.

Net revenue was $303M, more than double that of Q1/24. Contribution profit was $148M, up 4x from last year, with a contribution margin of 49%.

Net interest income for this segment was $173M, up 45% YoY, driven by growth in member deposits.

Non-interest income grew 3.2x to $130M, equating to over $0.5B in high-quality fee-based income annualized.

Financial services revenue per product increased nearly 50% from $59 in Q1/24 to $88 in Q1/25.

The Loan Platform Business (LPB) generated $96M in adjusted net revenue, up 44% from Q4 2024, primarily from $1.6B of personal loans originated for third parties and referrals. This growth was aided by recent partnerships totaling $8.2B in new deals (Blue Owl, Fortress, Edge Focus), which will accelerate growth further in Q2 and beyond, from the Q1/25CC:

Another key contributor to growth in Financial Services is our loan platform business where we produce loans on behalf of third parties. In less than a year, we've grown the business to an annualized run rate of over $6 billion of originations and more than $380 million of additional high margin, high return fee based revenue… the LPB loans do not present any ongoing credit risk and contribute to member growth as we hold the relationship and can benefit from cross buy into other SoFi products.

The loan platform business still has ample room to grow, even more so, if the company choses to move “outside its credit box” (Q1CC):

Today, the bulk of our loan platform business is in and about our credit box, just volume that we wouldn't otherwise want to originate on our own balance sheet, both from a credit and risk standpoint.

To give you an idea of the opportunities, they turn down $100B in loan applications a year. They can select, within their own ‘credit box,’ fill their balance sheet and turn the rest over to third-party lenders on the LPB platform.

Other products in Financial Services are also up strongly (see the wheel below) as the flywheel effect takes hold

Financial Services Productivity Loop

This strategy drives cross-buying, with 32% of new products adopted by existing members, enhancing client lifetime value and engagement. This number increases significantly for SoFi Plus subscribers, with over 75% adopting a second product and over 40% a third product within 30 days of enrollment for new-to-SoFi Plus subscribers.

Member growth was 34% Y/Y to 10.9M, and product growth was 35% Y/Y to 15.9M.

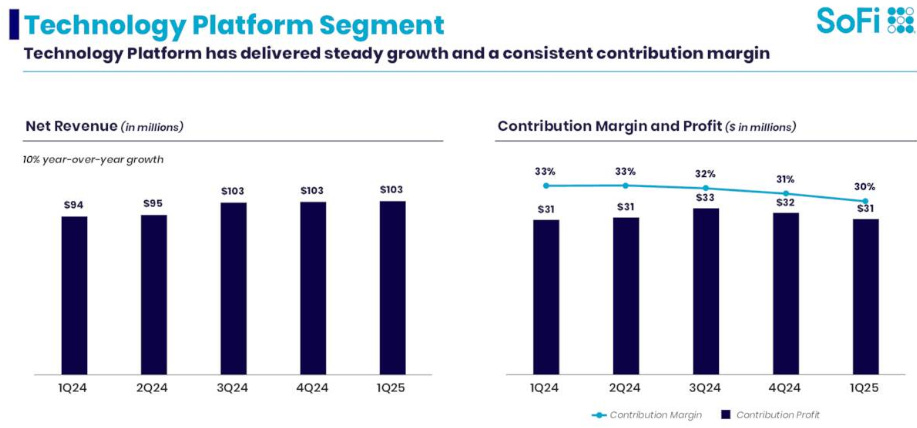

Technology Platform

Net revenue was $103M, up 10% Y/Y, and contribution profit was $31M, at a 30% contribution margin.

Accounts were down slightly to 158M (6% Y/Y decrease), attributed to a large client diversifying processing providers, which was factored into the 2025 outlook.

New client wins are expected to drive financial performance and offset this in FY26. The market for digitally native financial products remains significant and demand for tech platform services is increasing due to traditional financial institutions needing to innovate, Q1CC:

We've signed a number of partners that will be integrated this year and they'll contribute to revenue in 2026.. I do think there could be an acceleration in 2026 relative to 2025 in terms of the number of new deals, one, and the impact they could have because of the fact that people are starting to move more aggressively into innovative areas and they can no longer compete from an innovative standpoint.

Lending

Adjusted net revenue +27% to $412M.

Contribution profit was $239M, with a 58% contribution margin.

Total loan originations were up 66% to a record $7.2B:

Personal loan originations were a record $5.5B (including $1.6B for LPB), up 69% Y/Y.

Student loan originations were $1.2B, up 59% Y/Y.

Home loan originations were $518B, up 54% Y/Y.

Most of its lending is funded by its bank deposits, producing a rising NIM and providing SoFI with a competitive advantage that other FinTechs can’t match, from the Q1CC:

we have a competitive advantage. And that competitive advantage is that we have an insured depository entity in a SoFi bank and we have four loan products. Most companies that are not banks that are providing an interest rate on deposits are doing it on the back of a sponsor bank. And those deals are limited in terms of what the APY they can offer. They're typically Fed funds plus 20 basis points. It can't be more than that. And if it is, it's marginally more, maybe Fed funds plus 30 basis points. It is limited. And so it's a really tough strategy to try to live in a world that you want to be a holistic one stop shop and have a limit on what you could do in any product, whether it's interest rate on loans or interest rates on deposits. We have an unencumbered capability to compete on APOI if we need to, and we will, because we have such a strong ROE business from our lending business that can fund those deposits. And so on the margin, I don't know anyone that can outcompete us on the APY.

SoFi uses fair value accounting, meaning it recognizes income upfront from the premium value of its high-quality loans and then adjusts the loan values (and thus earnings) over time as defaults occur or market conditions change. This can lead to higher reported earnings and capital levels initially compared to the CECL approach, which recognizes expected losses immediately and is considered more conservative.

So far, SoFi hasn’t had serious issues with NPL (non-performing loans). SoFi sold $90M of late-stage delinquent personal loans, its personal loan borrowers have a weighted average income of $158K and a weighted average FICO score of 743. Its student loan borrowers have a weighted average income of $134K with a weighted average FICO score of 769.

The net charge-offs (the amount of debt that SoFi deems unlikely to be recovered, calculated as gross charge-offs minus any subsequent recoveries of delinquent debt) have been modest and not trending (or even trending downward):

They consistently sell loans above fair value:

SoFi could also benefit from a possible retreat of the Federal government in student loan programs like Grad PLUS, Parent PLUS, which are more attractive than their refinanced student loans, as “They come at a higher WACC and they're also typically backed by a co borrower and a parent.” (Q1CC).

Growth

The company’s main growth avenues are new members and new products, which keep the flywheel spinning.

Crypto Re-entry

On June 25, SoFi announced its return to the crypto platform, after exiting in late 2023 due to regulatory pressures related to obtaining its banking license.

The company plans to initially offer cryptocurrency trading in popular coins like Bitcoin and Ethereum, with future plans to offer stablecoins, the ability to borrow against crypto assets, and expanded payment options.

Market Potential

The U.S. Senate's passing of the Genius Act provides a regulatory path for stablecoins, opening a significant opportunity for fintechs like SoFi.

The stablecoin market is forecasted to rise more than tenfold by 2030, reaching between $3T and $4T from its current ~$250 billion.

Analysts at Citizens JMP estimate potential annual revenues from stablecoins could be $100B.

Comparison to Peers

Crypto fintechs like Robinhood and Circle trade at much higher valuation multiples due to their scalable and capital-light business models. Robinhood, which started offering crypto a few years ago, recently saw quarterly revenues top $50 million in Q1'24, with crypto notional trading volumes of $46 billion. Robinhood has an $87 billion market cap, which is over 4x SoFi's valuation. Circle Internet Group (CRCL), based on its stablecoin product, has a market cap of $45 billion.

Finances

SoFi became profitable in FY24. Q1 adjusted net revenue was up 33% to $771M.

Financial services net revenue was $303M, more than double that of Q1/24 with the contribution profit up 4x to $148M.

Q2 guidance anticipates $801.94M in revenue and $0.06 EPS, with multiple upward revisions from analysts.

The company projects FY25 revenue growth of 24%-27% ($3.235-$3.310B), outpacing the sector median.

Adjusted EBITDA margin was 27% in Q1, and the Financial Services segment showed a 49% contribution margin, indicating strong margin consistency and capacity for reinvestment.

SoFi's CEO aims to make SoFi a $10B revenue company.

Valuation

SoFi is fairly cheap for a FinTech stock but expensive as a bank.

SoFi trades at 24x EBITDA, which is below crypto peers like Robinhood (nearly 40x EBITDA).

SoFi's 36% 3-year revenue CAGR and its capital-light model justify optimism from growth-focused investors, especially as its fee-based part is growing faster than its interest rate income.

The shares are expensive on an EPS basis (37x FY26 EPS of $0.51)

Risks

The main risk is related to a worsening of economic conditions, which could lead to a slowdown of growth and a deterioration of credit risk. That doesn’t seem imminent. While the stock price was down on the tariff scare in April, management didn’t notice any slowdown in business.

SoFi's credit policy is dynamic, allowing for adjustments across eight different underwriting tiers based on economic indicators (Q1CC, our emphasis):

So from a credit policy standpoint, we have early warning dashboard across a number of external, internal, macro and microeconomic factors that kind of dictate how we approach credit. In the past, when those indicators have become red, we cut back on credit and we tightened our credit box. We can underwrite across eight different tiers. There is a period in the last three years where we cut back Tier 8, Tier 7 and Tier 6 and just underwrote through Tier 5. We're, as Chris has talked about multiple times, we're managing to a life alone lifetime loss of 8%. While in a recession, life alone losses go up. The way you maintain an 8% life alone loss when losses go up because of a recession or dislocation is you stop underwriting those higher tiers that have higher losses.

SoFi generally lends to people with significant income and high credit scores and it only collects fees on the loans originated on its Lending Platform. It sells a significant part (43% in Q1/25) of the loans originated in its banking business (mostly through securitization), although it sold only 20% of its personal loans.

Of course, more of the present HFI loans could become delinquent, but if history is any guidance, SoFi has been able to manage this quite well, and worsening economic conditions are usually accompanied by lower interest rates, which is a boost for their business.

Conclusion

SoFi is replete with competitive advantages: cheap deposit financing, a flywheel effect that produces cross-selling, increased lifetime value, and reduced customer acquisition cost. Banks have to maintain expensive branch networks.

Revenue and earnings are shifting toward its capital-light model, where there are ample economies of scale and scope to produce tremendous operating leverage.

While the shares aren’t cheap, the growth in its capital-light part seems inexorable, and it’s difficult to see what would cause a sufficient slowdown to cause valuation concerns.

While less spectacular, its lending business is growing strongly as well and credit risk seems well managed, with the company having opened a new front in the form of the Lending Platform Business, generating fees without incurring credit risk.

And just today, they are dressing up SoFi Invest with access to funds that are usually restricted to institutional investors.. https://seekingalpha.com/news/4465879-sofi-teams-up-with-asset-managers-to-offer-private-company-exposure-stock-jumps