Weekly Update 21

Quick takes on AREN, GKPRF, HYDTF, SOFI, and NUTX

Arena Group (AREN)

It’s still somewhat risky, but our take is that the cheap valuation counts for quite a lot and readers won’t disappear forever.

The new businesses, like Encore ad platform, ShopHQ e-commerce, and live video, shift AREN toward higher-margin, asset-light commerce and direct retail integration and are scaling.

Apart from the cheap valuation, our take is that the new businesses will at some point overtake the decline in readership, which is actually less serious than one might think at first hand, given that the company has put its publication business mostly on flexible costs (its ‘Entrepreneurial Publisher’ model).

We’ll have earnings in a week.

Gatekeeper (GKPRF)

One of our top picks for FY26 posted a record Q2/26 with 75% revenue growth and 5K MDCs that already produce recurring revenue, with 10K MDCs expected by the end of FY26. The Toronto trial is starting, and news about delays of the East Providence School bus project is nonsense.

With mandates in Canada and the US as secular tailwinds and the company partnering with important OEMs like Alstom and SaaS revenue rapidly increasing (albeit from a small basis) we still see excellent risk/reward here.

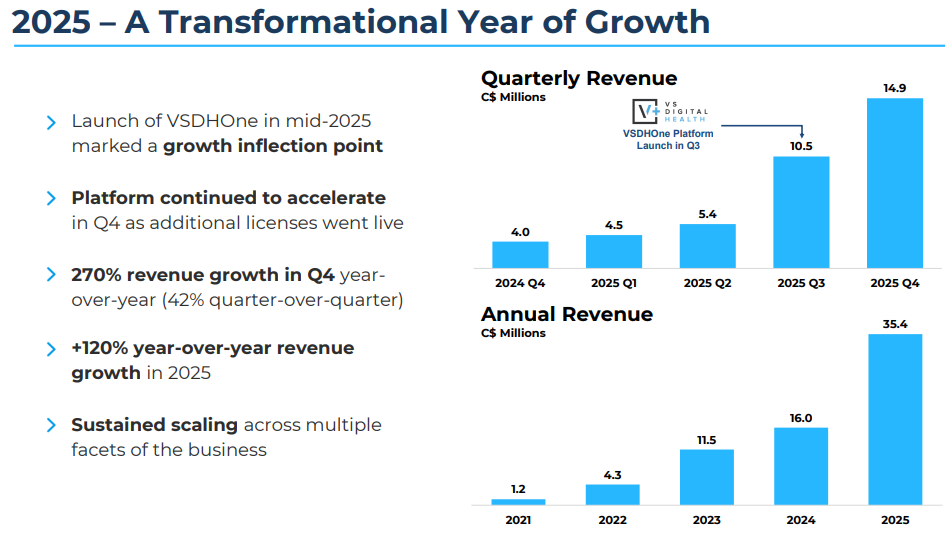

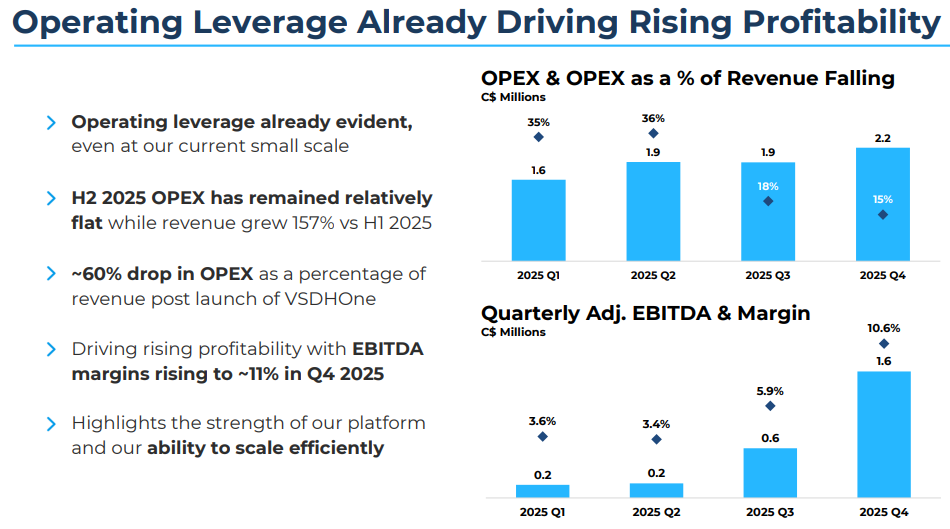

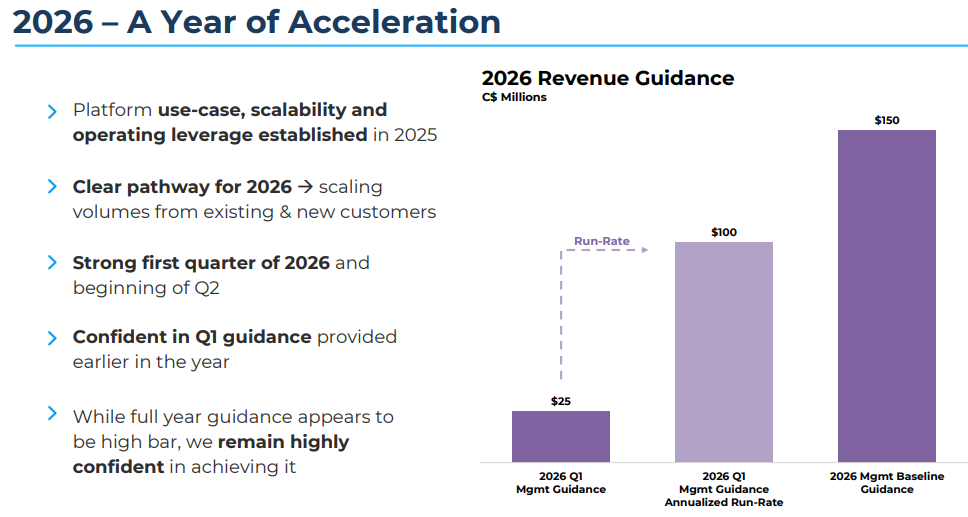

Hydreight (HYDTF)

Another company that we favor produced excellent results, in this case Q4/25 and FY25. Revenue grew 121% to C$35.4M, the company is profitable, producing significant operating leverage, and has C$30M+ in cash.

What’s more, apart from the income from nurses, part of that FY25 revenue basically comes from just 400 VSDHOne licenses, which were only activated in H2, while the company has already sold 12K licenses, but it takes time to onboard these.

We think the shares offer excellent value here. 12K licenses operating for a full year will produce multiples of revenue that the 400 licenses produced that were coming online in H2/25, so there is good visibility on rapidly rising revenue with management guiding a base case for FY26 at C$150M. Gross margins will also rise as the platform scales. Selling compliance seems an excellent idea to us.

SoFi (SOFI)

We discussed SOFI in our Weekly Update 15, recommending the shares, which rallied briefly from $15 to $20 but are now back to $16 after the Q1 results apparently disappointed investors. There was some headwind in its Technology Services segment (B2B, where they license the platform) and a lack of raised guidance.

We think the shares are still attractive, although we keep a wary eye on the economy and inflation/interest rates situation.

Nutex Health (NUTX)

We have to study the CC before a verdict here (stay tuned), but at first sight, the results were really good with a Q1 EPS of $6.52, and the shares are still trading in single-digit earnings multiples.

While its dependence on the IDR (Independent Dispute Resolution) of the No Surprises Act is declining, it’s still significant (at 50%-60% of claims), which adds an element of political uncertainty in the business model.

It wins, on average, over 80% of the IDR claims, with arbitration costs approximating 35% of arbitration-related revenue.

On the other hand, stock-based compensation turned negative ($3.9M), a sharp turnaround that was an investor concern.

Under present conditions, the company is a cash machine, producing $75.5M of operating cash flow in Q1 and reaching $207.3M in cash balance at the end of Q1.